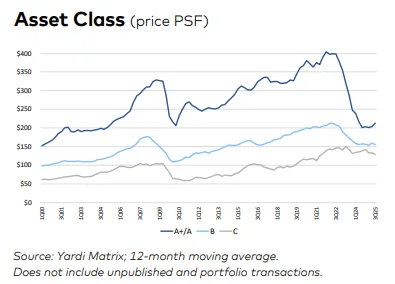

- US office property prices rose for the first time since 2022, signaling a potential market bottom, though they remain down 33% from their 2021 peak.

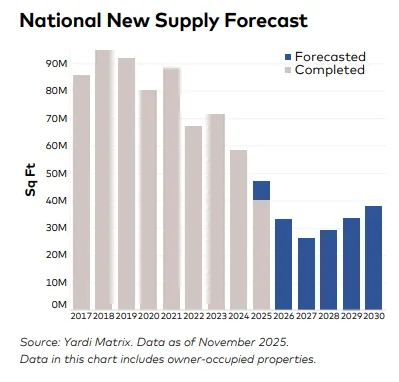

- Construction activity fell 44% year-over-year, and the national pipeline now represents just 1.7% of total stock, down from 3.0% last year.

- Coworking space surged 16% in 2025, capturing 2.2% of total office inventory, as hybrid work continues to drive demand for flexible space.

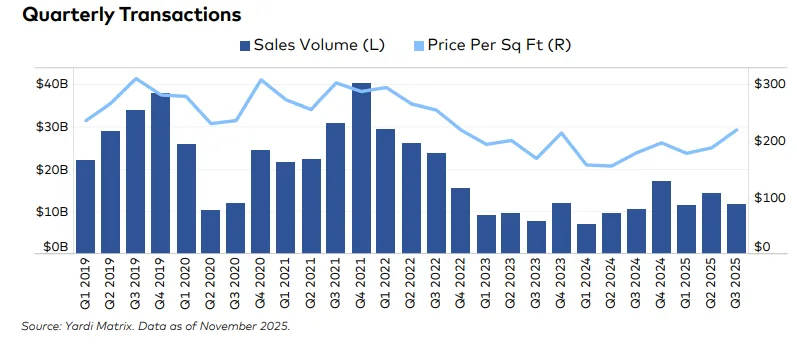

After years of falling valuations and limited demand, the national office sector may have found its footing, reports Yardi Matrix. According to their December 2025 report, average office sale prices rose 7.1% year-over-year to $190 PSF, the first increase since 2022. Though prices remain significantly below their 2021 highs, the uptick marks a potential bottom for the market.

Demand Remains Subdued

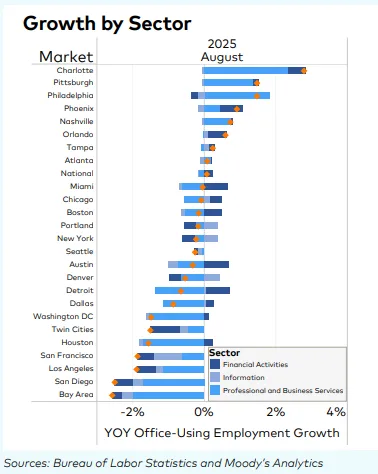

Vacancy declined slightly to 18.5%, but demand is still historically low. Physical occupancy has yet to rebound meaningfully, and job growth in office-using sectors was modest at 0.5% in 2025. The weak fundamentals, coupled with economic uncertainty, continue to suppress confidence in new development.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Construction Slows To A Crawl

Only 13M SF of new office space began construction by Nov 2025, unchanged from 2024 and far below historical levels. The total office construction pipeline dropped 44% from last year, representing just 0.5% of national stock under construction.

Boston still leads with 4.1M SF underway, but even that is less than half its pipeline from 2024. Notably, Manhattan and San Francisco bucked the trend, showing increases in development activity alongside growing demand.

Coworking Fills The Gap

The coworking sector expanded significantly in 2025, adding 22M SF—a 16% year-over-year increase. Coworking now accounts for 2.2% of all office space, bolstered by 42% of US firms adopting structured hybrid models. With most operators still running fewer than 10 locations, the sector is ripe for consolidation and innovation.

Markets Diverge Sharply

While some cities saw improvement, others continued to struggle. For instance:

- Manhattan: Strong performance with low vacancy and a growing pipeline.

- Chicago: Hit a record low in property values, averaging just $64 PSF—a 27.8% drop from 2024. A major property at 525 W. Van Buren traded at a 74% discount.

- Minneapolis: Vacancy spiked after Ameriprise Financial vacated its 1M SF headquarters downtown.

Why It Matters

Prices remain well below pre-pandemic highs. However, the recent uptick in sale prices, growing coworking demand, and slowing supply suggest the office sector is entering a period of gradual stabilization. Investors and developers alike are watching closely as certain metros begin to outperform others.

What’s Next

Conversion projects may gain momentum as discounted assets hit the market, especially in cities conducive to adaptive reuse. Coworking is expected to grow further, potentially reshaping office demand dynamics in 2026 and beyond.