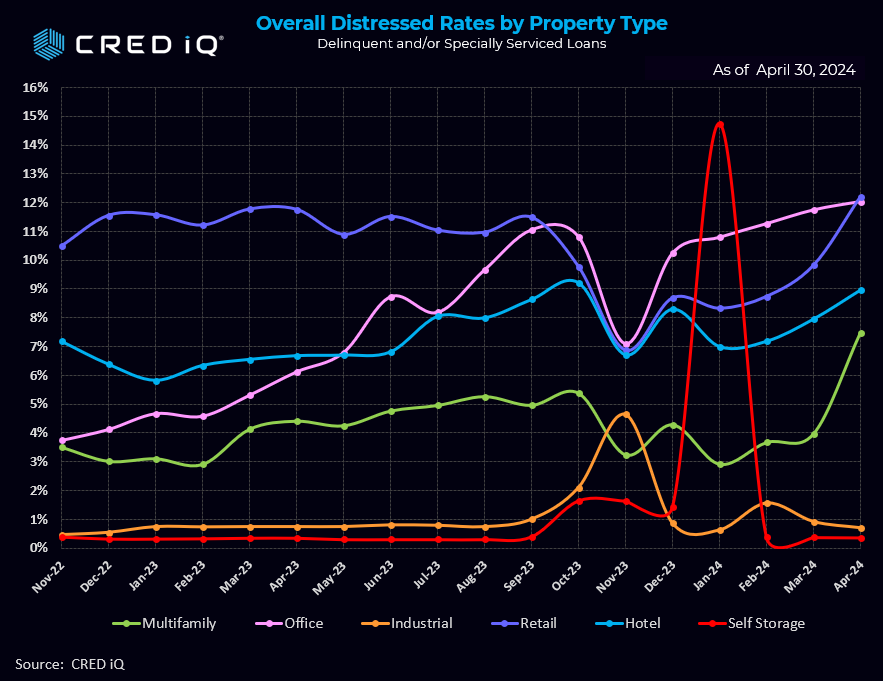

- The distress rate for U.S. multifamily doubled in just one month from 3.7% to 7.2% following a significant loan incident at Parkmerced.

- Retail distress surpassed hospitality at 11.9%, while the office distress rate rose slightly to 11.7%.

- About one-third of distressed loans are either current or in their grace period, with non-performing matured loans comprising 36.8% of the total.

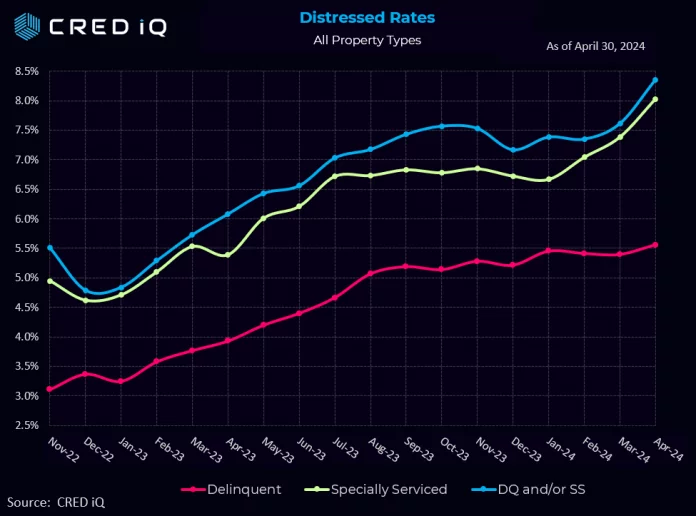

In April, CRED iQ reported a record-setting distress rate of 8.35% across all sectors, marking an increase from 7.61% in March. This rise in the distress rate, a metric assessing the health of commercial mortgage-backed securities (CMBS) loans, was primarily fueled by substantial distress in the multifamily property sector.

Multifamily Distress Surge

Notably, multifamily distress soared from 3.7% to 7.2%, driven by a $1.75B loan tied to Parkmerced, a 3,221-unit multifamily property in San Francisco. With a looming maturity date in December 2024 and underperforming metrics, this asset’s challenges contributed to the sector’s distress rate spike for the month.

Sector-Specific Breakdown

Retail properties recorded their third consecutive month of rising distress rates, reaching a record 11.9% in April. Among all CRE property types, retail faced the second-highest distress rate jump after multifamily, surpassing hospitality’s 8.7% rate increase. Office distress crept up to 11.7% and hotels followed suit at around 9%.

Meanwhile, industrial and self-storage stayed resilient, reporting low distress rates below 1%. Interestingly, self-storage saw a huge spike in distress up to nearly 15% back in January, but recovered just as quickly.

The Bigger Picture

A significant portion of distressed CRE loans currently fall into the non-performing or matured categories. About one-third of distressed loans are current or in their grace period. Non-performing matured loans comprising 36.8%, while performing matured loans account for 9.2%.

NOTE: CRED iQ’s distress rate combines delinquency and special servicing rates, covering non-performing loans and those failing to pay off at maturity. It also factors in all CMBS properties securitized in conduits and single-borrower large loan deals.