- Regional banks are using an u0022extend-and-pretendu0022 strategy to avoid acknowledging distress in their CRE loans, according to a report by the Federal Reserve Bank of New York.

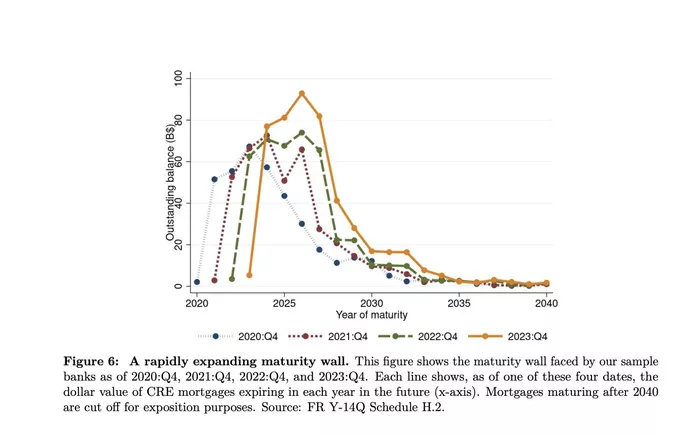

- The report highlights that $400B in near-term CRE loan maturities are piling up, with weaker banks more likely to hide distress, increasing the potential for defaults and capital losses.

- The extend-and-pretend approach, which has led to a decrease in new CRE mortgage origination, could result in a wave of defaults that could destabilize the financial system.

The Federal Reserve Bank of New York has raised alarms over a growing trend among regional banks: the tendency to defer acknowledging distress in their commercial real estate loan portfolios.

This practice, dubbed “extend-and-pretend,” has been allowing banks to delay the inevitable reckoning of nonperforming loans, but it could lead to broader financial instability, as reported by Bisnow.

The recent report suggests that the banking sector faces a looming $400B in near-term CRE loan maturities, increasing the likelihood of systemic risks.

Growing Systemic Risk

Regional banks have been under increased scrutiny following the collapses of Silicon Valley Bank, Signature Bank, and First Republic Bank in 2023. According to the report’s authors, Matteo Crosignani and Saketh Prazad, lenders are concealing distress by extending the terms of existing loans instead of marking them as troubled.

This has contributed to a growing “maturity wall” — a backlog of debt that could soon come due, threatening banks’ financial stability.

“The expansion of the maturity wall represents a financial stability risk as a sizable, and increasing, portion of bank regulatory capital is at risk should these CRE loans default,” Crosignani and Prazad wrote. The growing maturity wall now accounts for 27% of bank capital, a significant increase from 16% in 2020, underlining the escalating risks.

Impact on Lending, Stability

Since the first quarter of 2022, the extend-and-pretend strategy has caused a 4.8% to 5.3% drop in new CRE mortgage origination.

As banks hold onto more troubled loans, they reduce their capacity to issue new loans, further limiting growth in the CRE sector. The New York Fed report found that this practice has led weaker banks to underestimate the probability of default by 0.9% compared to their well-capitalized counterparts.

Moreover, these undercapitalized banks are more likely to grant maturity extensions, making it harder to recognize and address the actual extent of distress within their portfolios.

While offering short-term relief, this can create a dangerous buildup of risk if multiple defaults occur simultaneously, potentially leading to insolvency and a wave of property foreclosures.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Case Study: NYCB

New York Community Bancorp (NYCB) exemplifies the dangers of extend-and-pretend. Earlier this year, the bank struggled after recognizing massive losses in its CRE loan book, a stark contrast to its previous assurances of stability.

NYCB’s acknowledgment of $349M in net charge-offs in the second quarter, up from $81M, revealed a deeper issue. The fallout led to a $1B capital infusion and a leadership overhaul, including the appointment of former Treasury Secretary Steven Mnuchin.

The delayed disclosure of CRE loan weakness also triggered legal action against NYCB, highlighting the broader consequences of this strategy. Before NYCB’s challenges, five other regional banks faced downgrades from S&P Global due to similar concerns over cre exposure.

Interest Rate Dynamics

The extend-and-pretend strategy has become more prevalent as rising interest rates have made refinancing less feasible. Higher rates prevent borrowers from restructuring loans, pushing banks to extend terms instead of recognizing defaults.

However, this approach hampers the reallocation of capital that could otherwise support the transformation of struggling business districts, potentially affecting urban tax revenues and overall economic health.

“The resulting crowding-out of new credit provision slows down the efficient reallocation of CRE credit, likely hindering the downsizing of office districts in urban areas, also affecting cities’ tax revenues,” the report noted.