- Industrial vacancies plateaued at 9.2% nationally, double 2022’s rates.

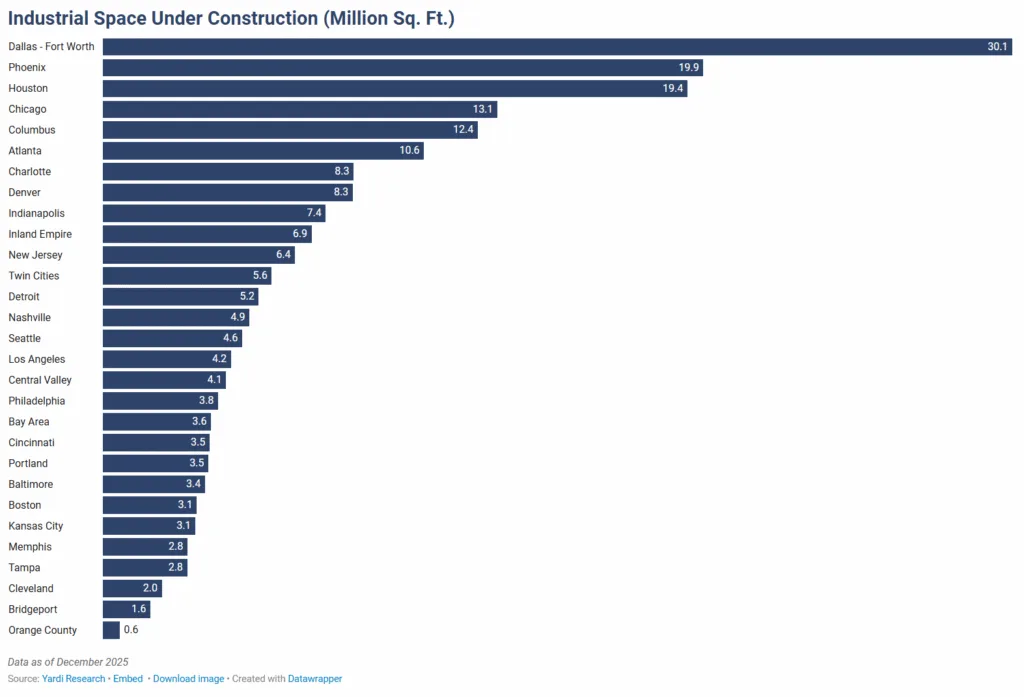

- Construction hit a decade low, with only 357.4MSF underway.

- In-place industrial rents rose 5.4% year-over-year to $8.87 PSF.

- Developers increasingly prioritize energy security in site selection.

Vacancies Plateau as Supply Pulls Back

Industrial real estate entered 2026 with vacancies stabilizing at 9.2%, more than double the 2022 rate. CommercialCafe reports that construction slowed significantly, hitting a decade low. Developers currently have just 357.4M SF underway. Deliveries in 2025 barely topped 300M SF. After years of rapid development and rising vacancy, the slowdown marks a sharp correction. Analysts expect vacancy rates to tighten later in 2026 as supply drops further.

Energy Security Moves Up the Agenda

Industrial developers have shifted their priorities when choosing sites. Access to affordable, reliable energy now outranks proximity to population or transit networks. This shift is most visible in projects for data centers and advanced manufacturing. Rising utility costs and power disruptions have driven the change. In fact, 89% of supply chain executives faced energy-related issues in the past year. Developers now target markets with strong energy infrastructure to manage future risks, especially as institutional capital flows into energy assets supporting AI-driven demand.

Rents and Occupancy Steadily Climb

Nationwide, in-place industrial rents averaged $8.87 PSF at year-end, advancing $0.11 from the prior month and up 5.4% YOY. Atlanta led rent growth among primary markets at 8.8%, buoyed by logistics infrastructure and population gains. Other strong performers included Miami (8.4% YOY) and Tampa (6.7% YOY). While national vacancy escalated by 120 bps in 2025, the industrial report expects stabilization and gradual tightening as the year progresses.

Construction Start Trends and Regional Standouts

New construction starts continued to slow, with only 265MSF breaking ground in 2025. However, Texas remains a bright spot; Dallas-Fort Worth and Houston together accounted for over 48MSF in new starts last year, benefiting from nearshoring trends and manufacturing reshoring. Pipeline expansions were also noted in markets like Austin and Phoenix, though both experienced downward momentum from earlier peaks.

Transaction Activity and Market Leaders

Despite headwinds, industrial transactions totaled $76.3B in 2025, representing a solid investment year. The average sale price per SF climbed 10% to $135 Y-o-Y. Notable regional highlights include New Jersey’s $2.8B sales volume and average pricing at $226 PSF. Dallas led all markets with $7B in sales, while Detroit and Phoenix were also significant contributors.

Regional Market Performance

California’s Orange County, Los Angeles, and Bay Area continued to command the highest in-place industrial rents nationally, though rent growth has moderated. The Midwest offered the most affordable rents, with Kansas City, St. Louis, and Indianapolis all below $5.30 PSF. Southern markets like Dallas-Fort Worth dominated construction and sales volume, while Charlotte posted the largest YOY sales increase regionally.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Why Energy Security Now Matters

An industrial report survey finds that 83% of logistics executives expect energy disruptions to cause the next major supply chain crisis. As data center and AI investments surge, communities are voicing concerns over utility demand. Power and water infrastructure, not just location or transport, are now central to the industrial real estate development calculus.

What’s Next

Looking ahead, the industrial report anticipates a slow recovery, with vacancies expected to tighten and construction picking up only where energy access and community acceptance align. As tariffs and trade policies remain uncertain heading into the USMCA review, industrial investors and developers will focus on resilience and adaptability across all regions.