- Self storage rents posted 0.3% annual growth in December, signaling further moderation.

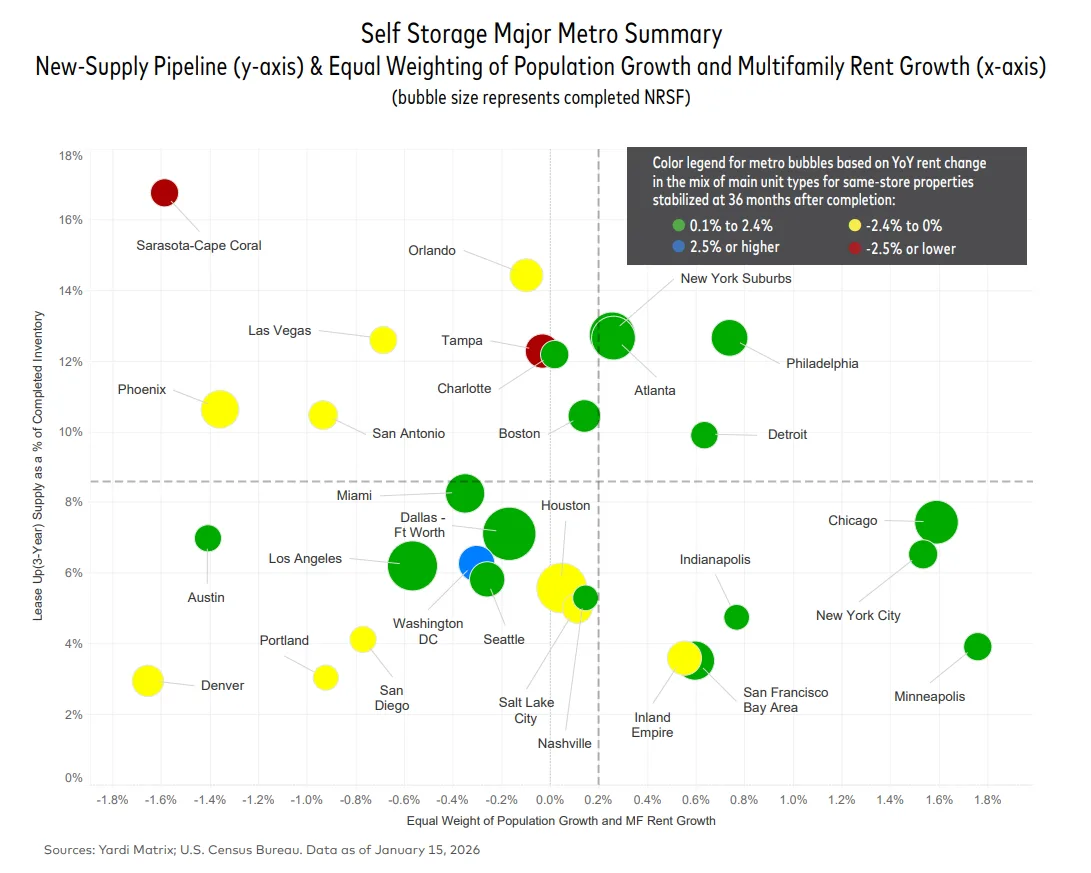

- The development pipeline remains flat, with under-construction supply at 2.7% of existing inventory.

- Markets with strong multifamily demand—like New York and D.C.—outperformed despite new deliveries.

- Winter seasonality and low home sales are weighing on self storage demand and investor sentiment.

Investor Caution Defines 2026

The US self storage market enters 2026 under more conservative sentiment as occupancy, revenue, and rent growth face pressure. According to the latest Yardi Matrix report, consistently low home sales and pockets of elevated supply are restraining demand and shaping a cautious investment climate. Investors are adjusting underwriting assumptions amid gradual and uneven performance across metros.

Despite wavering fundamentals, capital for self storage remains available for experienced owners and operators. However, deal activity is hampered by loan extensions and widespread use of bridge lending, keeping transaction volumes below historical norms.

Rent Growth Continues to Cool

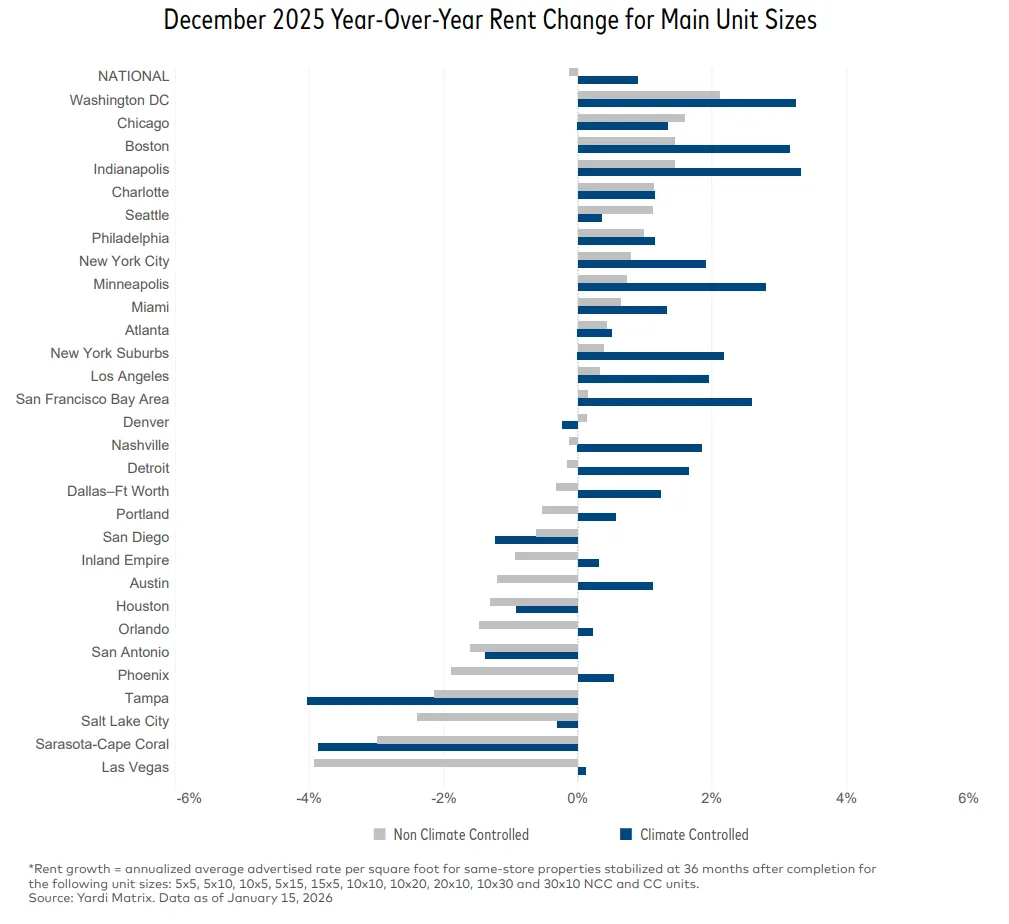

National self storage rents rose 0.3% year-over-year in December 2025, reaching $16.32 PSF. Growth continued but slowed from the previous quarter. Half of the top 30 metros posted weaker rent gains compared to November. Rents for climate-controlled units increased in 23 of the top 30 metros. Non-climate-controlled units saw flat growth or slight declines.

Month-over-month, the national average rate dipped 0.3% from November. This seasonal drop reflects weaker leasing demand during winter. Only five metros, including New York City and Los Angeles, posted monthly rent increases in December.

Supply Pipeline Stable but Varies by Metro

The under-construction self storage pipeline held steady at 2.7% of national inventory, or roughly 54.3M net rentable square feet. Supply growth remained flat compared to the previous month. Sun Belt metros like Sarasota-Cape Coral, Phoenix, Tampa, and Miami saw elevated construction activity. Developer interest remains strong, even amid rising costs and tighter underwriting.

Local trends show mixed momentum. Nashville, San Antonio, and Philadelphia posted construction declines. Miami, Las Vegas, and Tampa recorded year-over-year increases.New York suburbs continued to lead on rent growth. Strong multifamily and housing demand support performance, even after years of heavy supply additions.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Demand and Rate Performance Linked to Multifamily Trends

Rent gains increasingly track local population and apartment growth. Supply alone no longer drives performance. Strong multifamily markets show better rent trends. New York City, Boston, and Washington D.C. led the nation in self storage rent gains. These metros benefit from healthy rental housing sectors.

Weaker markets—like Denver, Portland, and San Diego—posted flat or declining rents. Demand lagged despite limited new self storage deliveries.

What’s Next

Without a shift in housing turnover or consumer patterns, rent growth will likely stay slow and uneven in 2026. Markets with rising population and housing activity may recover faster.

Oversupplied or slower-growth metros face more downside risk. Investors remain selective in underwriting deals, influenced by tighter lending standards and cautious capital markets. Measured optimism continues as national supply and demand patterns evolve.