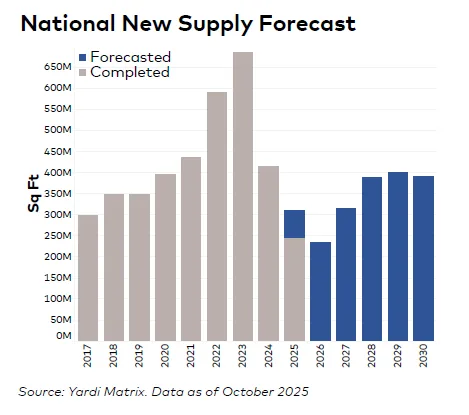

- Small-scale industrial properties (under 100K SF) are thriving, with a 16% Y-O-Y increase in development starts through Q3 2025, even as large-scale construction pulls back.

- Investor interest in the segment is rising, with average sale prices for smaller assets growing 10.6% Y-O-Y, far outpacing larger property price growth.

- Miami led the nation in industrial rent growth (8.9% Y-O-Y) in October, while Atlanta’s data center boom is redefining its industrial landscape.

A Growing Niche

As broader industrial development decelerates, small-scale projects are bucking the trend, reports Yardi Matrix. According to the report, 340 new facilities under 100K SF broke ground through Q3 2025—up 16% from the same period last year. This contrasts sharply with a 48% decline in new starts for facilities over 100K SF since 2022.

Why It’s Working

Urban infill, flexible layouts, and demand from light manufacturing and last-mile delivery providers are fueling interest in smaller spaces. But delivering these projects isn’t easy. Developers face high land costs, zoning restrictions, and construction hurdles—especially in dense urban markets.

Still, investors are taking notice:

- Sale prices for industrial buildings under 100K SF rose 10.6% Y-O-Y.

- By comparison, properties between 100K SF and 1M SF only saw a 3.5% increase.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Market Performance Snapshot

National average rent hit $8.73/SF in October, up 5.7% Y-O-Y, with a vacancy rate of 9.6%.

Miami continues to stand out:

- In-place rent: $12.91/SF

- Y-O-Y rent growth: 8.9%

- Recent leases: $16.41/SF average

- Vacancy: 11.2%, due to a wave of new deliveries.

Other top performers in rent growth include:

- Atlanta: 8.8%

- Philadelphia: 7.6%

- Dallas-Fort Worth: 7.2%

Supply Watch

Nationally, 352.9M SF of industrial space is under construction, representing 1.7% of total stock. Leading the charge:

- Dallas (30.9M SF)

- Houston (21M SF)

- Phoenix (18M SF, 4.1% of stock)

Atlanta, meanwhile, is emerging as a data center hub. More than 70% of its current industrial construction—over 7.7M SF—is dedicated to data centers, as demand from AI firms and cloud providers surges.

Investment Outlook

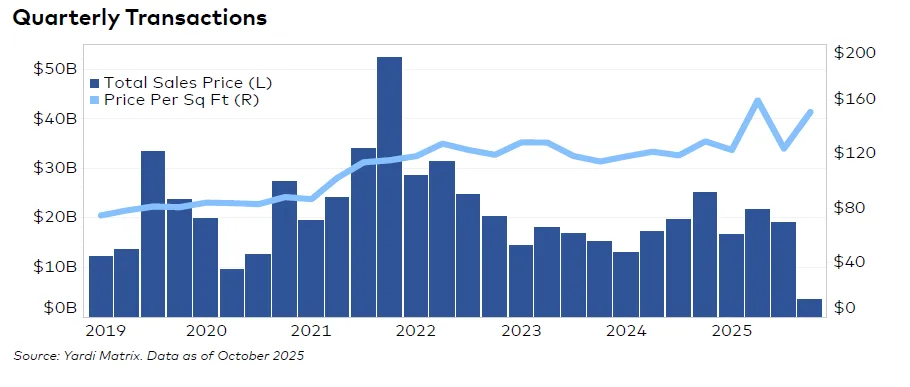

Through October, $61.8B in industrial transactions closed nationally at an average price of $136/SF.

Markets seeing major activity:

- Detroit led in price/SF at $610, followed by Orange County ($303) and Los Angeles ($276).

- Charlotte saw notable movement in submarkets like Iredell County, with Morgan Stanley-owned Eaton Vance acquiring the Statesville Operations Distribution Center for $139M, the area’s largest deal this year.

What’s Next

Expect continued momentum in small-scale industrial as same-day delivery trends, reshoring of manufacturing, and e-commerce sustain demand. However, challenges in land availability and construction feasibility will keep the supply constrained, potentially supporting continued price growth.

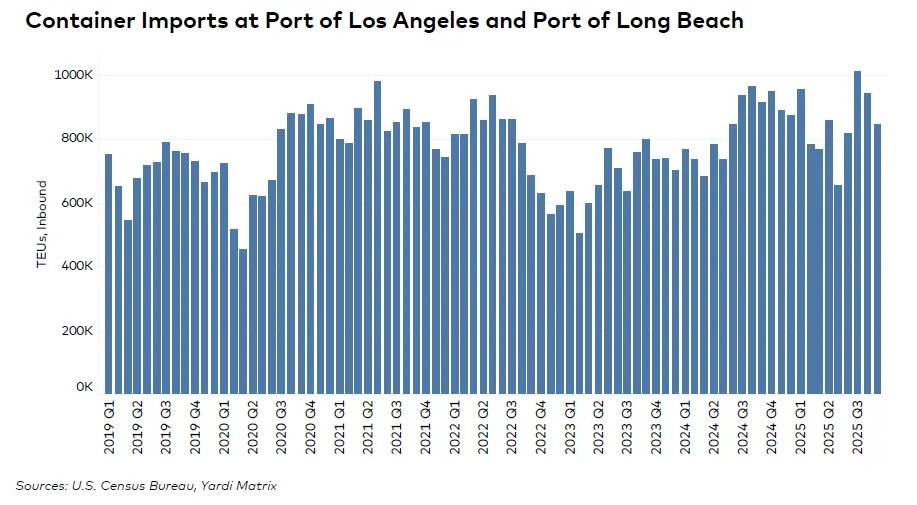

Meanwhile, the rise of data centers and shifting port dynamics (like softening volumes in Southern California) are reshaping regional industrial strategies heading into 2026.