- Property fundamentals showed signs of stabilization across office, retail, industrial, and apartment sectors by late 2025.

- Office fundamentals approached balance, with the sector posting its second quarterly occupancy uptick.

- Industrial and apartment sectors narrowed demand-supply gaps but still lagged in demand versus supply.

- Rent growth for all major property types slowed, but remained positive entering 2026.

Stabilization Takes Hold

According to Nareit, US commercial property fundamentals experienced continued adjustment in the fourth quarter of 2025, with CoStar data charting a trend toward supply-demand equilibrium across the four main sectors. Each property type—office, retail, industrial, and apartment—posted improvements, hinting at stronger operational gains to come in 2026.

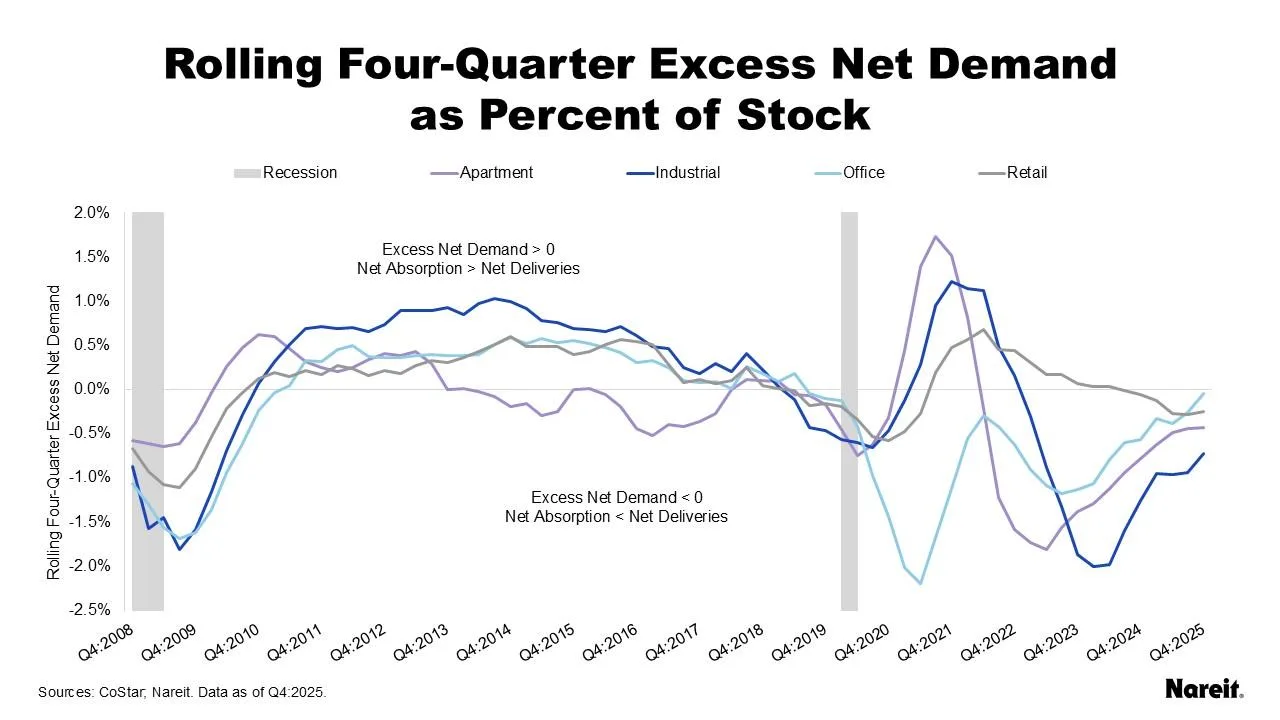

Demand and Supply Gaps Narrow

Net absorption fell short of new supply across all property types in late 2025, but each sector trended in a positive direction. Office posted a near-zero excess net demand, signaling fundamentals close to equilibrium. Retail excess net demand stayed modestly negative. Both industrial and apartment sectors maintained larger imbalances, but their supply-demand gaps have narrowed over recent quarters.

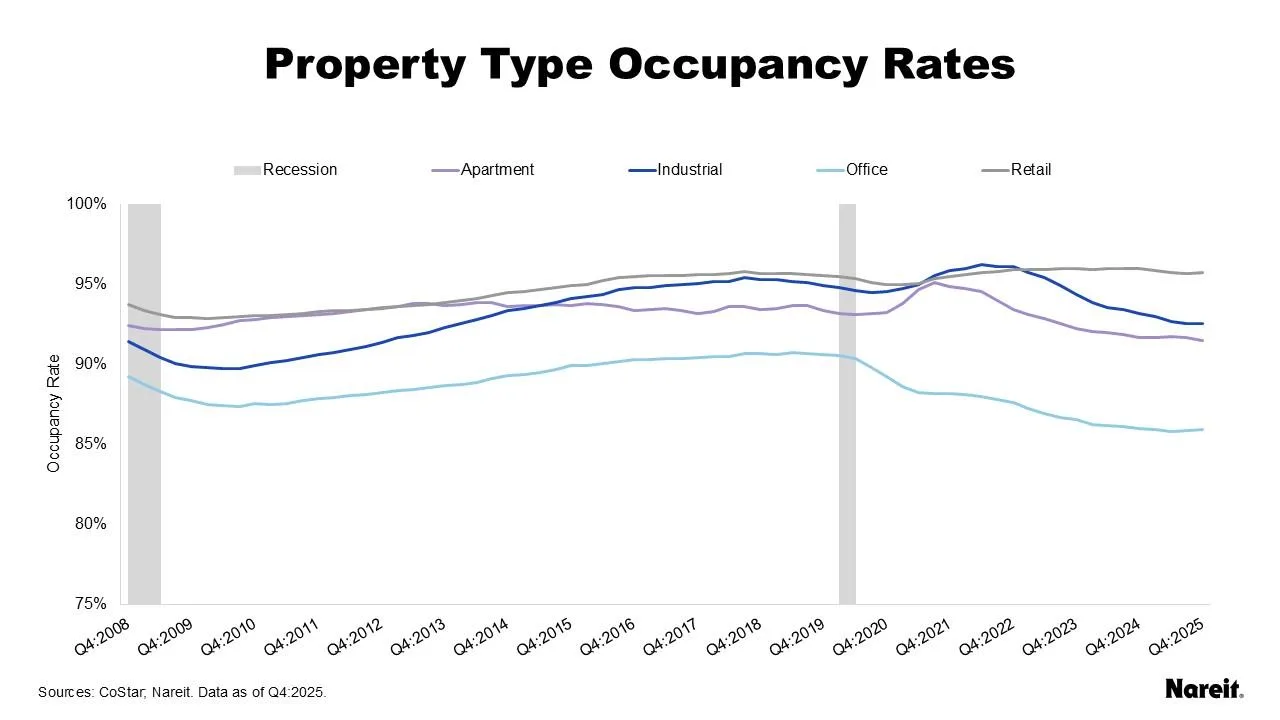

Occupancy Shows Signs of Recovery

Retail occupancy remained steady at 95.7%, while industrial and apartment rates stabilized at 92.6% and 91.5%, respectively, despite previous declines. Apartment occupancy hit its lowest mark since 2000. The office sector, after a lengthy downturn, reached 86.0% and saw the second consecutive quarterly increase, reinforcing early signals of stabilization in property fundamentals. Recent market reports have also noted improving office fundamentals as net absorption begins turning positive after several quarters of weakness.

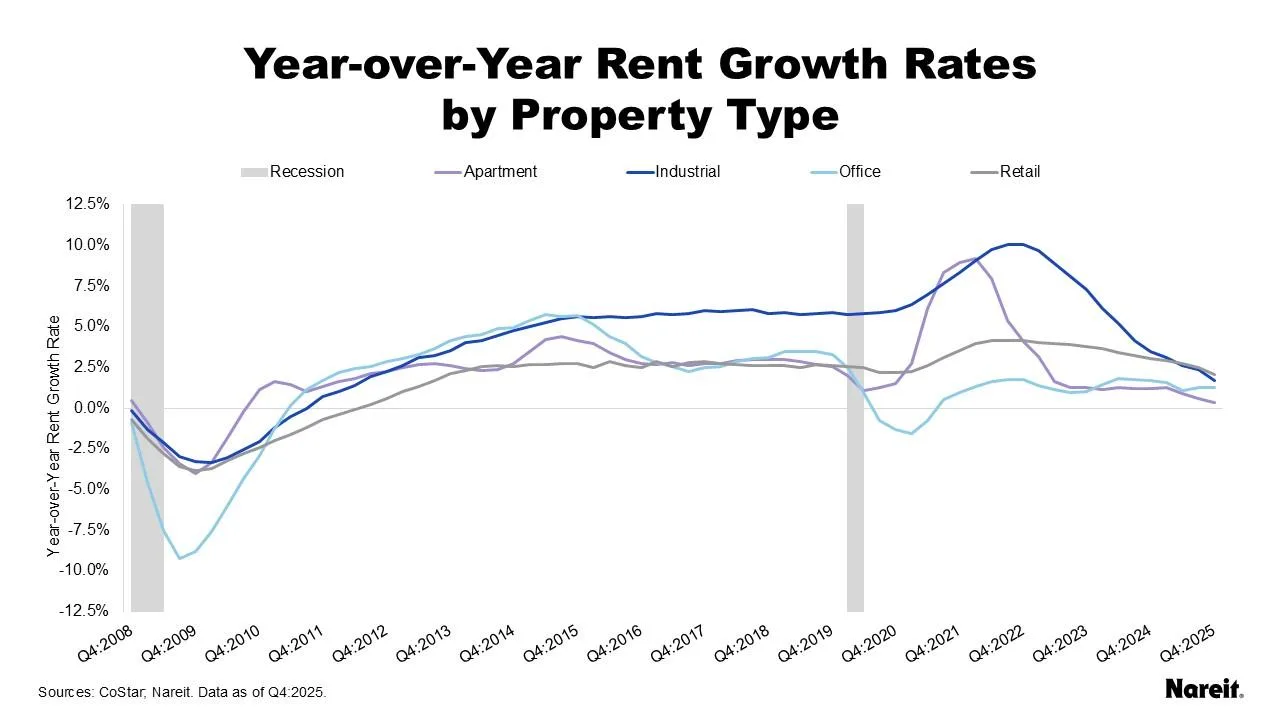

Rent Growth Remains Positive

All four sectors maintained positive year-over-year rent growth as of the fourth quarter of 2025. Industrial rent growth dropped to 1.7%, apartment to 0.4%, and retail to 2.1%, while office achieved 1.2% annual growth. Although below earlier peaks, these positive growth rates suggest improved stability, with further gains possible if property fundamentals continue to stabilize.

What’s Next

The return of more balanced property fundamentals points to potential operational improvement across all major sectors in 2026. Rising occupancy and rental rates are likely if stabilization in property fundamentals holds, setting the stage for better performance in the coming year.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes