- Distressed sales have remained low in this cycle, peaking at just 3% of market share through mid-2025, compared to 20% after the 2008 GFC.

- The rise of debt funds—especially those targeting mezzanine debt—has reshaped how financial distress unfolds in commercial real estate.

- Mezzanine-focused funds are showing signs of stress, offering a potential entry point for investors seeking discounted opportunities.

A New Cycle, A New Kind of Distress

Commercial real estate (CRE) has faced repricing and volatility since the 2022 interest rate shock. Yet, distressed asset sales have remained surprisingly muted. MSCI reports that, unlike the post-GFC period—when distressed transactions surged to 20% of sales—this cycle peaked at just 3% by mid-2025. Property prices have fallen, though not as dramatically. The maximum decline this time has been 10%, compared to a 23% drop during the GFC.

So why haven’t distress-driven opportunities followed?

The Rise of Debt Funds in the Capital Stack

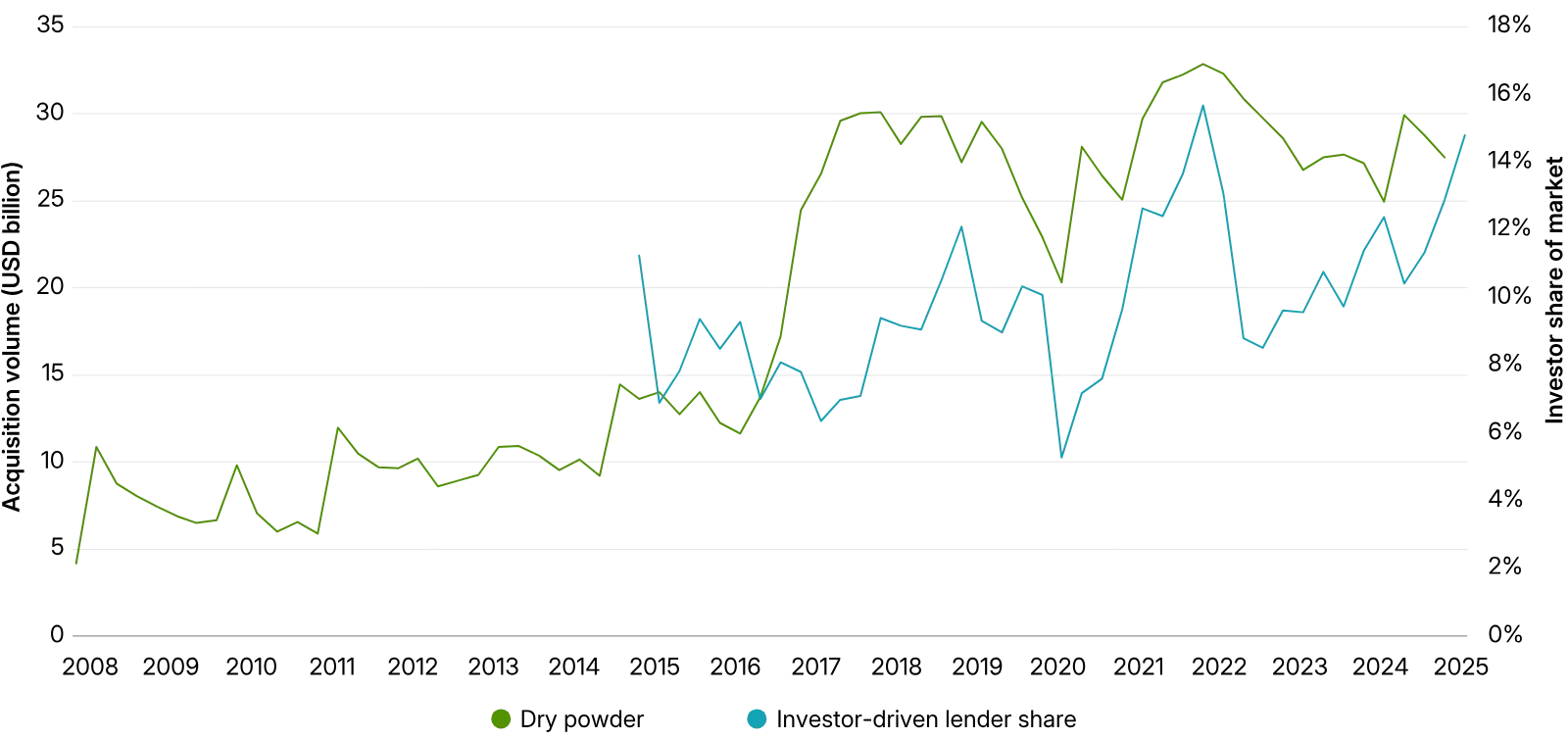

One key factor: the growing influence of investor-driven debt funds. Once a niche market of hard money lenders and mortgage REITs, this segment is now dominated by institutional capital deployed through private credit vehicles.

Debt funds, often less regulated than traditional banks, have taken over roles once held by more conservative lenders. This shift accelerated after the 2018 HVCRE regulations increased oversight on bank lending. With more capital available and fewer constraints, these funds have filled key gaps in CRE financing—especially in the mezzanine layer.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Understanding Risk: It’s All About Position

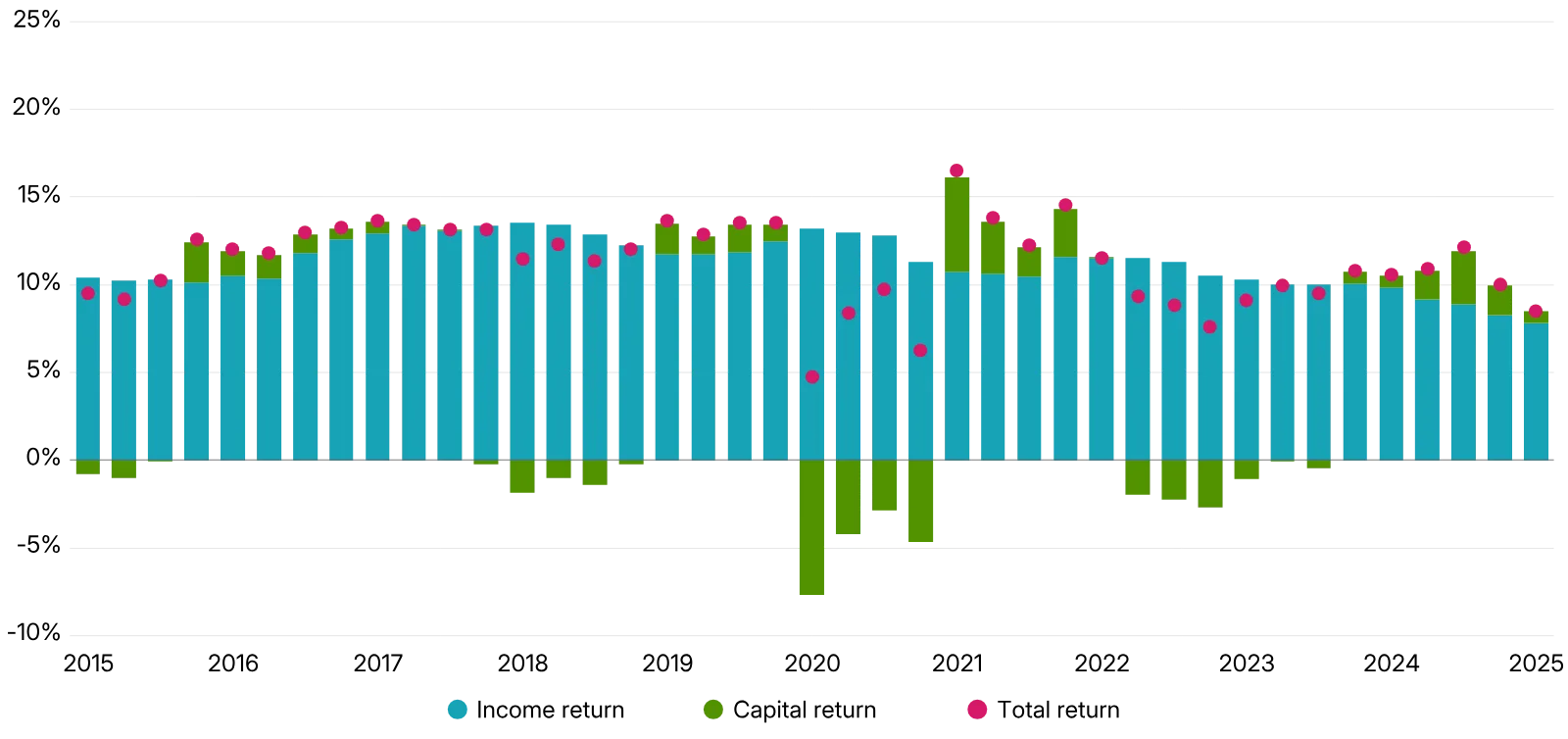

In real estate equity, risk is usually described as core, value-add, or opportunistic. In CRE debt, risk hinges on capital stack positioning. Senior debt typically offers steady, low-risk income, while mezzanine debt carries more risk and the potential for greater losses—or returns.

From 2020 to 2025, MSCI data shows mezzanine-focused debt funds saw a sharp rise in income-driven returns—up to 210% of total return. Capital losses, however, pulled overall performance down. These trends indicate mezzanine debt has absorbed much of the recent distress, even if it hasn’t surfaced in asset sales.

The Quiet Workaround: Mezzanine Restructuring Instead of Foreclosure

Unlike the GFC, this cycle has seen fewer courtroom battles and more behind-the-scenes financial maneuvering. Borrowers facing short-term value erosion are opting to add layers of mezzanine debt to delay foreclosure, hoping future market recovery will restore equity. Mezzanine lenders often gain control rights upon default, allowing for faster resolution and more flexible workout strategies.

This shift is happening against a backdrop of broader government and institutional strain, including federal housing agencies impacted by staffing cuts. As liquidity tightens across the system, the availability of capital—and the conditions under which it’s deployed—continues to evolve.

Where the Opportunity Lies

For investors hunting distressed opportunities, the answer may not lie in outright asset sales. Instead, it could be found within the structures of debt funds—especially those holding mezzanine positions. As capital values decline and losses mount, these funds may offer discounted entry points into troubled assets. Unlike traditional sales, they avoid the delays often tied to foreclosure battles.

Bottom Line

Distress in this cycle hasn’t disappeared—it’s just taken a different shape. With debt funds playing a central role in the capital stack, especially in mezzanine layers, distressed opportunities may be more about recapitalizations than auctions. For savvy investors, that’s a subtle but critical shift worth watching.