5 Trends to Watch in Real Assets for 2024

2023 experienced a decline in real estate, with lower asset values and transactions. Investors anticipate a market rebound, guided by five key trends identified by MSCI.

Han-Gwon Lung & Jordan B.

December 15, 2023

Together with

Good morning. Looking ahead to 2024, investors are hopeful for stabilized prices and a return to normal market activity. Meanwhile, Manhattan rents dropped for the first time since August 2021, a sign that the apartment market is experiencing more than just seasonal declines.

Today’s issue is brought to you by BetterPitch.

👋 First time reading? Sign up.

🎁 Want free merch? Share this.

Market Snapshot

|

|

||||

|

|

*Data as of 12/14/2023 market close.

YEAR-END REVIEW

5 Trends to Watch in Real Assets for 2024

2023 was a challenging year for real estate, with widespread declines in asset values and reduced transaction volumes. Looking ahead, investors are hopeful for stabilized prices and a return to normal market activity. Here are five key trends to watch, according to the MSCI research team.

1) Anticipating distressed sales: In 2023, distressed sales in the U.S. real estate market were only 1.7% of investments despite growing distress since 2022. With many loans from 2021 and 2022 nearing maturity and facing higher interest rates and lower valuations, more forced sales are expected. The current lending environment is more conservative, with declining loan-to-value ratios. Over USD 2 trillion in loans will mature by 2027, creating opportunities for investors. This downturn differs from post-2008, offering more flexibility for lenders and borrowers due to new investment strategies.

Looming US loan maturities

Loan maturities by origination vintage. Loans outstanding at Q4 2023. Data as of Dec. 5, 2023. Source: MSCI Mortgage Debt Intelligence

2) Mind the gap: Global real estate transactions are currently stalled due to a significant gap between buyer and seller price expectations, exacerbated by rising interest rates. This gap, particularly notable in European and North American office markets, has widened significantly, as shown by the MSCI Price Expectations Gap. Market liquidity will only improve with more consensus on property pricing, likely dependent on clearer expectations about future interest rates. Until then, caution is advised in this uncertain market.

Gap in buyers’ and sellers’ pricing has widened

Office properties only. Source: MSCI Price Expectations Gap, RCA Hedonic Series

3) Expect a double dip: The recent volatility in commercial real estate makes predicting market trends difficult. A potential second downturn, influenced by high interest rates and global economic slowdown, is particularly evident in the office sector. The MSCI Price Expectations Gap indicates that many market segments, especially offices, may need further price reductions to regain liquidity. This could lead to additional valuation declines. Markets like Australia and Ireland, heavily invested in offices, might see significant impacts on capital growth if these adjustments occur and transactions increase.

First dips in property performance already experienced

Capital value weights as of Q3 2023. Source: MSCI UK Quarterly Property Index

4) Shifting risk/return landscape: In the last 18 months, global real estate investment has shifted, with economic and financing changes affecting values across asset classes. These shifts, influenced by debt financing, interest rates, and rising risk-free-rate benchmarks, have led investors to reassess their capital allocations. There’s a focus on the varied impact on different market segments and the risk spectrum from core to opportunistic strategies.

Core investments have lagged so far in the current downturn

Fund returns. Source: Burgiss Global Real Estate Funds Index, MSCI Global Property Fund Index (Core Funds)

5) Rising insurance costs: Climate change is increasingly affecting real estate investments, with 2023 poised to be the warmest year on record. The MSCI Climate Value-at-Risk Model indicates that up to 5.5% of the MSCI Global Annual Property Index faces transition risk, and 3.0% is at risk from physical impacts in the coming years. A direct consequence for investors is rising insurance costs due to more frequent and severe weather events. Data from the MSCI U.S. Quarterly Property Index shows insurance costs more than doubling in five years to September 2023, particularly in high-risk states like Florida and California.

US insurance costs have increased, particularly in high-risk states

Insurance costs as share of income receivable. Source: MSCI U.S. Quarterly Property Index

➥ THE TAKEAWAY

Big picture: The 2024 commercial real estate market is navigating a mix of challenges and opportunities. Expectations of increased distressed sales due to maturing high-risk loans and a notable pricing gap, especially in office markets, are key issues. The office sector might see further declines, influencing the broader market. Shifting investment dynamics are altering risk-return profiles, compounded by escalating insurance costs impacting property values and expenses. Despite these hurdles, clearer interest rate trends offer hope for renewed market liquidity and balanced property pricing.

Which Trend Will Most Impact the CRE Market in 2024? |

TOGETHER WITH BETTERPITCH

Focus on your deal, not your deck

Does your firm’s pitch materials need a facelift? From fundraising to track records, BetterPitch offers a proven done-for-you pitch.

BetterPitch completes all design, copywriting, and market research. That’s right, they research the most compelling data to illustrate and support your investment thesis. Your days of moonlighting as a designer and analyst are over.

BetterPitch is the plug-and-play option to deliver an institutional quality deck that leads to a more effective pitch. The best part? They deliver the final product in a PowerPoint file for you to use on future deals!

TRENDING HEADLINES

-

Fort Worth’s frontier: Recent Houston transplant Shams Merchant moved his real estate law practice to Fort Worth, citing the city’s booming growth and strong economy as key factors.

-

Bursting balloons: The US built over 360K apartment units this year, exceeding the total from 2022, and resulting in a decrease in rental growth.

-

Agents without salaries: Redfin (RDFN) is shifting to an all-commission model, eliminating salaried agents to boost revenue and cut costs.

-

Retail investors: The rush of retail investors into alternatives is accelerating, with assets of $1–$5M, which have gone up by nearly 60% in the past 15 years.

-

Changing of the guard: Cushman & Wakefield’s (CWK) former Atlanta office leader and US multifamily sales head has departed, replaced by a senior executive from Greystone.

-

Magin in the Midwest: Developer and manager of single-story build-to-rent apartment homes, Redwood Living, Inc., is looking forward to 2024 with confidence.

-

Digital divide delights: Prince William County, VA, approves world’s largest data center hub at 34 data centers with 1.7 GW capacity (and $400M in expected annual tax revenue).

-

Educational endeavor: Elon Musk plans to start a university in Austin, TX, with a $100M donation to create a primary and secondary school focused on STEM education.

-

From gridiron to gold: Franchises are transforming into real estate ventures as sports teams aim to generate revenue from mixed-use developments surrounding their stadiums.

-

Unlocking land value: The highest and best-use concept in the CRE industry maximizes productivity and profit for land, regardless of its current use.

-

Construction material prices: The Bureau of Labor Statistics (BLS) reported that construction materials prices were up 0.2% MoM in November.

-

Adapting to the new: CRE and investment property sectors are shifting post-pandemic, with a retail rebound, changing investor sentiment about climate risks, and eroding affordability.

PROPERTY REPORT

Manhattan Apartment Rents See First Year-Over-Year Drop Since 2021

Tenants are regaining control. For the first time since August 2021, Manhattan rents have decreased year-over-year last month, following two years of continuous growth.

Big Apple DVs: According to appraisal firm Miller Samuel for Douglas Elliman, median rents in NYC slipped 2.3% YoY to $4K and fell 9% since August. On a MoM basis, median Manhattan rent slipped 9% since August. Brokers believe the slide indicates that regular seasonality (i.e., lower demand in the winter) has returned after the COVID-19 pandemic upended normal leasing patterns across the city and the country.

Borough by borough: Miller’s report is not citywide and does not consider rent-regulated units, which make up half of the city’s rentals. In Northwest Queens, for example, median rent slipped 0.3% YoY to $3,175, while Brooklyn rents actually rose 6% YoY to a median of $3,495. And November’s median rent was effectively the same as October’s.

From the horse’s mouth: “In November, what we saw were renters really taking their time and looking at multiple units and different neighborhoods — just trying to find the best value,” said Hal Gavzie, a Douglas Elliman broker. Meanwhile, Jonathan Miller, the author of the report, stated that the decline suggests rents are falling faster than normal seasonality can explain.

➥ THE TAKEAWAY

Too much of a good thing: Manhattan’s downward trend may very well continue into 2024, especially if the Fed’s forecast for rate cuts holds true.“I think there is more room for further declines into next year,” said Miller. Cheaper mortgages should also significantly drive up homeownership rates compared to this year, which should in turn drive down demand for rentals.

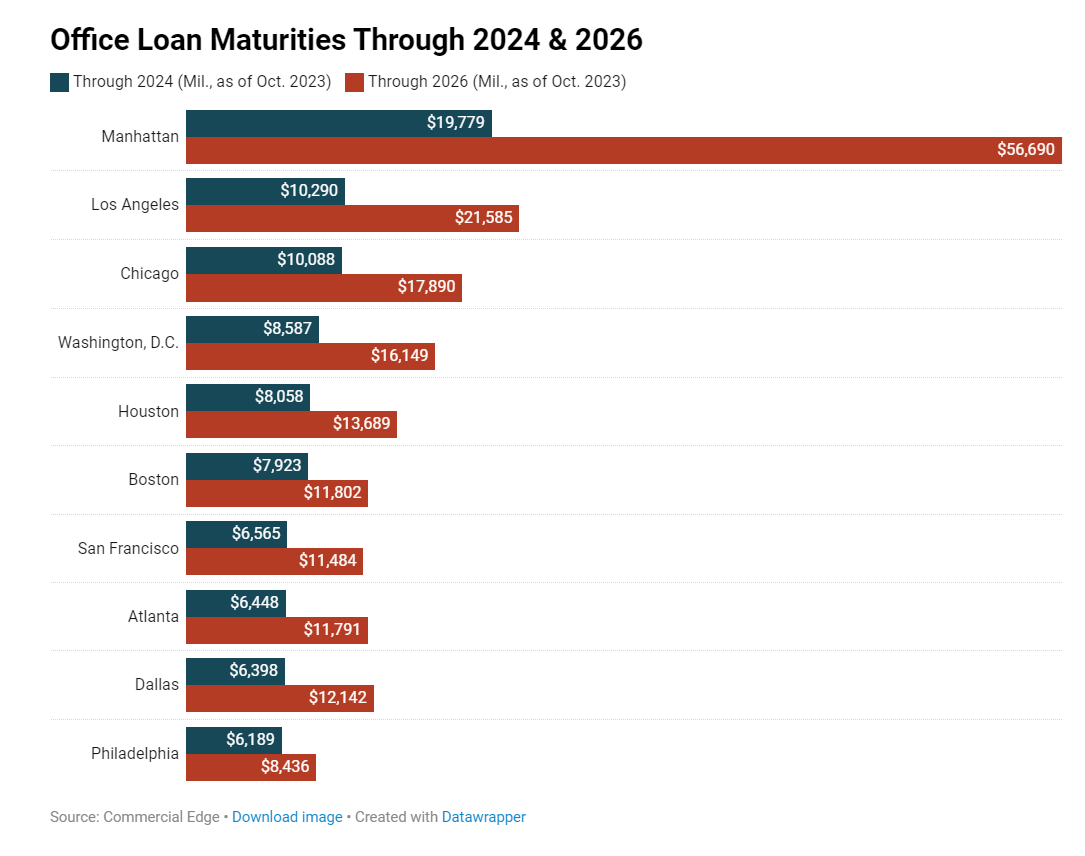

CHART OF THE DAY

From 2024 to 2026, a lot of office loans are coming due. Big gateway cities across the country, like NYC, LA, Chicago, DC, and Houston, will see billions in office loan maturities just in 2024. Manhattan, in particular, will have to deal with nearly $20B in maturing office loans next year, and another $37B by 2026.

What did you think of today’s newsletter? |