- National office vacancy fell to 18.4% in December 2025, down 150 basis points from its March 2025 peak.

- Coworking expanded by over 1,000 locations in 2025, increasing its market share to 2.2%.

- Sustained listing rate resilience: national average at $32.86 PSF, down only 0.8% year-over-year.

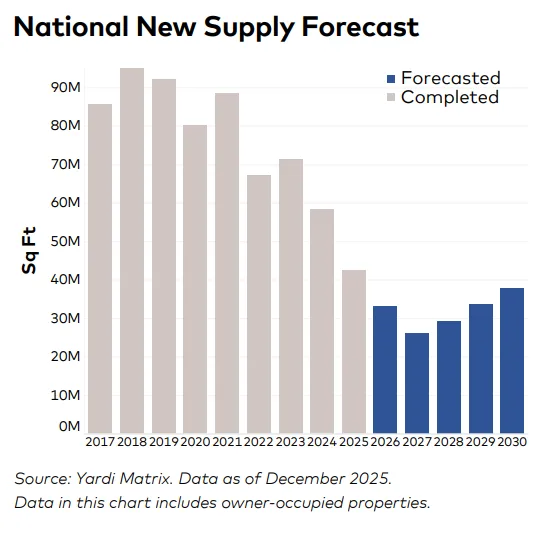

- Office supply pipeline contracted sharply to 30.9M KSF under construction, a 44% annual drop.

Vacancy Finally Eases

After a multiyear surge, office vacancy levels in the US have started to recede. The national vacancy rate peaked at 19.9% in March 2025 before dropping 150 basis points to 18.4% by December, according to Yardi Matrix. Manhattan, an early leader in this reversal, saw vacancy fall by more than 400 basis points since 2023 and now stands at 13.6%. This trend has begun to appear in other major metros as well, such as Houston, San Francisco, and the Bay Area, all posting vacancy declines of over 300 basis points in 2025. Despite these improvements, vacancy remains well above historical norms, and a full return to pre-pandemic levels looks unlikely given ongoing hybrid work trends.

Coworking Expansion Continues

Coworking carved out further space in the office sector last year, adding 1,000 new locations and lifting its total market share to 2.2%. This flexible model is capturing demand from companies not ready to sign traditional long-term leases, yet not ready to go fully remote. Owners of underperforming office assets are increasingly targeting coworking tenants to fill vacant space. Several of the country’s top coworking markets saw notable activity in 2025, reflecting broader shifts in how tenants are rethinking space needs. As coworking becomes more mainstream, new operators entering the sector can leverage established management partners to streamline their transition.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Conversions and Interest Rate Shifts

The Federal Reserve’s 25-basis-point rate cut in December and more expected reductions could make discounted office assets and costly conversion projects more feasible. Yardi’s Conversion Feasibility Index shows that 23.4% of office buildings nationwide are well-positioned or viable for adaptive reuse. Developers now have more opportunity to convert outdated offices to other uses, aided by attractive pricing and financing.

Sales and Pricing Trends

Total office sales in 2025 reached $53B, with Bay Area transactions surging both in volume and price. The Bay Area saw 119 deals, the highest since 2021, and a 35% jump in average price per PSF to $392, reversing a four-year decline. Notably, a Palo Alto life-sciences property sold for $29M, more than doubling its 2005 price. Nationally, the average office sale price was $192 PSF.

Supply Pipeline Contracts

New office construction continues to shrink. Only 30.9M KSF was under construction at year-end, down 44% from the prior January. New starts in 2025 (13.2M KSF) were almost flat with 2024, but overall deliveries remain at decade lows. As more tenants pursue smaller, amenity-driven “jewel box” locations over large footprints, new projects face ongoing funding challenges.

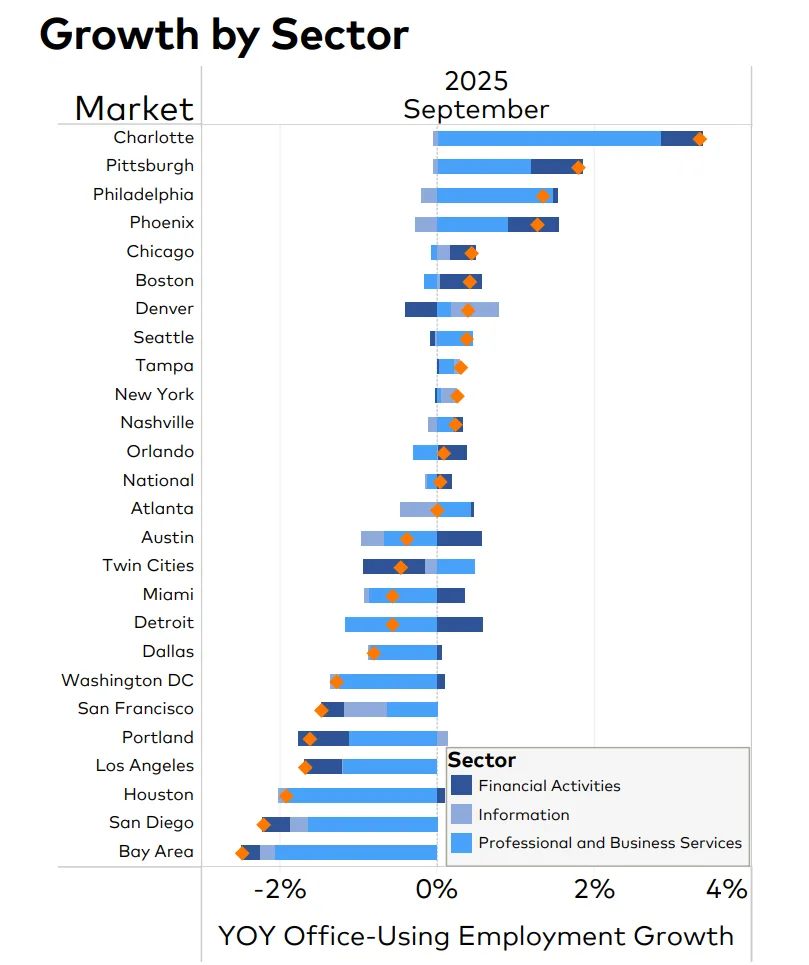

Employment and Market Leaders

Office-using employment was essentially flat year-over-year nationwide, but Charlotte posted standout growth at 3.3%. The city’s low taxes and business-friendly policies are driving in-migration, making it a notable hot spot for office demand and employment in 2026.

What’s Next

Momentum has shifted across the office sector, with vacancy easing and coworking gaining share. Uncertainty remains around just how far vacancy can decline, but ongoing conversions, muted new supply, and shifting tenant preferences are likely to drive further adaptation in 2026.