- US office vacancy rose to 19.4% in July, up 130 basis points year-over-year.

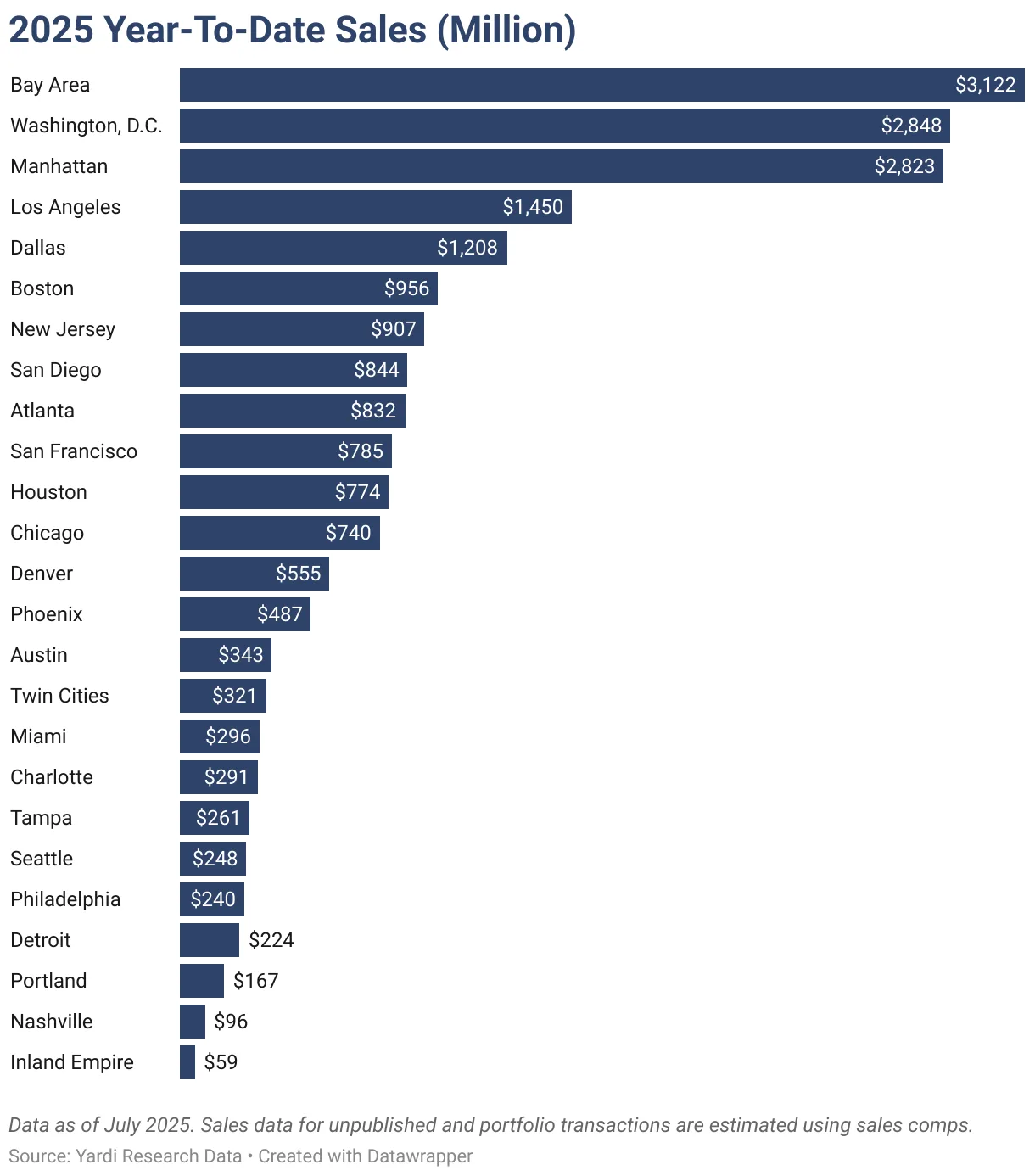

- $27B in office sales closed year-to-date through July at an average of $182 PSF.

- 42% of office properties sold since 2023 traded at a discount to prior sales.

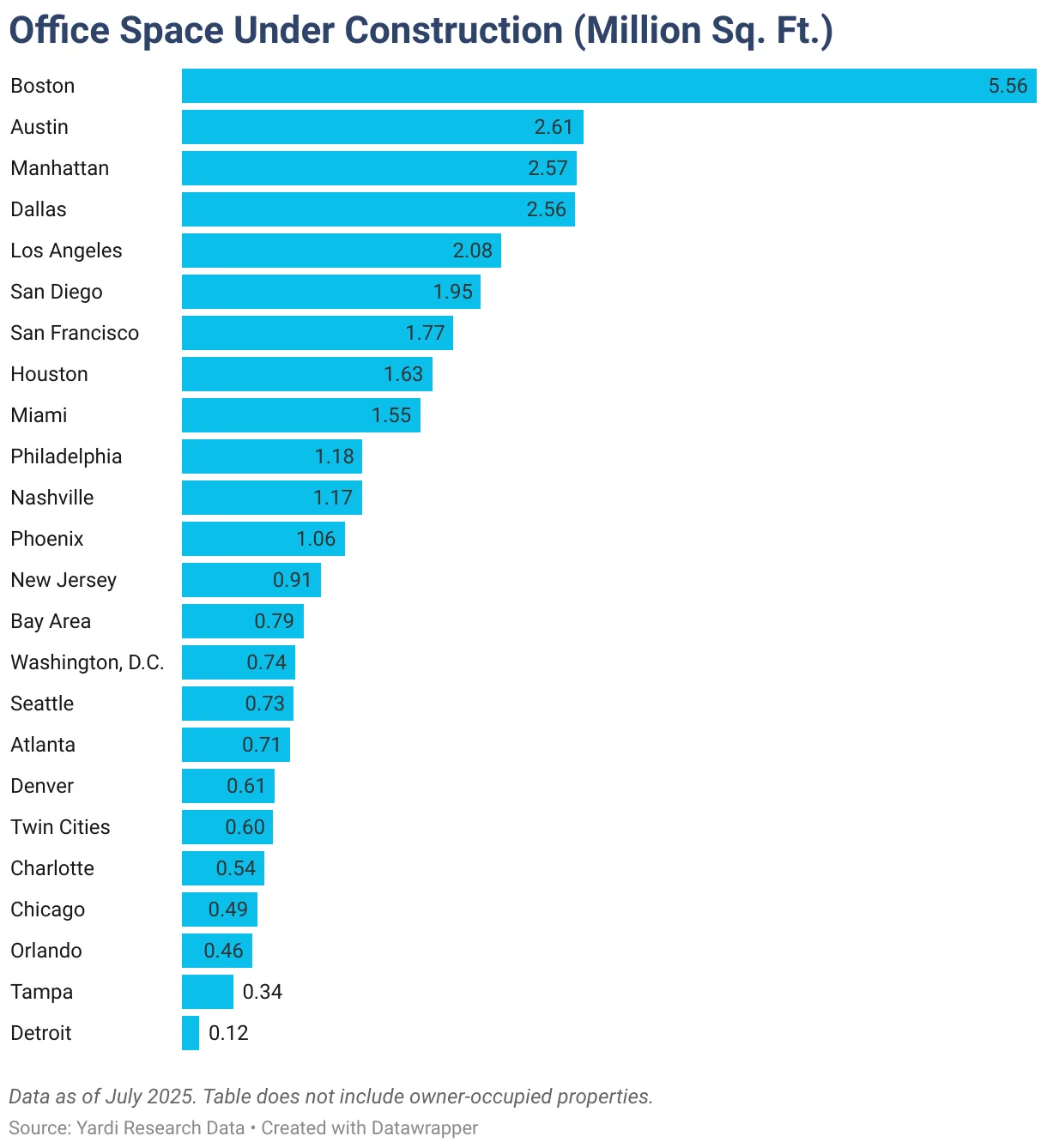

- Manhattan and Boston lead construction pipelines with millions of square feet underway.

Maturing Loans Accelerate Office Price Declines

Weak demand, stubbornly high interest rates, and maturing loans continue to weigh on office fundamentals, reports Commercial Cafe. As lenders show less willingness to extend financing for underperforming properties, pricing pressure is mounting — creating both risks and opportunities for investors.

According to Yardi Research, 42% of office assets traded since 2023 sold at a discount to prior pricing, with the sharpest corrections in Houston (69%), San Francisco (67%), and Manhattan (64%). Class A towers were hit hardest, with 71% of A/A+ assets selling below previous valuations, compared to just 19% of Class C properties. This recalibration of values, noted Yardi Research Director Peter Kolaczynski, is opening the door for buyers who see long-term potential. It is also creating new entry points for developers interested in redeveloping or repurposing struggling assets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Listing Rates & Vacancy

The national vacancy rate reached 19.4%, with Austin’s surging to 27% after adding 14.3M SF of new stock since 2020. Despite strong employment, the flood of supply and hybrid work patterns have kept availability elevated.

Phoenix Finally Sees Price Growth

Office investment sales reached $27B year-to-date through July, marking a sharp increase from 2024. The Bay Area, Washington, DC, and Manhattan were the only markets to surpass $2B in sales. Phoenix, however, stood out by posting its first pricing rebound in three years, with average prices rising from $165 PSF in 2024 to $197 PSF in 2025.

Manhattan Pipeline Swells

Nationally, 40M SF of office space is under construction — less than 1% of total stock. Yet Manhattan’s pipeline grew by 1M SF in July alone, driven by large-scale projects at Hudson Yards and Madison Avenue. Boston remains the leader, with 5.6M SF underway.

Regional Highlights

- West: San Francisco’s vacancy held near 26%, with asking rents topping $59 PSF, the highest in the US Bay Area sales led the West with $3.1B YTD.

- Midwest: Chicago remained the region’s volume leader with $750M in sales, averaging just $62 PSF — the nation’s lowest among major markets.

- South: Miami commanded the highest regional rents at $57 PSF, while Houston posted the most affordable sales at $96 PSF. DC led sales with $2.8B YTD.

- Northeast: Manhattan’s vacancy improved to 15.2%, with rents near $68 PSF and sales averaging $429 PSF, the nation’s highest.

Office-Using Employment

While national office-using jobs grew 0.1% Y-o-Y, sector-level performance diverged. Charlotte led metro-level gains with 3% job growth, fueled by corporate relocations, followed by Seattle (1.2%) and Orlando (1.1%).

Why It Matters

The office sector remains under pressure from structural demand shifts, refinancing challenges, and muted new construction. For investors, the current environment presents a dual-edged opportunity. Distressed Class A assets in core CBDs may be repriced enough to attract repositioning strategies. At the same time, secondary markets with stronger affordability and steady employment trends may prove more resilient.