- Global private real estate fundraising climbed 13% in 2025 to $172B, marking a modest recovery after multiple down years.

- Capital is increasingly concentrated among top managers, with mega-funds capturing 40% of total fundraising.

- Debt strategies, data centers, and alternative assets are driving investor interest as traditional sectors lag.

Private real estate is entering 2026 on firmer footing, with fundraising rebounding in 2025 despite persistent headwinds from elevated interest rates and geopolitical uncertainty, according to With Intelligence. While the uptick signals renewed investor confidence, expectations remain tempered as capital markets adjust to a higher-for-longer rate environment.

A Cautious Comeback

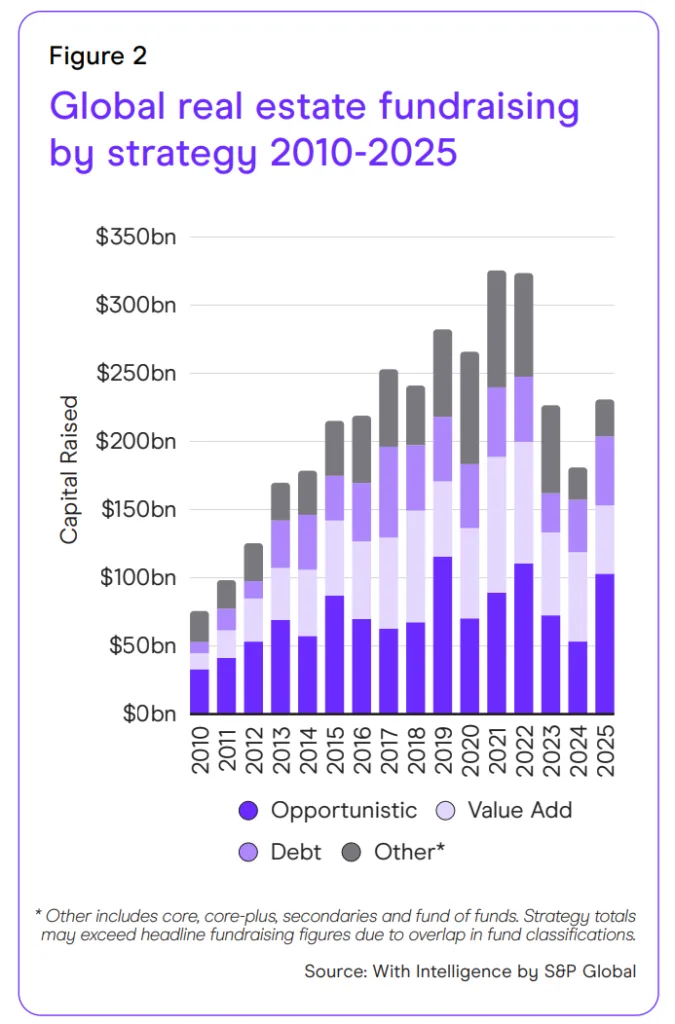

After two years of decline, global private real estate fundraising reached $172B in 2025, up from $152B the year prior. The increase marks the first annual gain since 2021, though activity still trails the record-setting pace seen during the low-rate era.

Higher borrowing costs still weigh on deal activity. The 10-year Treasury yield has stayed above 4% for much of the past two years. As a result, fund managers and investors are recalibrating expectations for 2026. Most large funds now target capital raises in line with 2025 levels. They no longer expect a sharp rebound.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Capital Concentration Accelerates

Even as fundraising improves, capital is flowing into fewer hands. The top 10 real estate funds accounted for $68B in 2025—roughly 40% of all capital raised—highlighting a growing divide between industry giants and smaller players.

Large general partners continue to scale through mergers, acquisitions, and diversified investment platforms, making them more attractive to institutional investors. Meanwhile, emerging managers face a tougher environment, with just two firms capturing more than half of the $4.2B raised by new entrants through Q3 2025.

Strategy Shift Reshapes Allocations

Investors are increasingly favoring opportunistic, value-add, and debt strategies, which made up nearly 90% of capital raised last year. These approaches offer higher return potential and greater flexibility in a volatile market.

At the same time, core real estate—particularly office—remains under pressure, though sentiment is beginning to stabilize. Improved performance and discounted entry points are drawing selective interest, especially as some investors view beaten-down office assets as mispriced opportunities.

Private Credit Gains Ground

As banks pull back from commercial real estate lending, private credit is stepping in to fill the gap. Debt funds raised $51B in 2025, the highest level since 2021, and have outperformed many equity strategies.

This shift is expected to continue as stricter lending standards and loan maturities create demand for alternative financing sources. Both established firms and new entrants are expanding into real estate lending to capitalize on the trend. Recent market coverage has also pointed to growing concerns among institutional investors about rising risks in private credit, even as allocations increase.

Data Centers And Alternatives Lead

Data centers remain a standout sector, fueled by AI-driven demand and digital infrastructure needs. Investor appetite continues to grow, with billions flowing into new funds targeting the space.

Beyond data centers, capital is rotating into alternative sectors like single-family rentals, healthcare, and logistics. In Europe, rising defense spending is նաև beginning to drive niche real estate opportunities tied to military and infrastructure needs.

Why It Matters

The recovery in fundraising signals improving sentiment, but structural shifts are redefining the market. Capital concentration, the rise of private credit, and increased demand for alternative assets are reshaping how and where investors deploy capital.

Importantly, many large pension funds remain under-allocated to real estate, providing a long-term tailwind for fundraising even as short-term conditions remain challenging.

What’s Next

Looking ahead, private real estate is poised for gradual—not explosive—growth. Fundraising is expected to stabilize rather than surge, with investors prioritizing discipline, diversification, and downside protection.

As capital continues to rotate and new opportunities emerge, particularly in lending and digital infrastructure, the industry’s next phase will be defined less by rapid expansion and more by strategic adaptation.