2024 Apartment Forecast Remains Strong Despite Twists

Plus: Moody’s 2024 forecast predicts a challenging year for commercial real estate financing, with high interest rates impacting the CMBS market.

Han-Gwon Lung & Jordan B.

December 12, 2023

Together with

Good morning. The 2024 apartment market is expected to have strong fundamentals despite ongoing economic uncertainties. Meanwhile, increased utilization of CMBS loans by US commercial property owners is expected in 2024 due to tighter lending standards by banks and elevated interest rates.

Today’s issue is brought to you by Yieldstreet—build a portfolio beyond the stock market on the largest private market investing platform.

👋 First time reading? Sign up.

🎁 Want free merch? Share this.

Market Snapshot

|

|

||||

|

|

*Data as of 12/11/2023 market close.

MARKET OUTLOOK

2024 Apartment Forecast: Strong Fundamentals Despite Twists & Turns

Despite concerns about uncertainties and a potential recession, the 2024 forecast for the rental market shows robust fundamentals for multifamily.

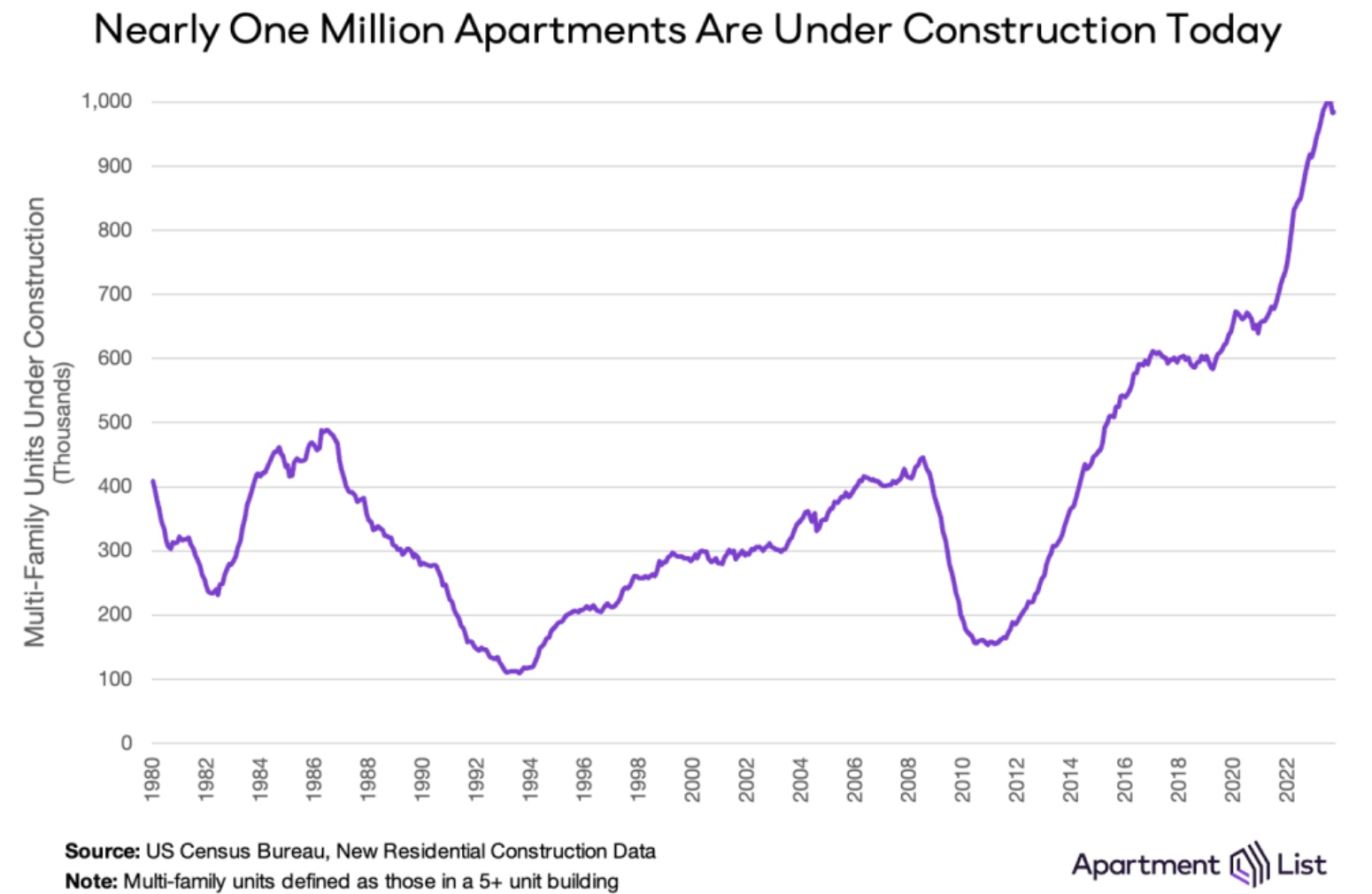

Supply surge predictions: The number of new multifamily apartment units under construction reached a record 1M in late 2023. Origin Investments predicts a slowdown in new starts next year due to a lack of funding and ongoing uncertainties. Yardi Matrix analysis also aligns with this prediction.

Rent growth outlook: Rent growth, which cooled due to easing demand and rising supply, is expected to recover slightly in 2024 but remain in the low single digits. Negative rent growth is projected to return to the historic norm within a 2–4% range by 2H24, similar to 2022 levels.

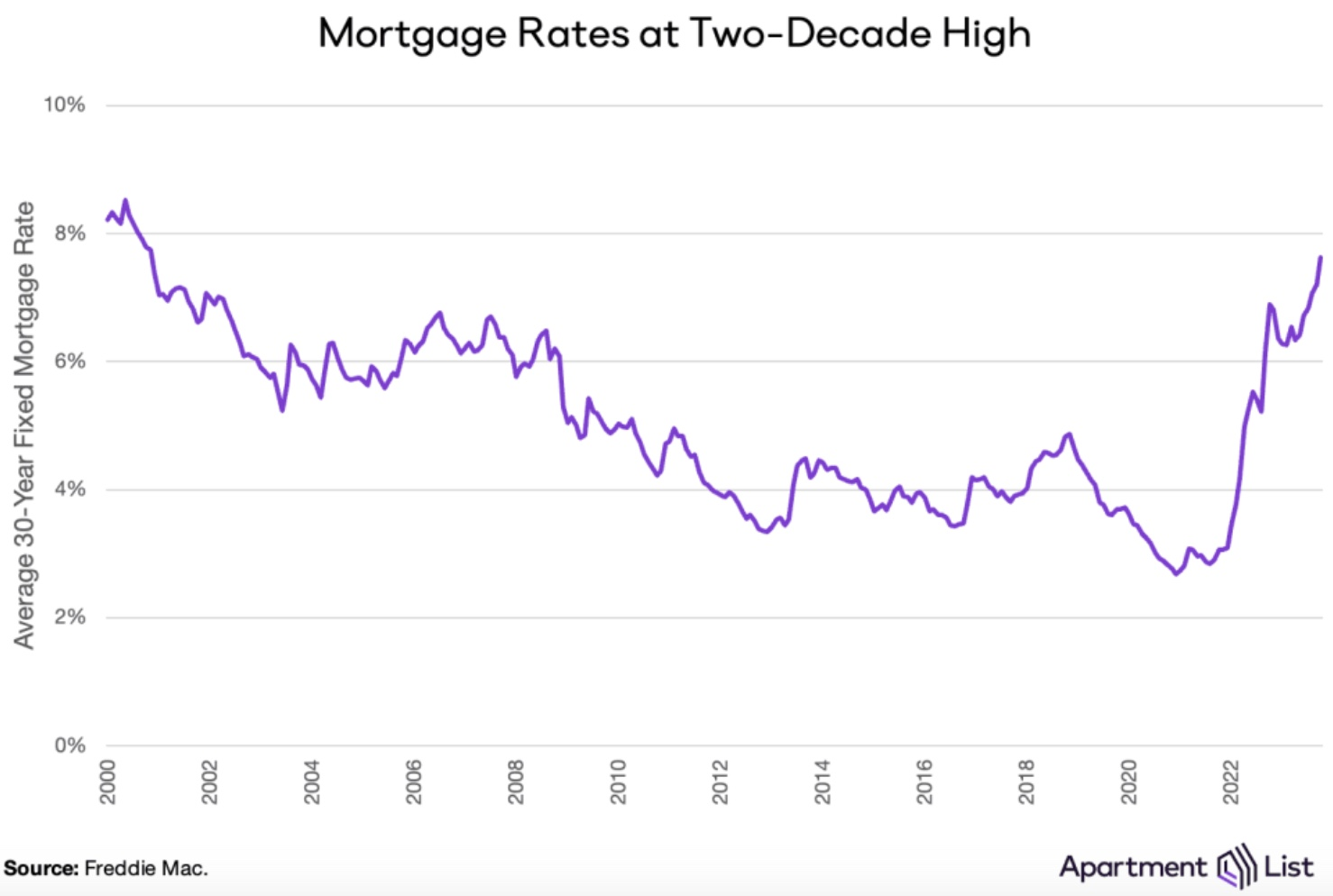

Homeownership barriers: Systemic barriers to homeownership, such as high prices and spiking mortgage rates, contribute to the long-term renter trend. Few buyers can afford homes and existing owners are reluctant to sell. Consensus expectations suggest mortgage rates will ease in 2024 but won’t significantly impact the for-sale market.

➥ THE TAKEAWAY

New realities and opportunities: Next year’s apartment forecasts reveal new realities and new opportunities. Hybrid work, driven by the pandemic, will become the new normal, creating demand for rentals that accommodate flexible work-life balance. And insurance, which shot up in 2022 due to natural disasters, may stay high. Despite this, ongoing opportunities and potential returns, particularly in senior debt and preferred equity, are attracting plenty of attention.

TOGETHER WITH YIELDSTREET

Alternative Investments to Curb Inflation

Higher interest rates and market volatility are making it harder for investors to find above-market returns. Diversify your portfolio with Yieldstreet’s robust private market offerings. Through their platform, you can invest in various asset classes, including art, venture capital, private equity, and real estate.

Since its inception, Yieldstreet has unlocked over 500 private market opportunities for investors and invested over $4B on its platform.

Get started at Yieldstreet.com to learn more about what private market investing can do for you and your portfolio.

TRENDING HEADLINES

-

Real estate rumble: Florida’s China property crackdown law disrupts deals, and major real estate players are lobbying for changes to the restrictive legislation.

-

Property pricing in the balance: US CRE valuations dropped 3% in November, down 10% YoY, but may be stabilizing due to a recent rally in bonds.

-

Pandemic pressures: Mall landlord PREIT files for bankruptcy for the second time, planning to reduce its overall debt by $880M.

-

Flipping the script: Goldman Sachs (GS) advises clients to stop shorting UK property stocks as the housing market stabilizes while predicting a Bank of England rate cut in Auguset.

-

Win-win situation: Development Deal: Relevant Group sells the Morrison Hotel in LA to the AIDS Healthcare Foundation for $12.4M, resolving a default on Relevant’s loan.

-

Can’t make this up: Adam Neumann’s latest venture, Flow, a property management startup, is set to launch its first property next year, valued at $1B after receiving a $350M investment from Andreessen Horowitz.

-

Diamond in the rough: Carmel, IN, is attracting big-city buyers from LA and Austin due to lots of exciting development and positive rankings in numerous top 10 lists.

-

Employment puzzle: November employment levels in multifamily were below last month’s levels as total non-farm employment rose by 199K jobs and the US unemployment rate fell to 3.7%.

-

Searching for deals: Kennedy Wilson (KW) sells Glendale office property for $60M, a 60% decrease, setting a new benchmark for falling office values.

-

The plot thickens: Ben Ashkenazy secretly recorded lender Rexmark during a dispute over the $1B Union Station development in Washington, DC.

-

Signs of softening: Property insurance rates in the US are expected to shoot up by single digits next year, indicating a possible softening in the market.

-

From Cubicles: Indoor vertical farming in CRE spaces can fill vacant offices and provide fresh, locally grown food. However, high costs remain a significant obstacle.

-

Retail rebound: Retail real estate professionals express confidence in retail demand despite challenges in building new properties.

CMBS SENSATION

Moody’s Expects More CRE Owners to Turn to CMBS Lenders in 2024

Moody’s 2024 forecast predicts a challenging year for commercial real estate financing, with high interest rates impacting the CMBS market, reducing transaction volumes, and increasing loan default risks.

Setting the scene: Throughout 2023, the CRE landscape faced headwinds due to high interest rates and declining property values. Banks responded by tightening lending criteria, leading many CRE owners to consider CMBS as a viable alternative. These securities pool individual loans and offer appealing yields and credit quality to investors. And despite a dip in multi-loan and single-asset CMBS issuance in early 2023, the latter half saw a resurgence in these securities, alongside a rise in CRE collateralized loan obligations (CLOs).

Challenges in refinancing: Higher interest rates have compressed loan-to-value (LTV) ratios from an average of 60% to 55%. This uptick has made it tougher for borrowers to maintain adequate debt-service coverage ratios (DSCR), leading to a spike in interest-only loans. Office buildings, in particular, have felt the brunt of this shift, with a significant drop in their refinancing rates.

➥ THE TAKEAWAY

CMBS outlook: Moody’s expects a rise in CMBS issuance in 2024 due to tighter bank lending. However, there’s a significant risk of defaults, especially in the office sector, with about 20% of maturing CMBS loans at high default risk. This could increase the delinquency rate to 7.05%. Despite these risks, there’s optimism for market recovery through strategic resolutions and loan payoffs.

QUICK HITS

📖 READ: The term “American Dream” entered the national lexicon during the worst part of the Great Depression. But nearly 100 years later, that dream—which depends mostly on homeownership—is more out of reach for most Americans than ever.

🎧 LISTEN: Kimco Realty (KIM) President and CIO Ross Cooper discuss the evolving partnership between retail and mixed-use property owners and tenants, the benefits of JVs, the synergy between retail and e-commerce, and unconventional investment opportunities.

🖥️ WATCH: Bloomberg’s Carol Massar and Tim Stenovec discuss the challenges of finding office space in Miami since relocating and the outlook for CRE during the Bloomberg New Voices panel.

CHART OF THE DAY

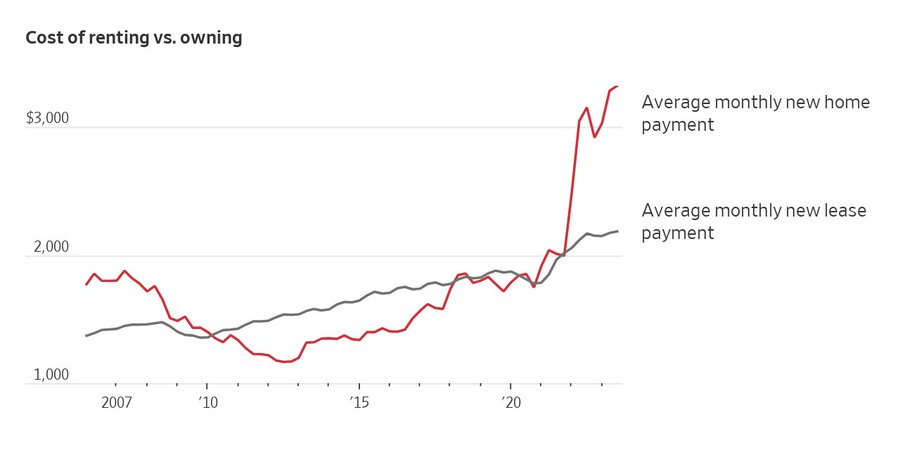

Note: The data assumes a 10% down payment and includes private mortgage insurance. (CBRE Research, US Census Bureau, Realtor.com, FHFA)

Why would anyone want to buy a home when renting is so much cheaper? Even during the worst parts of the Great Recession, the gap between average monthly new home payments nationwide and average monthly new lease payments was around half the current gap. Since 2022, average monthly new home payments have shot up to the $3,000/mo+ mark, while the average monthly new lease payment is nearly $1,000/mo less.

What did you think of today’s newsletter? |