- Rental housing demand is buoyed by affordability pressures, a housing shortfall, and shifting demographics.

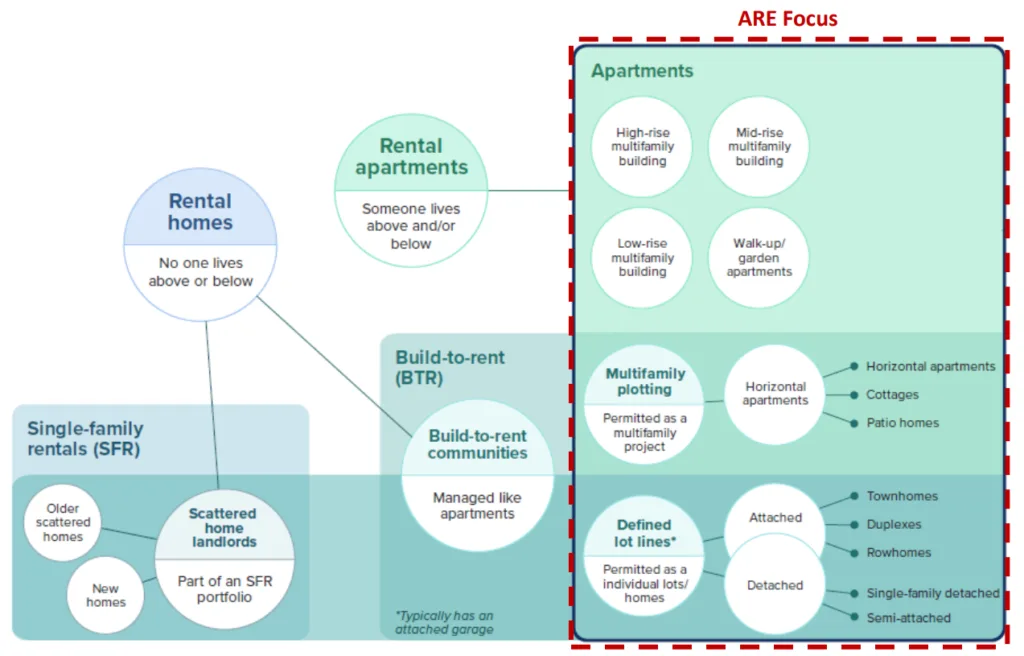

- Alpaca targets high-density townhomes, suburban low-rise, and urban high-rise assets, matched to specific capital strategies.

- Purpose-built rentals and preferred equity in urban assets offer unique opportunities amid supply cooling and capital distress.

- Market and product selection, not broad beta exposure, are critical for outperformance in 2026 and beyond.

Long-Term Tailwinds for Rental Housing

Alpaca’s recent white paper outlines a bullish outlook for US rental housing, despite current market headwinds. The firm highlights enduring demand drivers: homeownership’s rising unaffordability, a national housing unit shortfall, and refinancing risks confronting multifamily debt made during low-rate years. This confluence supports both operational upside and capital markets opportunities, particularly for those able to navigate market distress.

Alpaca divides the opportunity into three asset types—urban high-rise, suburban low-rise, and multifamily townhomes—and four execution approaches: structured forward purchase, distressed recapitalization, acquisition or repositioning, and low-basis development. The firm stresses nuanced product and capital structure selection over a “one-size-fits-all” approach to residential investment.

Affordability and Structural Demand Support

Rental housing demand remains underpinned by a 44% cost gap between renting and homeownership nationally. Mortgage rates above 6% have priced out nearly one-third of households, while only 37% can afford a median home. Even a return to 3% mortgages leaves renting more cost-effective in most markets.

Several tailwinds are building at once. Wage growth now exceeds inflation, which supports renter purchasing power. At the same time, many young adults still live with parents, creating pent-up demand for new household formation. The US has about 132M occupied housing units, with rentals making up roughly 34%. Demand continues to come from families, roommates, and downsizing retirees. However, traditional apartments often miss these groups, while townhomes better match their space needs, flexibility, and lifestyle.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply Pipeline Cools After Big Delivery Wave

The US rental housing market continues to face a substantial supply imbalance, with Alpaca estimating a 14M-unit need by 2030. Annual completions have dropped 18% from their 2022 peak, and multifamily starts are down 60% from peak as financing dries up. Deliveries are projected to dip to pre-2016 levels, while absorption may outpace supply by the next decade—setting the stage for renewed future rent growth.

Purpose-built rental deliveries have already declined sharply from 2023 peaks, making the case for townhome rentals in well-chosen markets. At the same time, tighter agency lending conditions and rising competition for multifamily debt are reshaping how projects get financed, further slowing new starts and reinforcing supply constraints. Alpaca’s approach avoids legislative risks associated with institutional single-family rentals by prioritizing high-density formats exempt from recent policy changes.

Target Markets and Execution Tactics

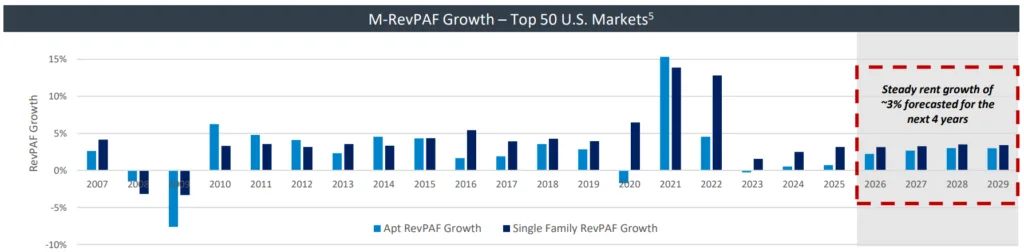

Alpaca identifies the strongest RevPAF (revenue per available footprint) growth in Atlanta, Seattle, and several Texas and California metros, though cautions that supply overhangs in certain markets will require careful micro-market selection and disciplined entry basis. Austin, for example, should see rent recovery as supply is absorbed, while markets like Phoenix face persistent oversupply.

The strategy focuses on forward-purchase deals for townhome communities in high-demand markets. It also deploys preferred equity into distressed but well-located urban towers. In addition, it acquires impaired assets at discounted bases and targets low-cost multifamily development in dense infill areas. This approach keeps entry pricing disciplined while preserving upside. Case studies highlight creative deal structures and strict control over acquisition basis. Underwriting targets 6.5%–7% yields on cost and IRRs above 20%.

What’s Next

Alpaca concludes that broad market beta in rental housing is no longer sufficient. Success will depend on identifying opportunity in distress and supply-demand mismatches, with a focus on products and capital structures aligned to evolving policy, demographic and financial market realities. Family-oriented high-density rentals, creative recapitalizations, and careful market selection remain core to the firm’s 2026 strategy.