- Actively managed global real estate funds held $16.7B in assets as of Q2 2025, with 25 funds tracked (22 reporting).

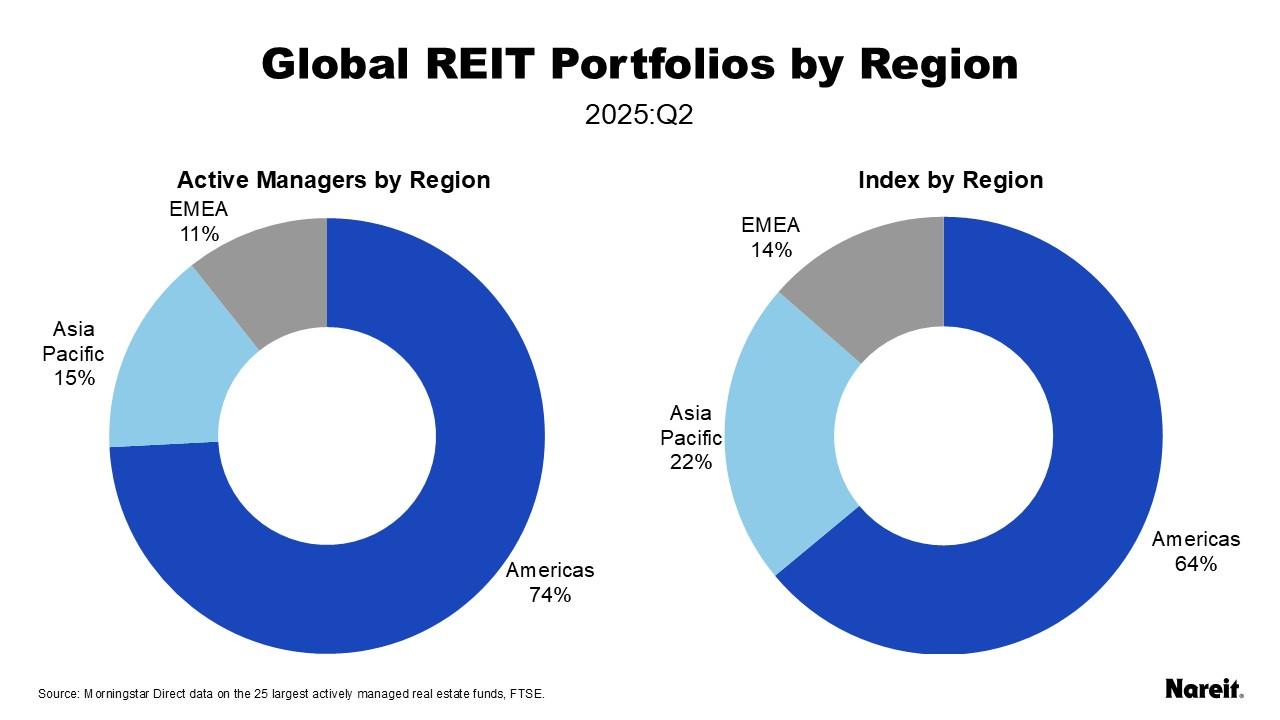

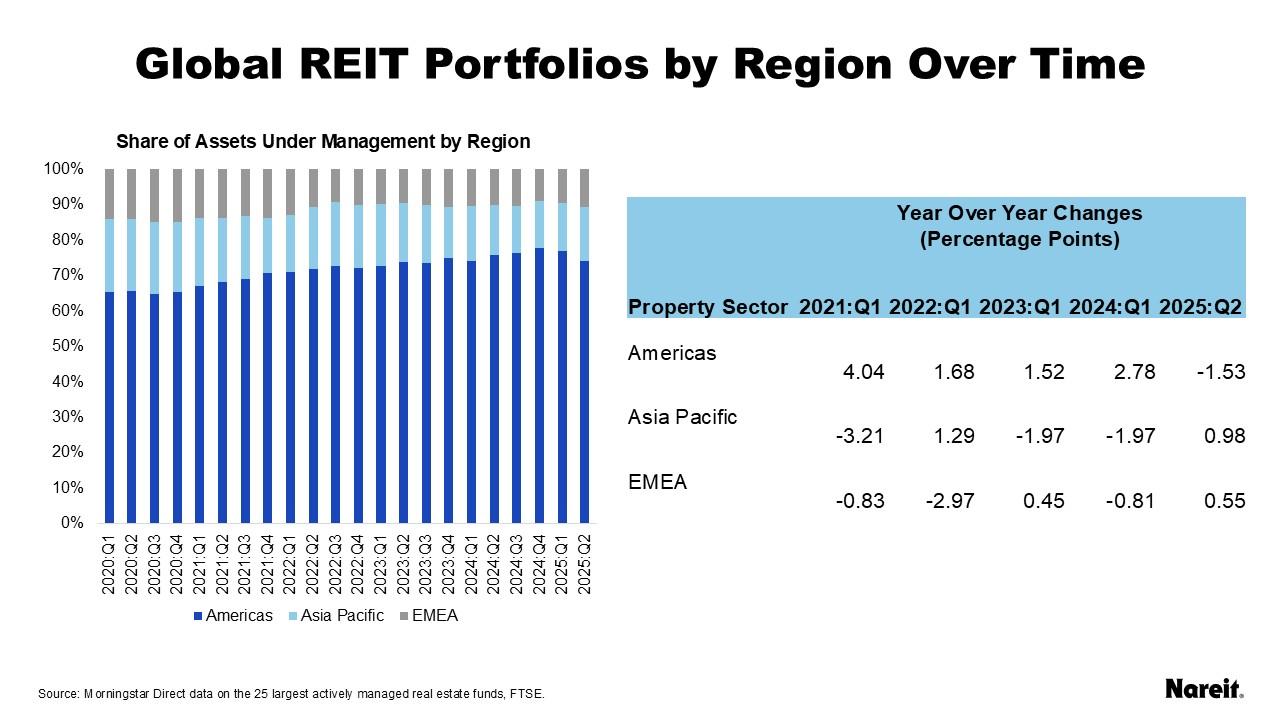

- Fund managers have increasingly overweighted the Americas (74%) and reduced exposure to Asia Pacific (15%) since 2020.

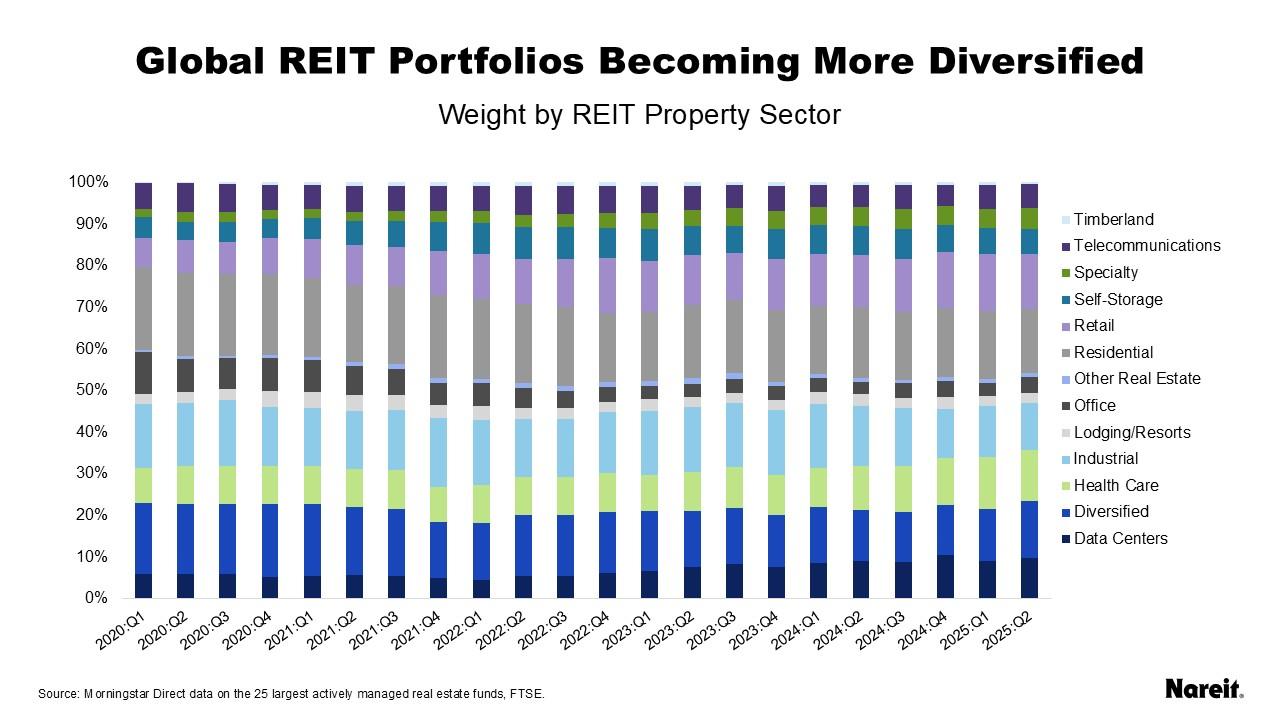

- Sector allocations show a strong pivot to retail, data centers, health care, and lodging/resorts, with major pullbacks in office and residential.

A Global Lens on Real Estate Allocation

A new quarterly tracker developed by Nareit is shedding light on the investment strategies of 25 of the largest actively managed global real estate funds—distinct from their US-only counterparts, according to Nareit.

As of mid-2025, these funds collectively manage $16.7B in real estate assets and are adjusting their positions across geographies and sectors in response to changing market dynamics.

Americas on the Rise

Fund managers have steadily increased their investments in the Americas, particularly the US, rising from 65% in 2020 to 74% by mid-2025. This shift has largely come at the expense of the Asia Pacific region, which dropped from 21% to 15% in the same period. EMEA holdings remained relatively stable at 11%, slightly below the index’s 14%.

Sector Shake-Up: Retail and Data Centers Ascend

A closer look at property sectors reveals a significant realignment since 2020:

- Retail allocations nearly doubled, from 7% to over 13%.

- Data centers grew by nearly 4 percentage points to 10%.

- Health care rose to 12%, while lodging/resorts and self-storage also gained ground.

- Residential and diversified, once dominant, declined to 15% and 14%, respectively.

- Office fell from 10% to just 4%, now among the lowest allocations.

- Industrial remained stable until a notable drop to 11% in 2025.

Active vs Index

Compared to the FTSE/EPRA Nareit Global Extended Index, active managers are tactically overweighting certain sectors:

- Data centers lead at 135% of their index weight.

- Lodging/resorts, self-storage, and health care are all over 130% of their respective index shares.

- Diversified and telecommunications remain persistently underweight, with diversified representing only 65% of its index share.

- Office has shifted from overweight to underweight, while retail has moved to parity.

Why It Matters

Active global managers are signaling clear preferences amid macroeconomic shifts—moving capital into more resilient or growing sectors like data centers and health care, while stepping back from sectors like office and residential. This pattern mirrors trends in US real estate but includes unique global tilts, such as greater allocations to lodging and self-storage.

What’s Next

With regional and sector diversification playing an increasing role, active managers appear positioned to respond to global economic trends and shifting investor priorities. Expect continued divergence from traditional benchmarks as these funds seek alpha in non-traditional and emerging real estate segments.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes