Miami is the Nation’s Hottest Renting Spot, Midwest Heats Up the Competition

Plus: Federal Reserve Chair Jerome Powell has wrapped up a gift for the CRE market to maintain its short-term interest rates steady as 2023.

Han-Gwon Lung & Jordan B.

December 14, 2023

Together with

Good morning. Miami leads as the hottest market in the U.S., but the Midwest is increasingly becoming a strong competitor. The Federal Reserve has maintained steady rates to conclude this year, with an eye on three rate cuts in 2024. Meanwhile, D.C.’s NHL and NBA teams have finalized a major deal to relocate to Virginia, a mere 6 miles southwest.

Today’s issue is brought to you by WiCRE—connect with commercial real estate talent from one-time projects to full-time contracts.

👋 First time reading? Sign up.

🎁 Want free merch? Share this.

Market Snapshot

|

|

||||

|

|

*Data as of 12/13/2023 market close.

2023 YEAR-END REPORT

Miami Tops U.S. Hottest Markets, but the Midwest Heats Up the Competition

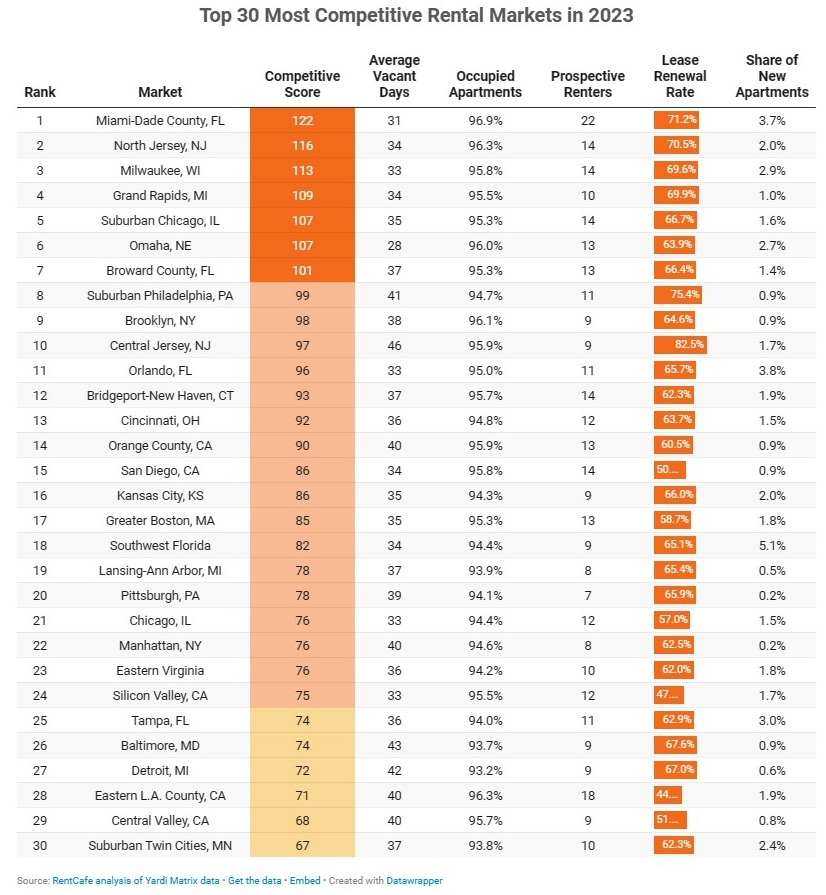

In 2023, the Midwest emerged as the most competitive rental market in the U.S., with three cities in the top five, driven by its affordability, ample space for remote work, and easy access to nature. But Miami still leads the nation.

Factors at play: The Rental Competitivity Index (RCI), developed by RentCafe, is used to gauge the competitiveness of rental markets, incorporating five key metrics: the duration of apartment vacancies, occupancy percentages, the number of renters vying for apartments, lease renewal rates, and the annual completion rate of new apartments. In 2023, the national average RCI was 59.5, but significantly higher in the most competitive markets.

America’s heartland: Favored by remote workers for its affordability and space, the Midwest became the hottest region in 2023. High lease renewal rates intensified competition, with the Midwest boasting 10 cities in the top 30 most competitive markets. Leading the Midwest, Milwaukee was the third most competitive nationally, with an RCI score of 113. With most of its population renting and less than 5% of apartments available, finding a rental in Milwaukee was particularly challenging, as apartments stayed on the market for only 33 days, attracting about 14 renters per unit.

Magic in Miami: While the Midwest had the highest number of competitive cities, Miami ranked as the #1 most competitive U.S. rental market with an RCI score of 122. High demand, fueled by job opportunities and no income tax, coupled with locals buying condos, strained rental supply. A 71.2% lease renewal rate led to fierce competition, with 22 applicants per vacancy, twice the national average. North Jersey followed as the second hottest market, with an RCI of 116, appealing to Millennials seeking affordability near NYC.

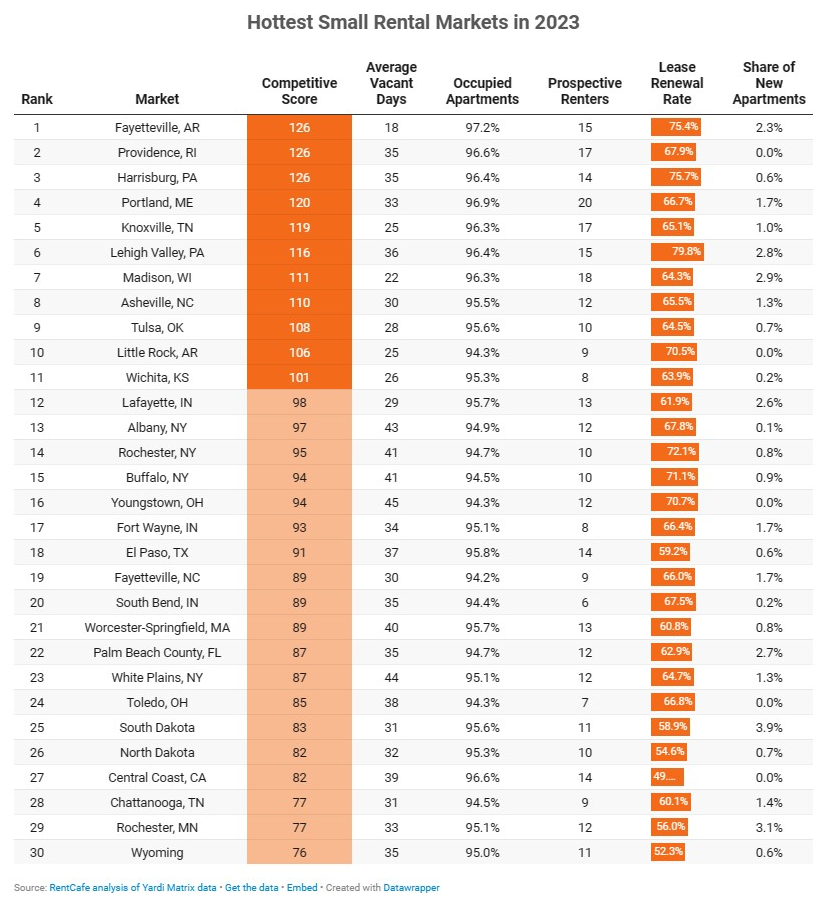

Small-town living: In 2023, small-town rental markets were also intensely competitive, with Fayetteville, AR, and Providence, RI, leading the charge. Fayetteville, boosted by its university and startup focus, had a 97.2% occupancy rate, and apartments were quickly occupied within 18 days, despite a 2.3% increase in housing. Providence, a popular choice for relocators, faced a severe housing shortage with no new constructions, a 96.6% occupancy rate, and apartments filling up in 35 days, attracting 17 applicants each.

➥ THE TAKEAWAY

Zooming out: The 2023 U.S. rental market saw the Midwest becoming the most competitive region, led by three top-ranking cities, in contrast to a general softening in other areas. Miami emerged as the hottest rental market due to its thriving tech scene and favorable business climate. The RentCafe report revealed a trend of increasing apartment constructions and evolving lease renewal behaviors, highlighting diverse regional rental market dynamics and trends.

TOGETHER WITH WiCRE

Find CRE talent your way

Bullpen is the #1 place to hire freelancers in the real estate industry, boasting over 4,000 professionals and aiding 1,000+ companies. But finding support for small projects (modeling gigs, pitch deck, etc.) has never been an option…until now.

Enter WiCRE, a platform where you can post jobs and browse a database of commercial real estate experts for hire, no matter the project size. It’s 100% free, and you can contact freelancers directly from their profiles. Give it a try!

TRENDING HEADLINES

-

Office exodus: The US office sector struggles with low office utilization rates, remaining 30–40% below 2019 levels amid the current hybrid work trend.

-

Workforce rush: Florida’s Live Local Act incentivizes developers to create more middle-income housing, resulting in more projects taking advantage of tax breaks and bypassing zoning rules.

-

Cracking down: FinCEN is set to release newly proposed rules requiring real estate professionals to report identities of cash-paying beneficial owners.

-

Commercial challenges mount: NYC’s CRE struggles continue with high interest rates, a depressed office market, and declining investment sales. But retail shows signs of improvement.

-

Paving the way: Prologis (PLD) plans to demolish a 141 KSF industrial building in San Jose and replace it with a larger warehouse.

-

Church and real estate: Citadel and Vornado Realty Trust (VNO) will pay $164M for 525 KSF of air rights from the Roman Catholic Archdiocese to develop a 51-story office tower.

-

Conversion of the day: Google (GOOGL) plans to redevelop Chicago’s James R. Thompson Center into its HQ, maintaining its iconic design while making sustainable improvements.

-

Affordable efforts: San Francisco bought an apartment building for $27.15M to convert it into supportive housing for young adults transitioning out of homelessness.

-

Housing and hotels: Perhaps unsurprisingly, affordable housing and hotels dominated the top 10 largest proposed projects in NYC for 2023.

-

Unlocking the conversion code: Self-storage conversions of empty office and retail buildings are touted as opportunities, but they make up just 4% of CRE properties in most portfolios.

COOLING INFLATION

Fed Leaves Interest Rates Unchanged and Signals 3 Cuts in 2024

Federal Reserve Chair Jerome Powell has wrapped up a gift for the CRE market to maintain its short-term interest rates steady as 2023 ends, signaling a potential shift in commercial real estate transactions heading into 2024.

Slow and steady: In the final meeting of the year, the benchmark interest rate remained at 5.25-5.5%, unchanged for three consecutive meetings after peaking at a 22-year high in July. Despite past increases to tackle inflation, the Fed plans to cut rates 3x in 2024, reflecting eased but still elevated inflation levels. Chairman Jerome Powell emphasizes a cautious approach, balancing policy firming and the need for flexibility in response to economic data and risks.

What it means for CRE: Analysts predict a slow start in CRE transactions for early 2024, with potential acceleration in the latter half if interest rates decline. Moody’s Analytics forecasts 2-3 rate cuts, starting late in Q2 of 2024. A steady decline in interest rates is anticipated, with the Fed funds rate predicted to normalize between 2-3% and the 10-year Treasury rate around 4-4.5%. This downward trajectory, evident in the recent drop of the 10-year Treasury rate, is expected to revitalize the CRE capital market, especially in refinancing distressed properties.

➥ THE TAKEAWAY

Why it matters: The market anticipates deeper rate cuts than the Fed’s projections, suggesting a more significant decrease in the federal funds rate by the end of 2024. Such a trend could ease pressures on long-term debts, offering flexibility in the refinancing market. The higher borrowing conditions experienced so far have also benefited well-capitalized sponsors, reducing competition. This financial landscape sets a unique stage for CRE in 2024, balancing cautious optimism with the need to find new deals.

HISTORIC MOVE

Washington Wizards, Capitals Plan to Leave DC for $2B Arena in VA

In a groundbreaking move, the Washington Capitals and Wizards, D.C.’s NHL and NBA teams, are set to relocate from the District to Virginia, only 6 miles away.

Details of the relocation: This relocation involves a $2 billion mixed-use entertainment district in Potomac Yard, featuring a new arena for the teams, set to open in 2028. The project, a collaboration between Monumental Sports & Entertainment, the state of Virginia, the city of Alexandria, and developer JBG Smith, represents Virginia’s first foray into hosting major North American pro sports teams. The development includes sports facilities, a corporate headquarters, a practice facility, and various commercial spaces.

Economic boost: The move is expected to bring economic growth, with investments from Monumental and matched funding from Alexandria for additional developments like a concert venue. However, it has stirred mixed reactions. Some locals, seeing it as a “billionaire’s playground,” express concerns about neighborhood needs and the development’s long-term impact. Meanwhile, D.C. faces economic challenges with the teams’ departure, potentially impacting the downtown area’s vibrancy and commercial value.

➥ THE TAKEAWAY

Downhill for DC: This relocation is more than just a sports move; it’s a transformative development for Northern Virginia, aligning with the region’s growing innovation and economic potential. On the flip side, The move will greatly affect downtown DC. The arena, which opened in 1997, has been an economic driver for the neighborhood, attracting restaurants, bars, cultural attractions, and foot traffic. The teams’ departure is expected to harm business, close stores, drop hotel demand, and worsen office vacancies and crime.

QUICK HITS

📖 READ: In Los Angeles, the prolonged 17-year struggle to construct just 49 housing units exemplifies California’s self-imposed challenges in addressing its dire need for affordable housing.

🎧 LISTEN: CRE investor Logan Freeman breaks down Congress’s attack on institutional investors while Best Ever CRE explores the top headlines investors should be paying attention to in its midweek news brief.

CHART OF THE DAY

Starting in 2024, minimum wages will rise in twenty-two states, with nine states and Washington D.C. reaching or exceeding a $15 minimum wage by January 1, as reported by DailyMail.com. Leading the way, Washington State will set the highest national minimum wage at $16.28 per hour, closely followed by California at $16.00 per hour.

What did you think of today’s newsletter? |