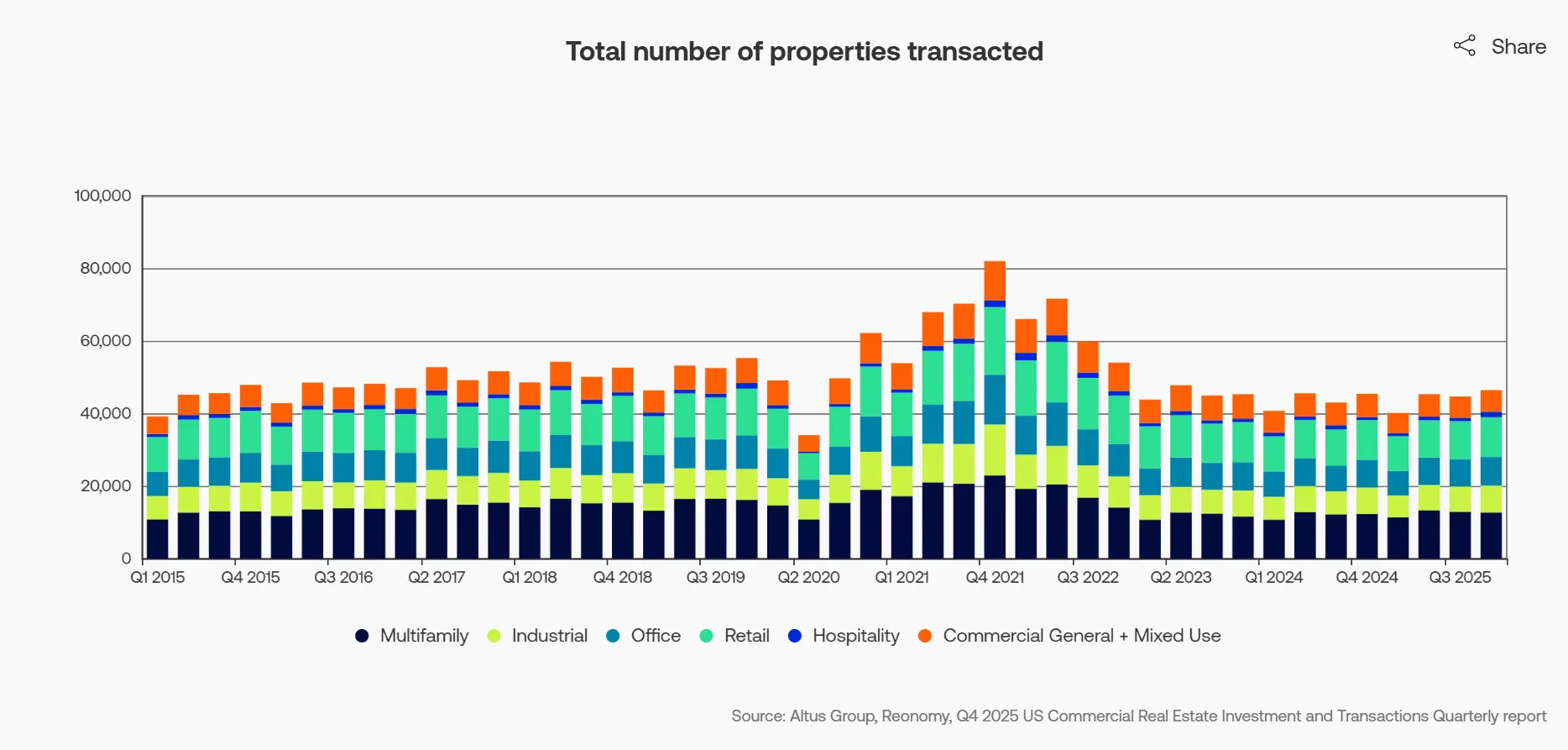

- US commercial real estate transactions in Q4 2025 rose 3.9% quarter over quarter and 2.2% year over year, led by hospitality, office, and multifamily.

- Total CRE transaction volume reached $179.9B in Q4, a 20.7% increase from Q3 and up 20.2% year over year.

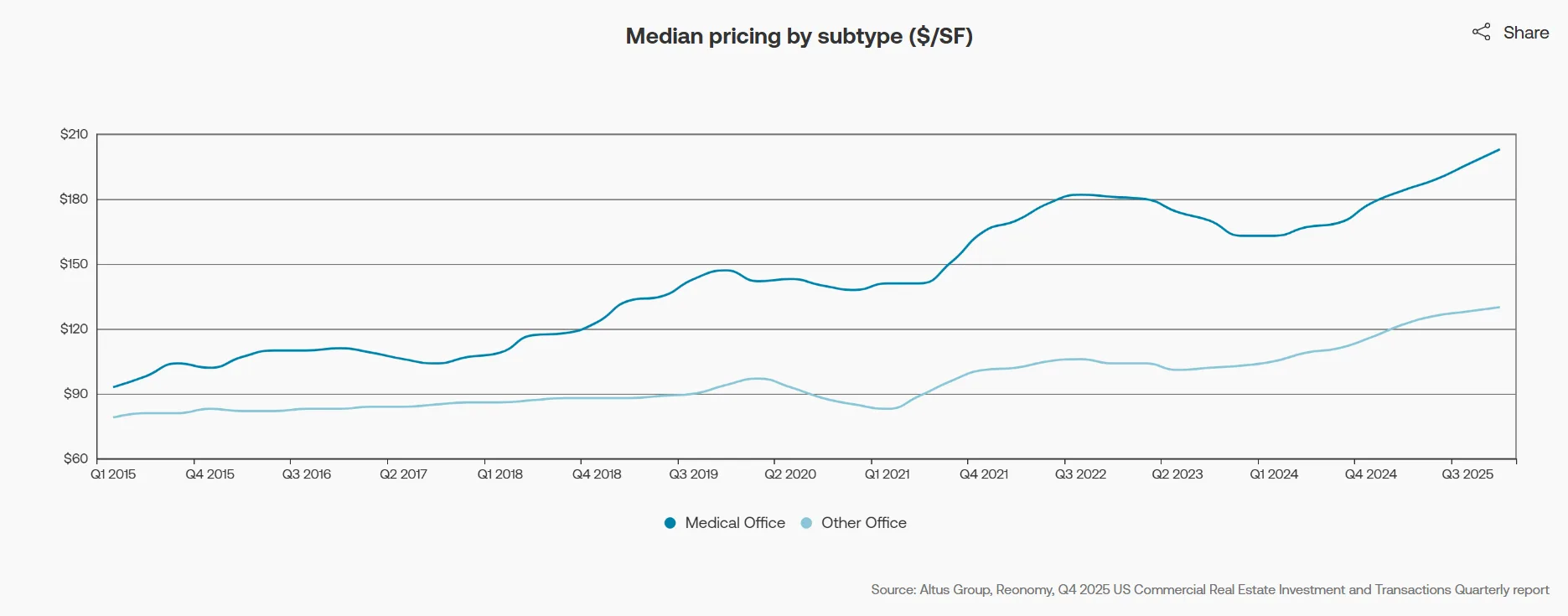

- Median pricing for single-asset CRE deals increased 2.5% quarter over quarter and 12.1% compared to Q4 2024, with all major sectors seeing gains.

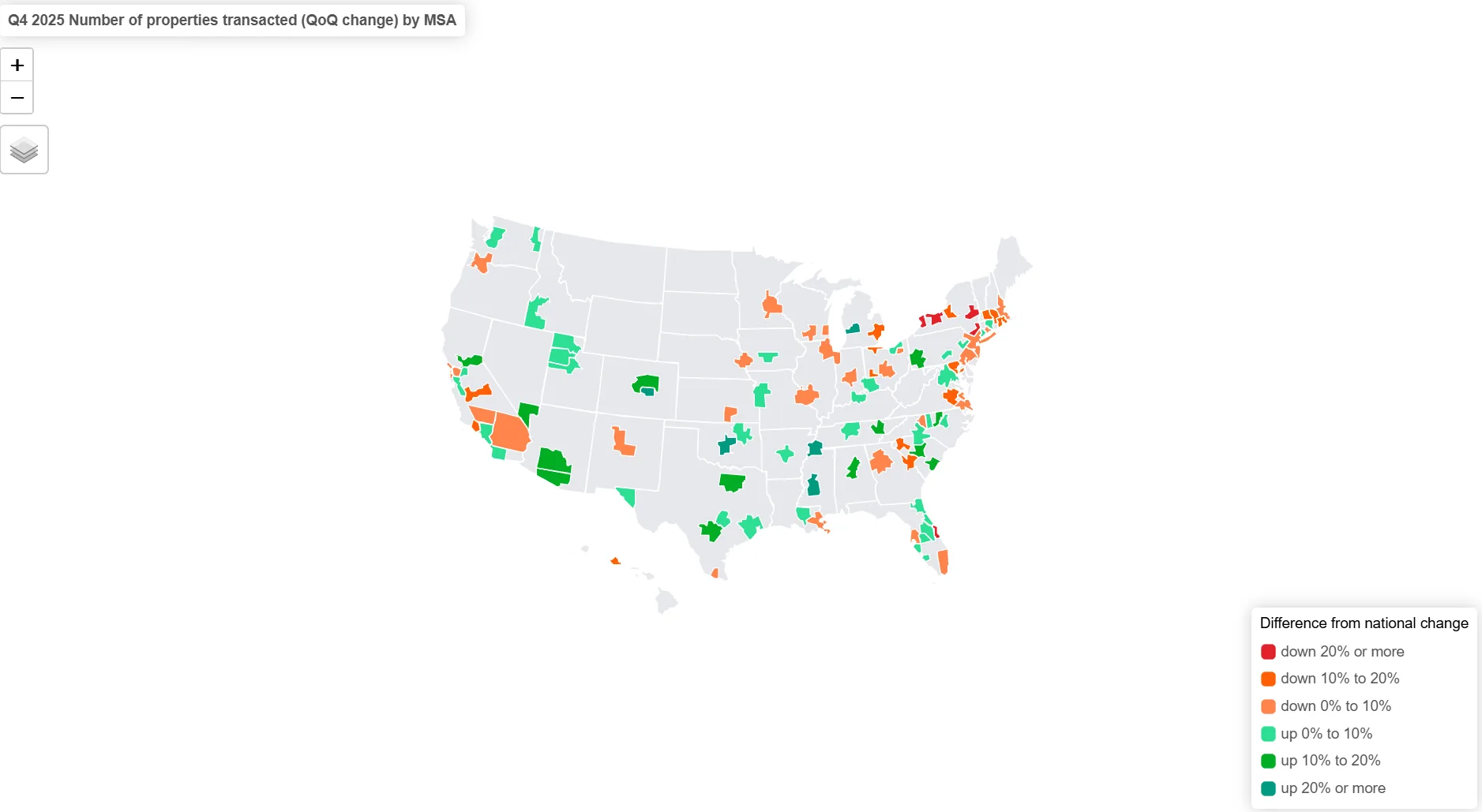

- Major MSAs saw varied CRE pricing trends, with markets like Chicago, Dallas, and Phoenix posting gains across sectors, and declines in Los Angeles and DC office.

CRE Transactions Rebound

US commercial real estate transactions saw renewed activity in Q4 2025, according to Altus Group’s quarterly report. A total of 46,395 properties changed hands, marking both quarterly and annual increases in deal volume, with hospitality and multifamily leading growth by property count and dollar value.

National CRE transaction volume jumped to $179.9B for the quarter, up over 20% both sequentially and year over year. Full-year 2025 data confirmed the rebound, with 176,445 properties trading and total volume of $560.2B, representing a 14.4% annual increase—the second consecutive year of growth.

Transaction Volume and Pricing Trends

Industrial properties dominated by dollar volume, reaching $44.9B in Q4—up 54.4% year over year and representing nearly a quarter of total activity. Multi-property, general commercial, and hospitality sectors posted even higher year-over-year dollar volume percentage gains, outpacing the overall market.

Median CRE pricing for single-asset transactions climbed 2.5% quarter over quarter and 12.1% year over year in Q4. Retail and multifamily led annual price gains (13.4% and 12.4%, respectively), while industrial prices advanced 10.9%. Since pre-pandemic Q4 2019, median price per PSF for single-property sales is up 58.5%, led by industrial at 83.8% growth, building on longer-term shifts in capital flows and asset preferences that have reshaped the market over the past quarter century.

Sectors and Submarkets

Most CRE subsectors logged quarterly price increases, with storage (+10.9%) and general commercial (+6.4%) leading. Manufacturing was the only sector to see annual median price declines. Transaction velocity remains below pre-pandemic levels, but all sectors posted higher annual median deal sizes, led by multifamily (+19.9%) and office (+19.3%).

Among the largest metropolitan areas, CRE pricing trends diverged: Chicago, Dallas, and Phoenix showed across-the-board gains, while Los Angeles and Washington, DC, recorded significant declines in select property types. Washington, DC, retail saw the biggest annual spike (+39.6%), while its office sector experienced the steepest drop (-39.1%).

What’s Next for CRE Activity

The Q4 2025 CRE data suggests a broad-based recovery in investment activity and pricing, with most property types and markets outperforming or keeping pace with national trends. Industrial and multifamily persist as key drivers of growth, while hospitality rebounded sharply in quarterly volume. Sector and market-level divergences remain, underscoring the need for localized market intelligence as CRE capital continues to flow in 2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes