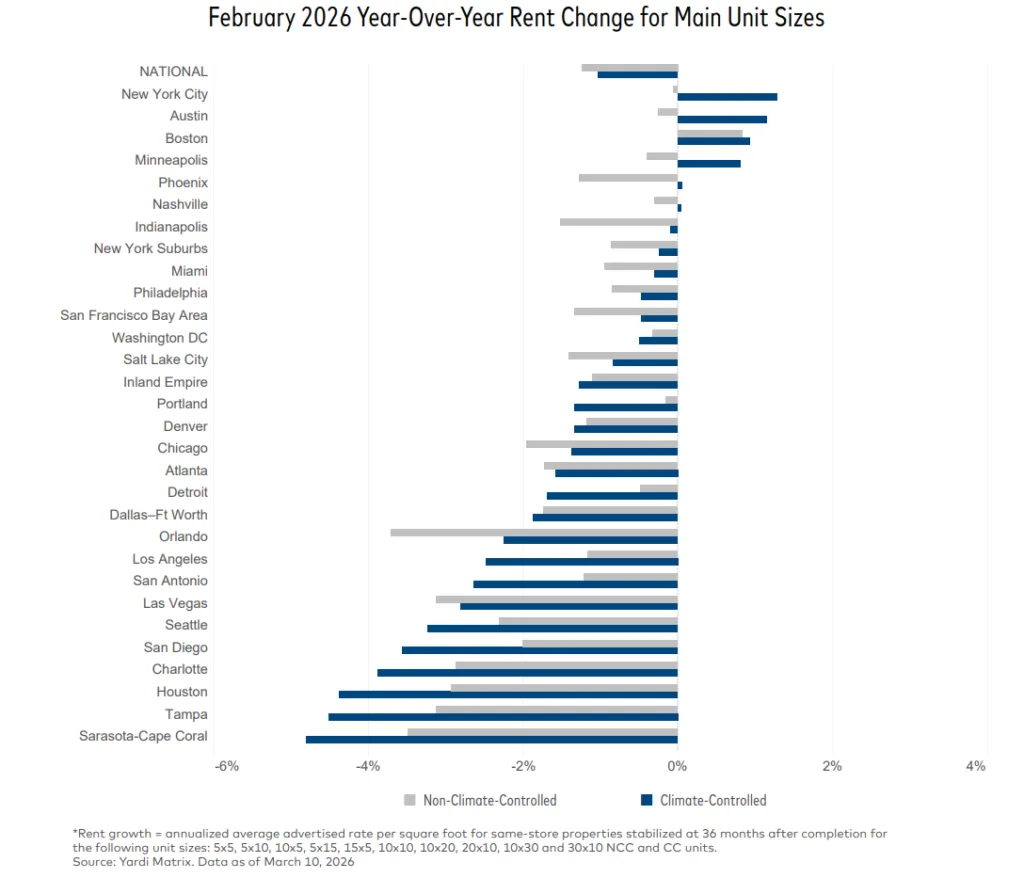

- Self storage national average rent fell 1.1% year-over-year in February 2026.

- Sun Belt metros with elevated new supply continue to face sharper rent declines.

- The national pipeline remains steady but masks metro-level volatility and new supply risks.

- Demand remains soft, leading to cautious revenue growth forecasts among REITs.

Soft Demand and Declining Rents

Self storage demand remained sluggish in early 2026 despite some stabilization at the national level. According to the latest Yardi Matrix National Report, average rents fell to $16.10 PSF in February, marking a 1.1% drop year-over-year. REIT guidance for 2026 remains cautious, with expectations for flat to slightly negative revenue growth due to ongoing pressure from limited new demand and excess available units.

Metro Performance Diverges

Rent trends continue to diverge at the metro level. Sun Belt markets like Sarasota–Cape Coral, Tampa, Orlando, and Charlotte posted some of the largest rent declines, with each seeing supply growth over 13% of existing inventory within the past three years, a pattern that mirrors broader apartment market dynamics where elevated supply has begun reshaping pricing power in high-growth Sun Belt regions. In contrast, supply-constrained metros such as Minneapolis, Chicago, and Boston maintained positive or flat rent growth as new development largely leveled off.

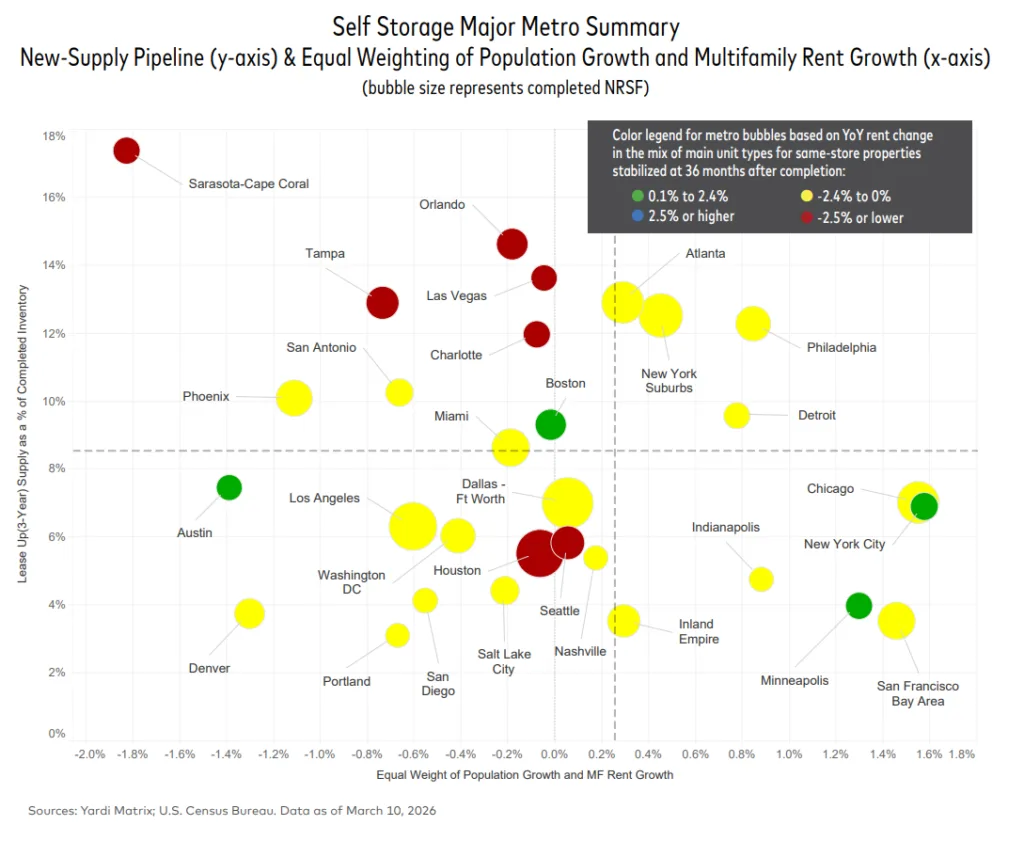

Supply Pipeline, Lease-Up and Risk

Nationally, 2.4% of existing self storage inventory is under construction, unchanged since January, with about 48.4M NRSF in various pipeline stages. While the overall pipeline is steady, metro-level volatility has increased—Las Vegas saw declines in its construction pipeline, while Austin and Houston experienced increases. New deliveries are biggest in metros already facing rent declines, intensifying competitive pressures and lengthening lease-up periods.

Why It Matters

The self storage sector faces ongoing headwinds from both slowing demand and a still-active development pipeline. With realized rates up only slightly due to lower move-outs and new supply continuing to outpace immediate demand in many metros, operators remain cautious. Rent growth appears unlikely to rebound until absorption improves or construction moderates more significantly, especially in oversupplied markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes