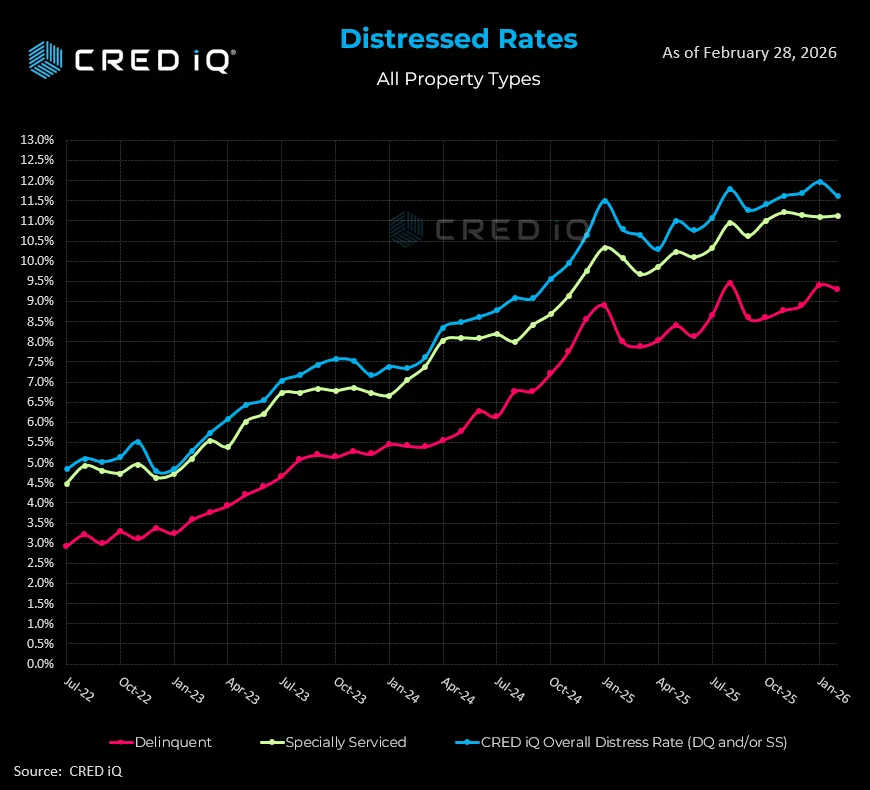

- Special servicing rate in commercial real estate hit 11.1% in February 2026, nearly the highest since the GFC.

- Overall CRE distress rates remain above 11%, reflecting sustained market challenges.

- Office and multifamily loans continue to drive distress, with office delinquencies reaching double digits.

- CRED iQ expects elevated rates through mid-2026, with gradual improvement possible in the year’s second half.

Distress Cycle Persists

Special servicing continues to trend near record highs in the commercial real estate market, according to the latest CRED iQ data. In February 2026, the special servicing rate climbed to 11.1%, the second-highest level since the Global Financial Crisis. While the overall distress rate dipped slightly to 11.6%, measured improvement remains elusive as delinquency rates remain stubbornly elevated.

The overlap in special servicing and delinquency rates signals a maturing distress cycle. Many loans that entered special servicing over the last year now face resolution, a factor pushing delinquencies upward even as new special servicing inflows slow.

Mixed Economic Signals

Broader economic conditions present both relief and new headwinds. The 10-year Treasury rate dropped to around 3.94%, easing some refinancing pressures, and the Fed’s benchmark rate cuts are helping on the margin. Inflation shows steady moderation, but the labor market is losing momentum, with a recent rise in unemployment and cooling job growth.

Weakness in jobs impacts multifamily and retail fundamentals especially, amplifying property-level risk in these sectors, even as several major US markets continue to report historically strong renter demand despite broader economic uncertainty.

Office and Multifamily Drive Distress

Office remains the most distressed major property type, with double-digit delinquency rates common in CMBS pools. Multifamily faces ongoing stress, particularly from 2021-2022 floating-rate bridge loans, though lower floating-rate benchmarks are offering some relief. Private-label CMBS issuance lags last year’s pace as lenders remain selective.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

What to Watch Through 2026

CRED iQ expects overall distress rates to remain between 11% and 12.5% through mid-2026. Conditions may improve later in the year. Meanwhile, a large maturity wave is approaching. Many CMBS and CRE CLO loans originated before inflation will soon require refinancing. This wave will test lenders and borrowers across the market. Office distress could worsen before stabilizing. Special servicing rates in the sector may approach 14%. However, multifamily conditions may improve if borrowing costs continue to decline. Lower rates could ease pressure on floating-rate loans.

The path forward will involve a protracted workout cycle, shaping the trajectory of special servicing and market recovery into 2027.