- Office properties in major markets led value-weighted price gains, up 3.8% year over year.

- Midwest saw the largest regional surge, with value-weighted prices spiking 7.4% annually.

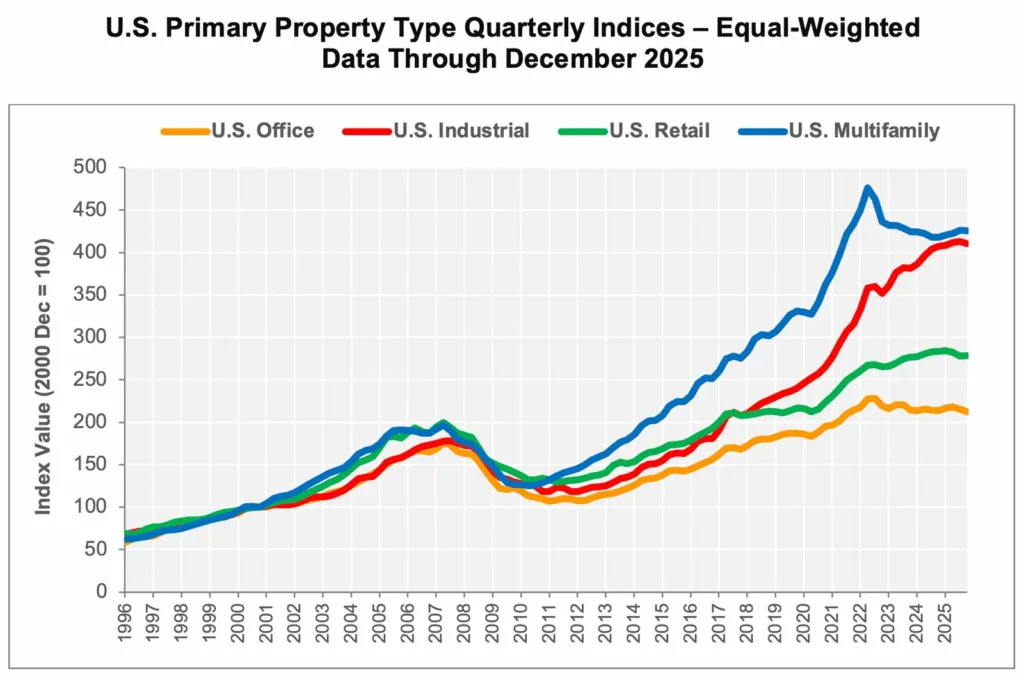

- Industrial and retail price growth slowed sharply compared to previous years.

- Transaction counts and sales volume both increased in 2025 despite mixed price trends.

Renewed Optimism for Office Properties

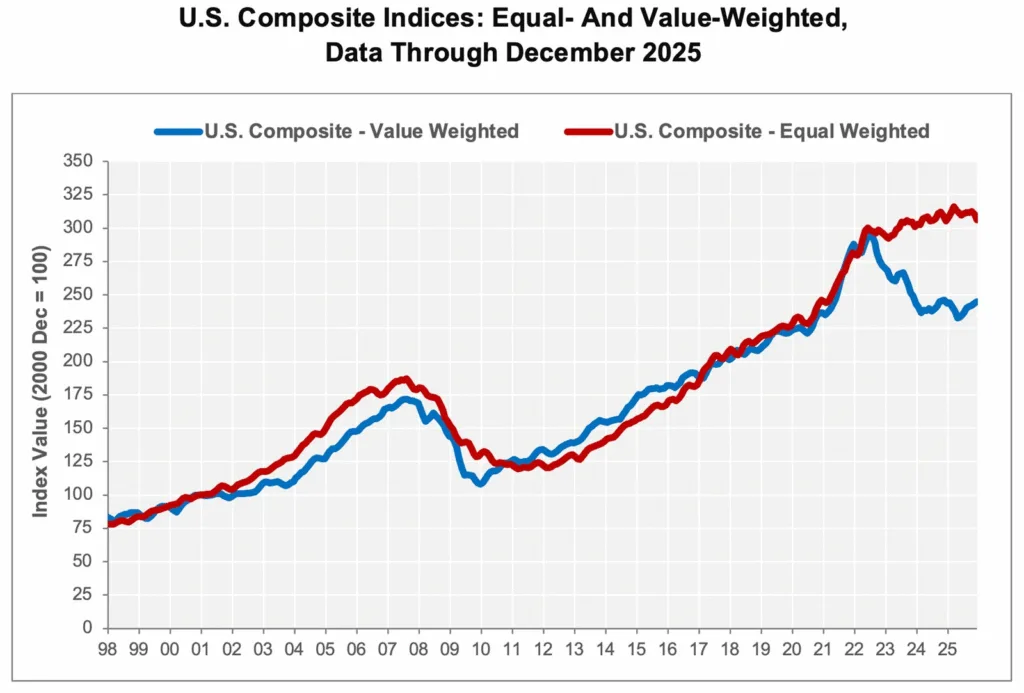

US commercial real estate prices saw varied performance in 2025, with office properties in major markets posting the strongest gains according to CoStar’s Commercial Repeat Sale Indices. Value-weighted office prices rose 3.8% over the year, marking a significant rebound from an 11.4% decline in 2024. The uptick reflects renewed investor confidence in high-value office assets, particularly in markets like San Francisco benefiting from demand in sectors such as artificial intelligence.

Industrial and Retail Markets Cool Off

Industrial and retail property prices increased just 0.4% each annually, a marked slowdown from gains of 4.1% and 2.6% respectively in 2024. Multifamily prices returned to positive territory, with a 0.7% rise after a 2.3% drop the previous year. The sector has benefited from increased investor confidence, particularly in more resilient markets where fundamentals have stabilized. The equal-weighted index, capturing trends for smaller and lower-priced assets, showed continued weakness for office and retail, but modest gains in industrial and multifamily segments.

Regional Shifts Highlight Midwest Strength

Regional analysis showed the Midwest outperforming all other regions with a 7.4% annual gain in value-weighted prices, led by multifamily (up 7.5%), industrial (up 4.5%), and office (up 3.2%). The South also posted annual increases, while the Northeast and West experienced annual declines in their value-weighted indices. These regional divides underscore the impact of local dynamics and investor focus on core assets in stable markets.

Transaction Activity Picks Up

Transaction activity grew in 2025: total repeat sale volume reached $143.7B for the year, up 20.7% from 2024. The investment-grade segment saw sales volume rise 20.5%, while general commercial sales volume grew 21%. Despite ongoing concerns about remote work and occupancy, institutional investors targeted quality office assets in leading markets, contributing to the year’s positive momentum.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes