Apartment Construction Has Literally Disappeared in 16 Major Markets

In 16 major U.S. apartment markets, there isn't a single unit under construction — and in some of them, that's starting to look less like a problem and more like an opportunity.

Together with

Good morning. Sixteen major U.S. apartment markets have no units under construction — and in the ones where occupancy is pushing 99%, that empty pipeline is starting to look a lot less like a warning sign and a lot more like a setup.

Today’s issue is sponsored by Henry—turn your investor presentations into a polished, on-brand presentation in minutes.

🎥 Watch on demand → Flood zones don't have to be a dealbreaker — watch our on-demand webinar with DJ McClure of National Flood Experts to learn how CRE operators are using LOMAs, engineering strategies, and insurance audits to permanently eliminate flood zone liabilities across their portfolios.

CRE Trivia 🧠

What is the most expensive office building ever sold in the United States, and what did it trade for?

(Answer at the bottom of the newsletter)

Market Snapshot

|

|

||||

|

|

*Data as of 4/2/2026 market close.

Nobody Is Building

The Apartment Pipeline Has Gone Completely Dark in These 16 Markets

In 16 major U.S. apartment markets, there isn't a single unit under construction — and in some of them, that's starting to look less like a problem and more like an opportunity.

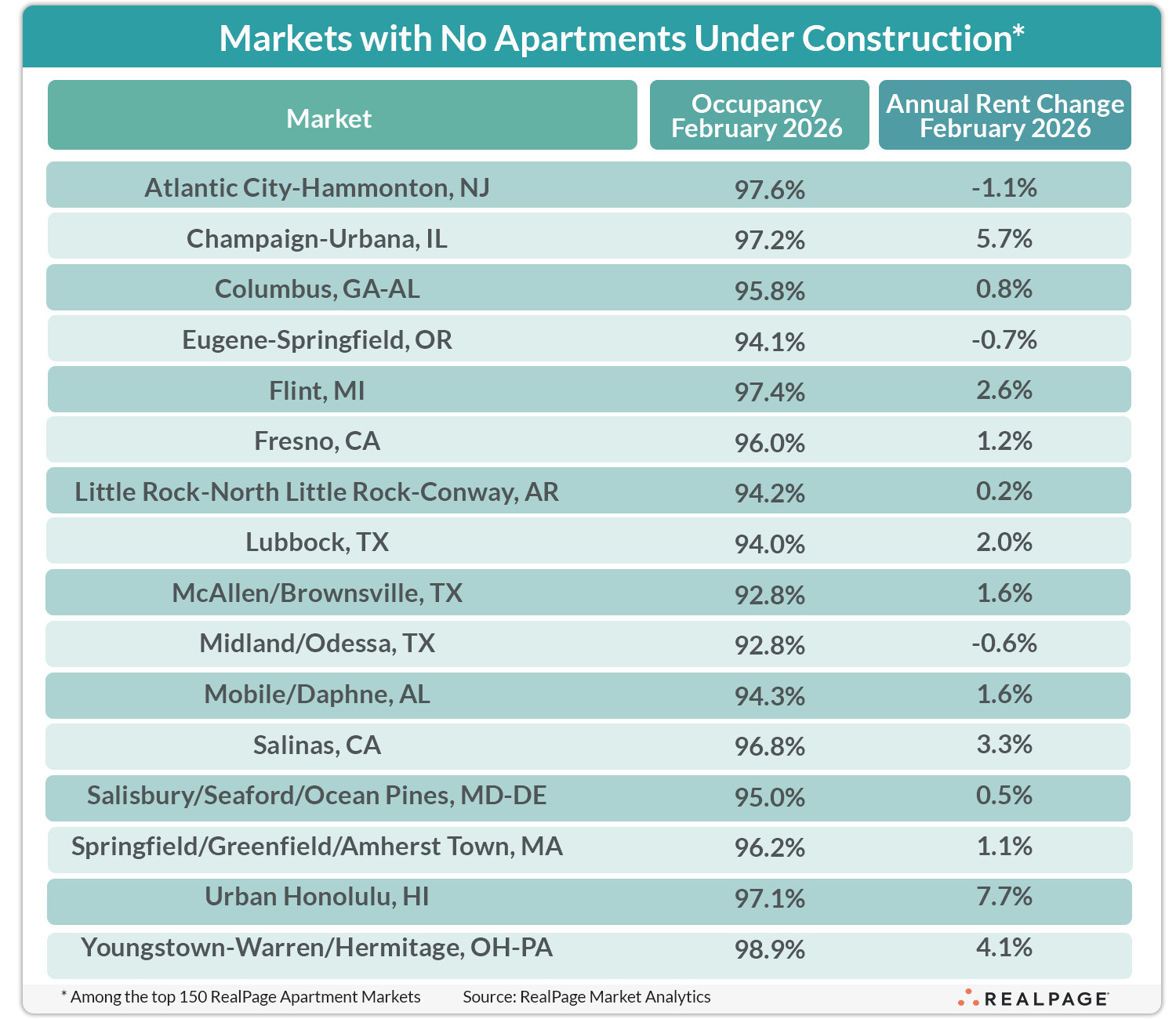

The list goes on: According to RealPage Market Analytics, 16 of the nation's 150 largest apartment markets had zero units under construction as of year-end — up from 10 a year ago and just six the year before that. The markets span the country: Atlantic City, Fresno, Lubbock, Honolulu, Flint, McAllen, and Youngstown, among others.

Screaming for product: Five of the 16 rank in the top 10 nationally for occupancy. Youngstown leads the entire country at 98.9%. Atlantic City and Flint aren't far behind at 97.6% and 97.4% respectively. Urban Honolulu posted the second-highest effective rent growth in the country at 7.7% over the past year — with nothing in the pipeline to meet it.

But it's not a clean story: Not every zero-pipeline market is a landlord's paradise. McAllen and Midland/Odessa both sit near the bottom nationally for occupancy at 92.8%, and three markets in the cohort actually cut rents over the past year. In those cases, the absence of construction reflects weak demand — not scarcity.

What the drought signals: The bifurcation is the point. Markets like Youngstown and Honolulu represent a classic setup — multi-year supply gaps meeting tight occupancy — that could produce outsized rent growth once demand firms up or capital regains confidence. Markets like Midland/Odessa tell a different story: volatility keeping developers away for good reason.

➥ THE TAKEAWAY

Why it matters: Zero construction doesn't automatically mean opportunity — but in the right markets, it's a signal worth paying attention to. As the broader apartment sector works through its oversupply, a quiet group of cities with no pipeline, near-full occupancy, and rising rents is building the conditions for the next landlord market.

TOGETHER WITH HENRY

Raise Capital 50% Faster with Institutional Quality OMs

Henry helps sponsors create polished, investor-ready deal decks that get LPs to yes faster. Upload your OM, pro forma, or rough materials and Henry builds a professional raise deck in minutes — not weeks.

AI creates the first draft. Real analysts refine every detail. No templates. No bottlenecks. Just institutional-quality presentations that stand out in investor inboxes and accelerate capital raises when timing matters most.

*This is a paid advertisement. Please see the full disclosure at the bottom of the newsletter.

✍️ Editor’s Picks

-

Fee transparency: The FTC is moving to ban hidden rental junk fees—like surprise charges for amenities and services—aiming to reshape leasing practices and give renters clearer all-in pricing.

-

What happens after a 1031 sale? Selling triggers capital gains taxes unless you complete another exchange. Learn your options—from reinvesting to cashing out—in our latest guide. (sponsored)

-

Stagflation watch: Economists are increasingly flagging a stagflation scenario, where stubborn inflation collides with slowing growth, complicating the Fed’s path forward.

-

Pyramid haircut: San Francisco’s Transamerica Pyramid traded for $692M at a steep loss from its prior sale, spotlighting how far office values have fallen—even for trophy assets.

-

Modeling overhaul: CRE firms are overhauling traditional financial models, turning to advanced scenario analysis tools to better underwrite deals in an unpredictable market.

🏘️ MULTIFAMILY

-

Construction thaw: A new NMHC survey shows modest improvement in apartment construction conditions, with developers seeing slightly better access to financing and materials.

-

Times Square conversion: Yellowstone secured $203M to convert a Times Square office building into residential use, advancing another high-profile adaptive reuse play.

-

East Bay surge: apartment rents in the East Bay hit a four-year growth high as a thinning supply pipeline tightens market conditions.

-

Brooklyn backing: JPMorgan provided financing for a major Brooklyn multifamily asset at 625 Fulton, signaling continued confidence in well-located urban apartments.

-

Pref equity stack: 3650 Capital deployed $104M in preferred equity for a $455M Chicago acquisition, highlighting creative capital stacks filling today’s financing gap.

🏭 Industrial

-

Data Center moratorium: Maine lawmakers are pushing to ban new data centers, citing energy strain and environmental concerns as opposition to the asset class grows.

-

Leased refi: Monday Properties and KPR secured refinancing for a fully leased Westchester industrial asset, signaling continued lender confidence in stabilized, income-producing logistics properties.

-

Portfolio flip: A Singapore-based investor sold a Dallas-area industrial portfolio to a local buyer, underscoring sustained demand for industrial assets and ongoing capital rotation in Texas markets.

🏬 RETAIL

-

Policy pushback: New York landlords are gearing up to challenge proposed commercial rent stabilization measures, warning the policy could disrupt leasing dynamics and deter investment.

-

Cannabis corner: A dispensary lease in Queens highlights continued retail demand from cannabis operators seeking footholds in high-traffic neighborhood corridors.

-

Net lease nudge: Single-tenant net lease retail remains resilient in 2026, with investors favoring stable, long-term income streams despite broader market uncertainty.

-

Desert deal: A Phoenix-area retail center traded for $10.8M, signaling steady investor appetite for well-located neighborhood retail assets.

-

Luxury lease-up: Gucci’s new Palm Beach storefront underscores the strength of ultra-luxury retail corridors as top brands double down on flagship locations

🏢 OFFICE

-

Federal underuse: Nearly 10,000 federal office spaces are operating below 60% utilization, highlighting widespread inefficiencies as agencies reassess their real estate needs.

-

LA refi: A Los Angeles office campus secured an $80M refinancing, signaling the lender's willingness to back well-positioned assets despite ongoing office market headwinds.

-

Leasing boom: AI companies are driving a resurgence in San Francisco office leasing, emerging as a rare source of expansion demand in a challenged market.

-

Houston suburban build: A new office development near Houston points to continued momentum for suburban, amenity-rich campuses attracting modern tenants.

🏨 HOSPITALITY

-

Napa resort buy: Blackstone acquired a luxury wine country resort north of San Francisco, expanding its hospitality portfolio with a high-end leisure asset.

-

London hotel sale: A Radisson Blu hotel in London traded to a private buyer, reflecting continued investor interest in core European hospitality assets.

-

Gaming growth: Regional demand beyond Las Vegas is driving strong revenue gains at gaming hotels, highlighting diversification across U.S. casino markets.

📈 CHART OF THE DAY

CRE Trivia (Answer)🧠

30 Hudson Yards in New York City — the skyscraper anchored by KKR and CNN — is among the most valuable, but the record for a single-asset U.S. office sale belongs to 1221 Avenue of the Americas, which traded for approximately $1.8 billion. However, the broader record for a U.S. commercial real estate transaction belongs to the Stuyvesant Town-Peter Cooper Village apartment complex in Manhattan, which sold for $5.45 billion in 2015 — the largest single real estate transaction in U.S. history at the time.

More from CRE Daily

-

📬 Newsletters: Stay ahead of the market with local insights from CRE Daily Texas and CRE Daily New York.

-

🎙️Podcast: No Cap by CRE Daily delivers an unfiltered look at the biggest trends—and the money game behind them.

-

🗓️ CRE Events Calendar: The largest searchable calendar of commercial real estate events—filter by city or sector.

-

📊 Market Reports: A centralized hub for brokerage research and market intelligence, all in one place.

-

📈 Fear & Greed Index: A fully interactive sentiment tracker on the pulse of CRE built in partnership with John Burns Research & Consulting.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |