- CRE prices stabilized across most sectors in Q4 2025, according to TPPI data.

- Larger institutional assets continue to undergo a slower repricing process.

- Sector performance varies, with lodging weaker and retail showing resilience.

- Mid-sized and smaller property transactions drive current price stability.

Market Conditions Reveal Steadying CRE Prices

Commercial real estate (CRE) pricing saw broad stabilization in Q4 2025, with most sectors reflecting an environment shaped by persistent borrowing costs, not sudden shocks. According to the Trepp Property Price Index (TPPI), pricing adjustments are now more gradual, particularly as market participants adapt to costlier financing and a moderate economic backdrop. While price discovery continues in the largest institutional assets, the mid-sized and smaller segments have entered a relatively stable phase.

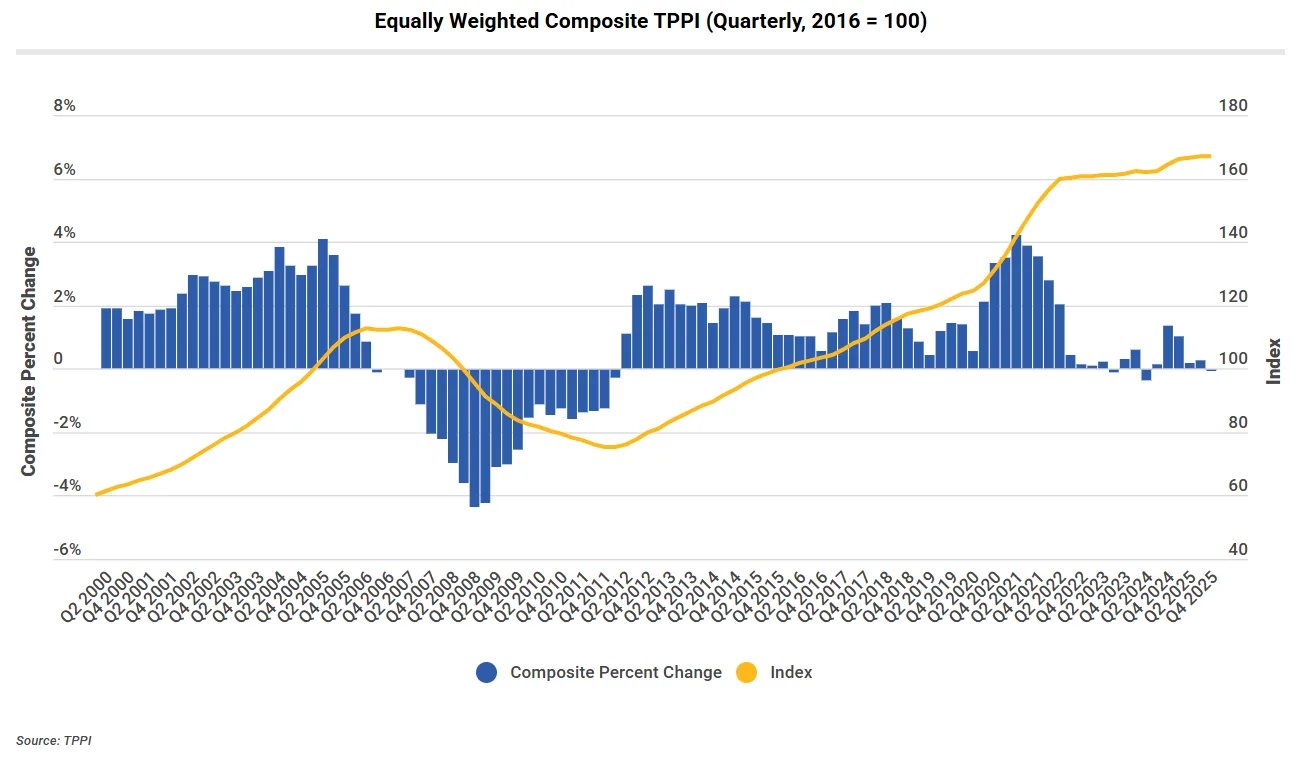

TPPI Methodology Supports Robust Trend Analysis

The TPPI tracks CRE pricing using two measures: equally weighted (EW) and value weighted (VW) indices. These metrics provide a detailed view of pricing trends across the commercial real estate market. In Q4 2025, more than 9,650 sale pairs strengthened the dataset and improved market visibility. The EW index remained nearly flat for the quarter, declining just 0.03%. However, it still sat 1.47% above its level from a year earlier.

The VW index fell 0.44% during the quarter and remained flat on a year-over-year basis. This gap between the indices reflects differences across deal sizes. Large institutional transactions still face ongoing repricing as capital costs remain elevated. Meanwhile, most mid-sized and smaller assets already adjusted to higher interest rates. As a result, pricing across much of the broader market has begun to stabilize.

Sector-Level Trends Show Varied Recovery

- Multifamily: Prices held steady for smaller assets but rose 1.31% in the VW index, though larger deals still trade below earlier peaks as high borrowing costs linger. At the same time, developers in many markets are also grappling with shifting construction costs and labor dynamics, which continue to influence project timelines and feasibility.

- Office: The segment saw slight declines in Q4, but smaller offices have stabilized even as institutional-scale buildings face ongoing price discovery and financing challenges.

- Retail: Demonstrated resilience, with both EW and VW metrics showing modest quarterly and annual gains. Consumer demand underpins stable valuations.

- Industrial: Small declines reflect a transition from rapid appreciation to stabilization. Future pricing depends on trade policy shifts and supply chain changes.

- Lodging: Remains the weakest performer, with price drops continuing due to uncertain business travel and fluctuating leisure demand.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

What’s Next for CRE Pricing

The Q4 2025 TPPI signals most CRE price corrections are largely complete for mid-tier and smaller properties, although large institutional assets are still repricing amid higher capital costs. This uneven adjustment is likely to persist, with pricing stability expanding if market participants acclimate to ongoing financing conditions. Continued TPPI updates will monitor these trends across sectors and geography as the market adapts.