Austin Apt Rents Are Down, Leading Nationwide Declines

Austin’s apartment rents have taken a nosedive, leading the nation with a -7.4% year-over-year drop in April. Here’s why rents are falling.

Jordan B. & Han-Gwon Lung

May 03, 2024

Together with

Good morning. The Austin metro has seen the nation’s sharpest decline among large metros. Meanwhile, U.S. port cities lead the nation in industrial property capitalization rates, followed closely by Midwestern markets.

Today’s issue is brought to you by Heritage Capital. Join the waitlist for priority access to their next industrial opportunity.

Market Snapshot

|

|

||||

|

|

*Data as of 5/02/2024 market close.

MULTIFAMILY METRICS

Austin’s Apartment Market Takes a Chill Pill

Austin’s apartment rents have taken a nosedive, leading the nation with a -7.4% year-over-year drop in April. Here’s why rents are falling.

The market: Just a few years back, Austin was the hot ticket for West Coast transplants, fueled by its vibrant economy and rock-bottom interest rates. Between late 2019 and mid-2022, the city’s home prices skyrocketed. But thanks to a massive wave of supply renters in the city are finally getting some relief.

Cooling down: The median rent in Austin ($1,470) fell by 0.2% in April and has now decreased by -7.4% over the past 12 months. Austin’s rent growth over the past year has fallen behind both the state (-2.7%) and national averages (-0.8%).

Source: Apartment List

It’s all about supply. Despite a strong job market, a surge in new multifamily units has tipped the scale towards oversupply. The southern U.S. saw a significant increase in new apartment completions, up nearly 72% year-over-year, contributing to the downward pressure on rents. In Austin, this was compounded by a dramatic increase in new construction during the pandemic’s peak growth years, leading to an eventual rent correction.

Zoom in: Austin leads the nation in issuing new home permits faster than any other large metro, stressing the important role new supply plays in managing long-term affordability. This trend is evident in many of the Sun Belt markets. Eight of the ten metros with the largest rent decreases—including Austin, Raleigh, Orlando, Jacksonville, Charlotte, Nashville, Phoenix, and Dallas—also topped the list for most new housing permits issued in 2023.

➥ THE TAKEAWAY

What they’re saying: It could be a few years before there’s enough demand to absorb the excess supply that’s overwhelming some metros, such as Austin. Additionally, the increasing difficulty in securing financing for new developments has led to a slowdown in the pipeline for future projects. This, along with other trends, will help the market reset in time. But the timeline remains unknown.

TOGETHER WITH HERITAGE CAPITAL

Investment Opportunity: Industrial portfolio with $1MM+ NOI

Welcome to Heritage Capital Group, a 3rd generation family office with over $750 million and 6 million square feet of assets under management.

For the first time in their history, they are offering the opportunity for accredited investors to join in their next acquisition. Highlights as follows:

-

Property: 212,000+ sq ft, multi-tenant, two-building portfolio in NE Indianapolis

-

Financing: Life insurance company with flexible, prepayment options

-

Occupancy: 100%, generating $1MM+ NOI at 8.6% cap rate

-

Lease Term: Weighted average of 2.87 years

-

Rent Upside: Potential 15-20% increase on renewal/turnover

-

Investor Returns: 8% preferred return, projected IRR of 16%

✍️ Editor’s Picks

-

Alternatives soar: Q1 of 2024 saw a 41% increase in sales volume for alternative real estate sectors, including medical offices and data centers, as reported by MSCI’s capital trends.

-

Cannabis reconsidered: The DOJ’s recommendation to reclassify cannabis as a lower-risk substance could significantly impact the real estate sector for marijuana businesses.

-

1% problems: The Dassault family is advancing its succession plan by preparing two fourth-generation heirs to join the supervisory board of their Paris-based real estate company.

-

REIT trends: Recent market data reveals that U.S. REITs raised $17.6B in 1Q24. $12.9B came from debt, and $3.7B came from follow-on common equity offerings.

🏘️ MULTIFAMILY

-

BTR boldness: Quarterra (QTRRF) and Invitation Homes (INVH) join forces in a JV, adding thousands of residences as BTR continues to grow rapidly.

-

The Golden Order: CA’s outmigration has officially ended, with the state adding 67.1K residents as SoCal sees over half of that growth (37K) in key counties like LA.

-

Affordable dilemma: Eagle Rock City Councilwoman Hernandez seeks a discretionary review for a local project threatening 17 rent-controlled units.

-

Risk, reward: Brookfield (BN) repays riskier tranches in full on $675M in San Francisco apartment loans, resulting in a 45% loss on its initial investment.

-

Rooting around Renton: Waterton acquires a 186-unit complex in Renton, WA, its third purchase in the rainy state in a year.

🏭 Industrial

-

Leasing boom: CBRE projects that 2024 will be the third-highest year on the record books for industrial leasing, with 413MSF released in 2023, even as supply is expected to drop.

-

Successful expansion: East Capital Partners in Darien, CT acquired 8 warehouses and a storage yard near Medley for $17.5M.

-

New development: A $55M industrial development is coming to Sanger’s PNK Group project, adding 500KSF to the already booming North Texas market.

🏬 RETAIL

-

Brick-and-mortar ruins: UBS estimates that up to 45K U.S. retail stores may close by 2028 due to growing online shopping preferences and higher brick-and-mortar operational costs.

-

Living like the 1%: Nationwide, online grocery sales are set to grow at a 4.5% CAGR over the next few years, outpacing in-store sales (1.3%) to hit $120B annually by 2028.

🏢 OFFICE

-

CBD complications: The Chicago CBD office market worsened in 1Q24, with leasing dropping to 1.1MSF alongside -1.4MSF net absorption, mainly in Class A properties.

-

Don’t need it: The U.S. Nuclear Regulatory Commission halves its office footprint at Peachtree Center in Atlanta amid downtown market challenges.

-

High-end hustle: Boston Properties (BXP) sees positive leasing trends with the highest lease lengths in years, boosting leasing volume and rates.

🏨 HOSPITALITY

-

Music City mood: Host Hotels & Resorts (HST) acquired 1 Hotel Nashville and Embassy Suites Downtown for $530M.

-

Hotel hurdles: Q1 U.S. hotel performance was mixed, and included a 2.2% drop in March RevPAR thanks in part to Easter.

-

Building dreams: VICI Properties (VICI) agreed to provide $700M in financing for Venetian Resort enhancements, marking the venue’s 25th birthday.

INVESTMENT INSIGHTS

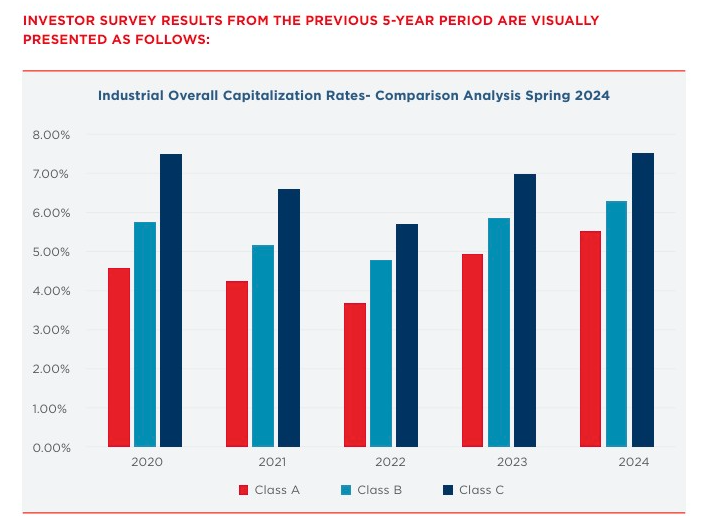

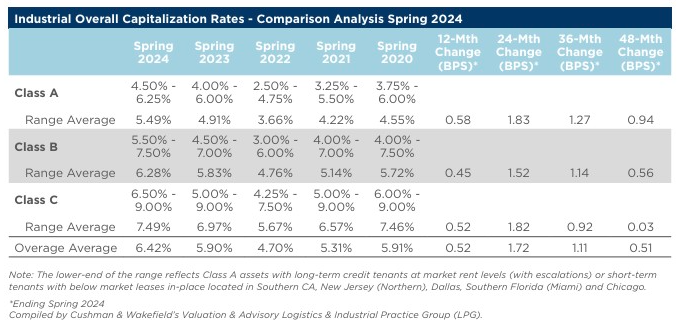

Port Cities Lead in Class A Industrial Capitalization Rates

According to Cushman & Wakefield’s Industrial Investor Survey for Spring 2024, port cities are commanding higher capitalization rates for Class A properties, thanks in part to nearshoring.

By the numbers: Activity in the 10-year US Treasury resulted in higher yield rates and cap rates, as well as a higher cost of capital. Average Class A cap rates rose by 58 bps YoY. Class B assets rose by 45 bps, while Class C was up by 52 bps. Overall rates for Class C assets are 121 bps higher than Class B industrial product.

Emerging Midwest: The survey reveals that Midwest markets are gaining traction among investors for Class A properties, with cap rates remaining competitive. Midwestern assets continue to attract both institutional and private investors who recognize the value and potential in the heartland of the U.S. industrial landscape.

Stable interest rates: Most investors do not foresee higher interest rates. Their current yield rates factor in any potential near-term rate hikes, providing a sense of stability and predictability for long-term holdings. This steady outlook on rates bodes well for investors seeking reliable returns on their Class A properties.

Confident choices: Despite a hawkish and largely unhelpful Federal Reserve, investor confidence is solid for Class A properties. Buyers are optimistic about the future performance of high-quality assets, revealing a positive sentiment towards industrial even in turbulent times.

➥ THE TAKEAWAY

Strategic outlook: Outside of the Midwest, investors foresee strong demand for industrial in coastal, Southwest, and Southeast markets. Class A assets in core markets command aggressive rates, while Class B and C properties near urban centers are sought for yield growth. With strong fundamentals, industrial market activity focuses on value-add projects, shorter leases, and competitive financing strategies to maximize returns.

📈 CHART OF THE DAY

Express, which filed for Chapter 11 bankruptcy, is planning to shutter nearly 100 locations by June 30th, mostly in CA, NY, NJ, TX, and FL making up nearly half of all closings. Express is the latest big-name retailer to file for bankruptcy, after 99 Cents Only Stores made headlines earlier in April.

What did you think of today’s newsletter? |