- The top 25 US industrial markets accounted for two-thirds of new supply and national demand, reinforcing their influence on the country’s logistics economy.

- Vacancy rates are stabilizing as the construction pipeline hits its lowest point since 2019, suggesting tighter fundamentals in major markets.

- Net absorption is outpacing supply in nearly one-third of top markets, pointing to improving market balance heading into 2026.

Construction Hits A Low, Vacancy Levels Settle

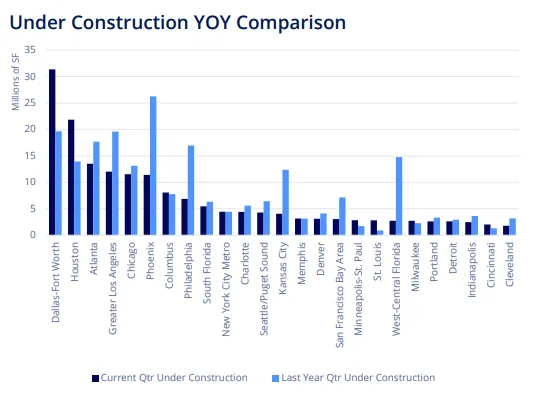

After years of rapid development, industrial construction across the US is slowing, reports Colliers. By Q3 2025, construction activity dropped 62% from its 2022 peak, with the pipeline at a 269.6M SF low. Within the top 25 markets, under-construction volume fell by 21.6% year-over-year to 171.4M SF.

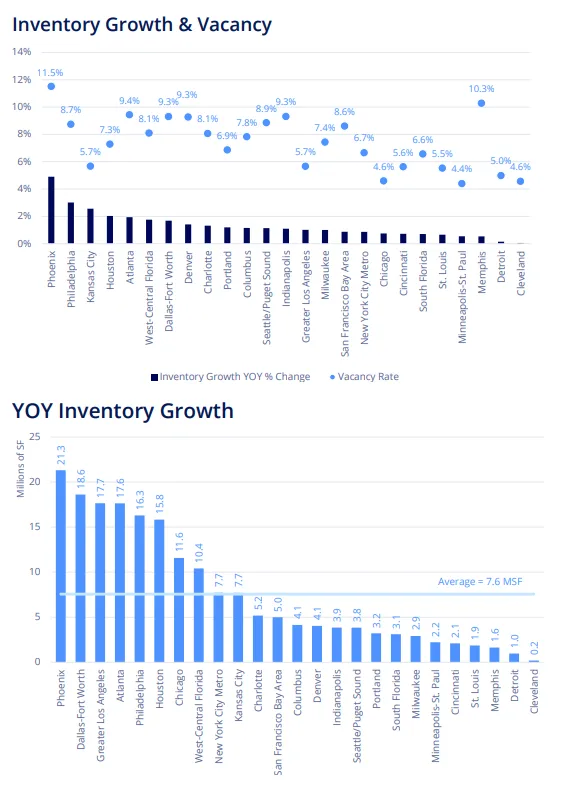

This contraction in new supply has helped ease pressure on vacancies. The average vacancy rate in the top 25 markets sits at 7.2%, just below the national average of 7.4%. Notably, Phoenix, despite leading in inventory growth with 21.3M SF added, is seeing vacancy ease from a high of 13.2% to 11.5%.

Supply Meets Demand

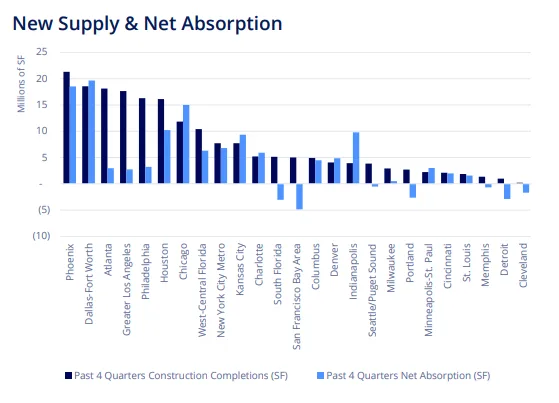

Demand is beginning to catch up. Over the past four quarters, net absorption reached 110.4M SF in the top 25 markets — a 4.6% increase year-over-year, even as national absorption dipped slightly.

Seven markets, including Indianapolis, Chicago, Denver, Kansas City, and Charlotte, saw demand outpace new supply. These signs of tightening fundamentals suggest that vacancy may peak in early 2026 before beginning to decline.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Rent Growth Flattens, But Coastal Markets Still Lead

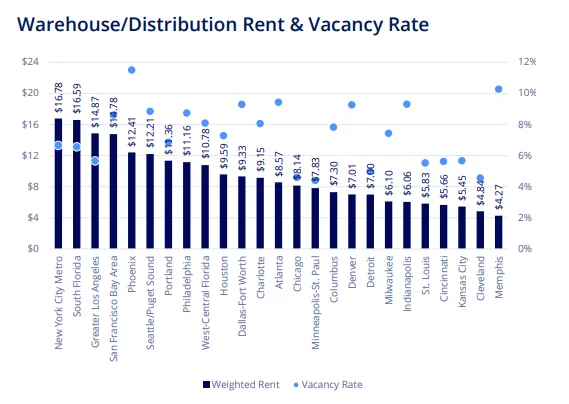

While demand strengthens, rent growth has cooled significantly. The national average warehouse/distribution asking rent grew only 1.9% over the past year, reaching $10.35/SF. In the top 25 markets, growth was flat at $9.32/SF.

Still, coastal ports maintain premium pricing, led by:

- New York Metro: $16.78/SF

- South Florida: $16.59/SF

- Greater Los Angeles: $14.87/SF

The sharpest decline was in Los Angeles, where rents dropped 11.4% year-over-year.

Controlled Growth And Speculative Restraint

Developers remain cautious, with most new projects now build-to-suit rather than speculative. The pipeline is expected to bottom out near 260M SF before gradually rebounding in late 2026 as vacancy tightens and replacement-cost rents align with market expectations.

Markets such as Dallas–Fort Worth, Houston, and Columbus continue to lead in construction volume, with DFW seeing the largest increase in pipeline activity, up 11.7M SF from a year ago.

Why It Matters

Industrial real estate is moving from pandemic highs to normalization, with top markets set for a steady, controlled rebound. With rent growth tapering, vacancy stabilizing, and supply reined in, developers and occupiers alike are operating in a more sustainable, albeit competitive, landscape.