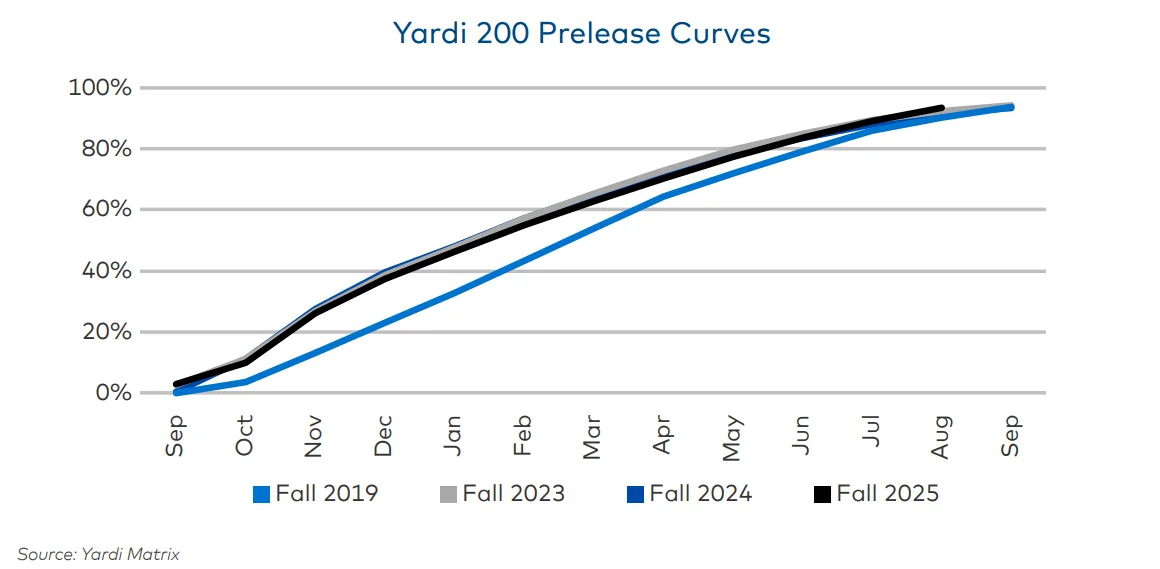

- Preleasing reached 93.7% in August, above both last year’s level and Fall 2024’s final occupancy.rn

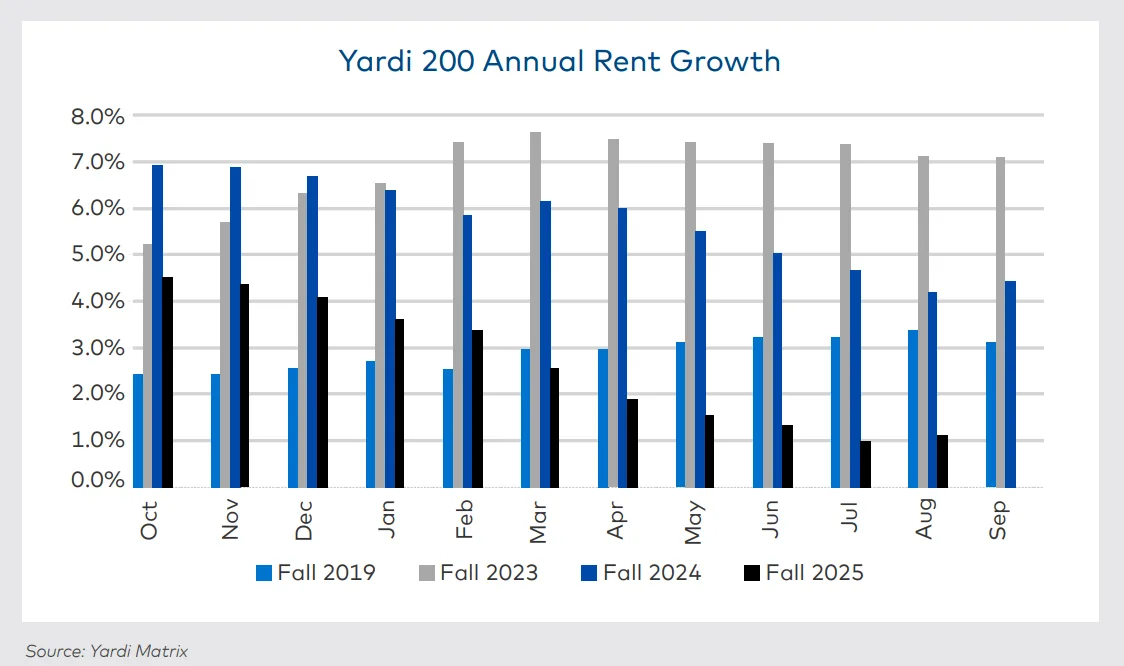

- Rent growth has cooled to 1.1% YoY, with average rents down from the March peak.rn

- New supply in markets like Arizona, Tennessee, and Central Florida is dampening both rent growth and leasing momentum.rn

- Student housing sales remain active, though mostly in single-asset trades rather than large portfolios.rnrnrn

Preleasing Momentum Ahead of Last Year

Leasing activity across the Yardi 200 points to another strong year, according to the National Student Housing Report from yardi matrix. Preleasing reached 93.7% in August, two percentage points higher than last year. It was also slightly above the final occupancy level recorded in September 2024.

More than a third of markets—36 in total—were nearly full at 99% or higher. This group included large universities with limited student housing stock such as UCLA, San José State, and Florida Atlantic.

The number of schools below 85% preleased fell to 21, down from 35 last August. A few large markets, however, are lagging. Purdue, Georgia Tech, Arizona, Michigan, and Texas A&M all trail last year’s pace by several points due to significant new supply.

Rent Growth Slows Into Fall

Occupancy is strong, but rents have been harder to push this cycle. Average asking rents were $903 per bed in August. That represents a 1.1% year-over-year increase but a 1.7% drop from the March peak of $919.

Since October 2024, rent growth has averaged 2.7%, a sharp slowdown from 5–7% in the two prior cycles.

Some markets did accelerate late in the season. Florida turned around from a slight decline to an 8.4% gain by August. The University of Washington also improved, climbing from a 3.5% decline to a 2.6% increase.

For others, early momentum faded. Arizona rents swung from double-digit growth at the start of the cycle to an 8% decline in August. Tennessee, which had posted two years of outsized gains, dropped 8.3% by the end of the season.

Market and Investment Trends

The rent slowdown is closely tied to supply. Markets with heavy construction pipelines—such as Central Florida, Clemson, and Arkansas—are struggling to hold rents. In contrast, schools with limited new stock, like Virginia Tech and Florida, have stayed nearly full and achieved growth above 6–8%.

Capital markets remain active but are quieter than last year. Seventy-one properties have traded so far in 2025, compared with 86 at this time in 2024. Last year’s volume, however, was boosted by a 19-asset portfolio sale. Activity this year has focused on single-asset and small portfolio transactions.

Outlook

Final occupancy for 2025–26 is expected to land slightly higher than last fall. This reinforces student housing’s resilience, even as rent growth cools. In supply-heavy markets, leasing velocity will be more important than rental rate increases. Stabilized core assets should continue to benefit from tight supply pipelines.

Longer term, enrollment is the main risk. Funding constraints and projected declines in international students could reshape demand, especially at schools with heavy reliance on global enrollment.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes