- March 2026 sees $3.18B of CMBS loans reach hard maturity, led by mixed-use, retail, and office exposure.

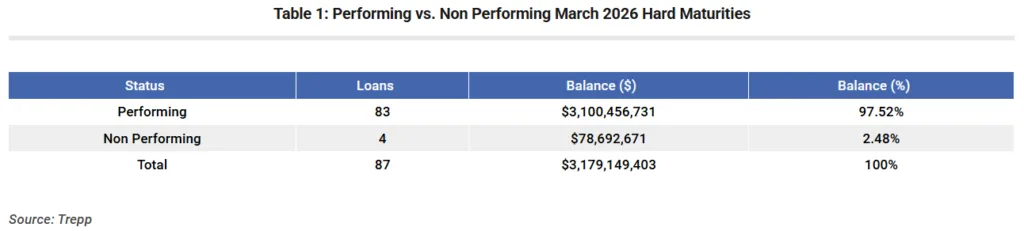

- Over 97% of the March cohort is performing, with only 2.5%—$78.7M—in non-performing status.

- Major loans include large mixed-use, life science, retail portfolios, and an office tower, each facing distinct refinancing challenges.

- Distress is concentrated in select assets; systemic risk remains limited in the current maturity pool.

Mixed-Use, Retail, and Office Dominate Maturities

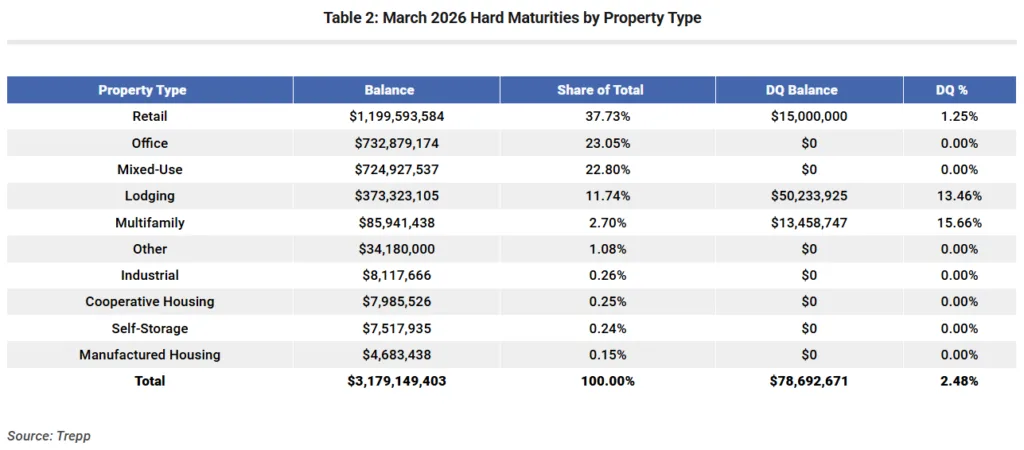

The March 2026 CMBS hard maturity roster spans 87 loans totaling $3.18B, according to data from Trepp. Mixed-use, retail, and office loans dominate the maturing balances: Retail comprises 37.7% ($1.20B), office 23.1% ($732.9M), and mixed-use 22.8% ($724.9M). Smaller exposures come from lodging, multifamily, and other property types.

Delinquency Remains Contained

Of the March cohort, $3.10B in loans are performing, while only $78.7M is non-performing. Delinquent assets are limited to select retail, lodging, and multifamily properties, including the Williamsburg Premium Outlets and the Sheraton North Houston, both recently reported in default. Non-performing loans make up just 2.5% of the total hard maturity exposure for the month.

Key Loan Exposures

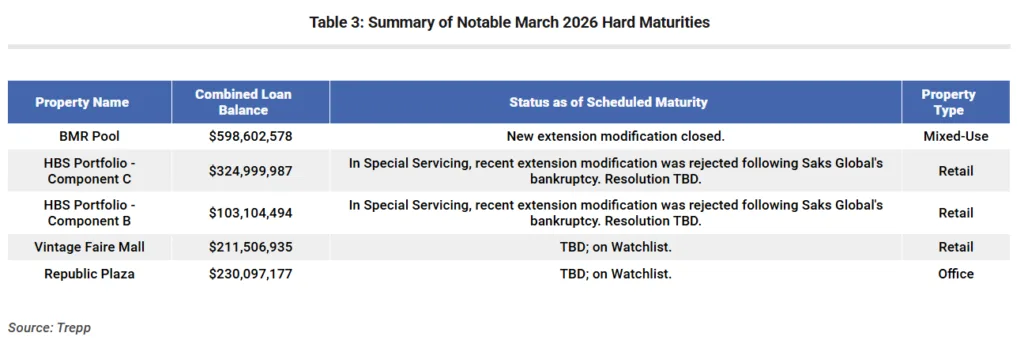

The largest upcoming maturities include the $598.6M BMR Pool mixed-use and life science portfolio. They also include the $325M and $103.1M HBS Portfolio retail loans. Other major loans include the $212.7M Vintage Faire Mall and the $230.1M Republic Plaza office tower.

Many of these loans sit in special servicing or remain on servicer watchlists. Some properties face tenant departures or ongoing lease restructurings. Others are negotiating extensions as maturity deadlines approach. Recent moves by banks to offload large CRE loan portfolios into private capital markets highlight how lenders are actively managing exposure ahead of maturities.

What to Watch

While mixed-use, retail, and office assets face maturity in March 2026, most loans remain current, and distress is isolated to a minority of portfolios. Outcomes for these CMBS hard maturities will depend on asset performance, tenant stability, and capital markets liquidity as sponsors pursue refinancing options. Systemic stress appears contained, but lenders and servicers remain alert to pockets of risk as major maturities approach.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes