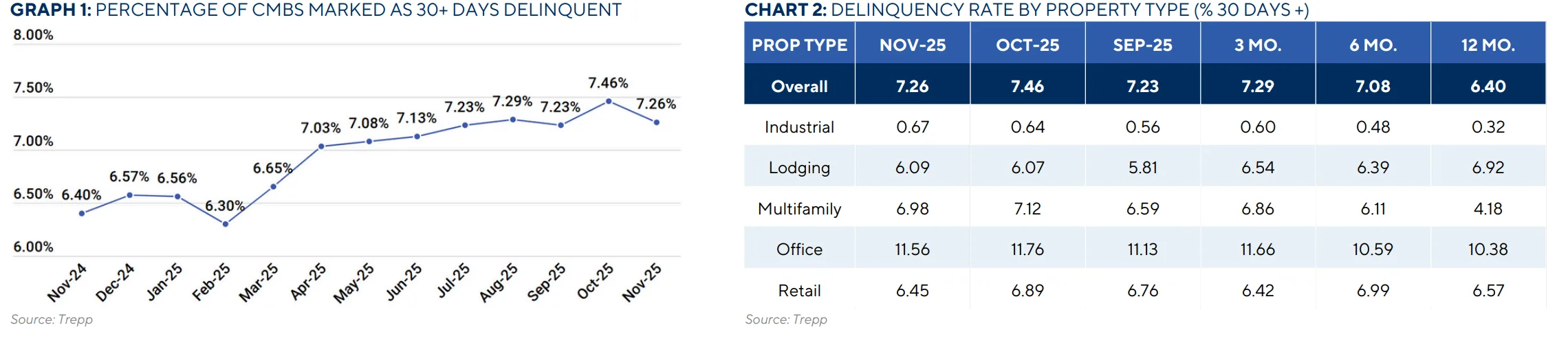

- The overall CMBS delinquency rate declined by 20 basis points in November to 7.26%, following a rise in October.

- Lodging and industrial were the only major sectors to post delinquency increases, with lodging rising 10 bps to 6.17% and industrial inching up 3 bps to 0.67%.

- Despite a lower delinquency rate, the seriously delinquent loan share (60+ days, foreclosure, REO, non-performing balloon) remained elevated at 7%.

- Retail, multifamily, and office saw month-over-month improvements, although net new delinquencies still outpaced cures in several cases.

November’s Numbers Show Mixed Signals

The US commercial mortgage-backed securities (CMBS) delinquency rate declined in November after rising in October. According to Trepp, the overall delinquency rate fell by 20 basis points to 7.26%, its fourth drop of the year. The improvement was driven by a $760M reduction in delinquent balances, coupled with a $5.8B increase in total outstanding CMBS loan volume.

However, the decline doesn’t tell the whole story.

Property Sector Breakdown

Out of the five major property types tracked by Trepp:

- Lodging had the largest rate increase, up 10 basis points to 6.17%, driven by more than $170M in net new delinquencies.

- Industrial ticked up slightly, rising 3 bps to 0.67%, continuing a modest upward trend that started in October.

- Retail experienced the biggest decline, falling 15 basis points to 6.45%, even as it recorded $247M in net new delinquencies—indicating that overall balance growth helped offset the rate.

- Multifamily dipped below the 7% mark again, improving by 14 bps to 6.98%, despite a net new delinquency increase of $45M.

- Office, still the most distressed sector, declined slightly by 8 basis points to 11.56%, though it added $88M in net new delinquencies. The sector continues to face record-setting stress levels, particularly following a steep rise in October that caught the market’s attention.

Performance by Delinquency Stage

- Seriously delinquent loans (60+ days late, in foreclosure, REO, or non-performing balloons): 7%, down 1 basis point.

- 30-day delinquent loans: 0.26%, down 21 basis points.

- Performing matured balloon loans: 1.55%

- Non-performing matured balloon loans: 2.43%

If defeased loans were excluded, the overall delinquency rate would have been 7.43%, still 22 bps lower than October.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

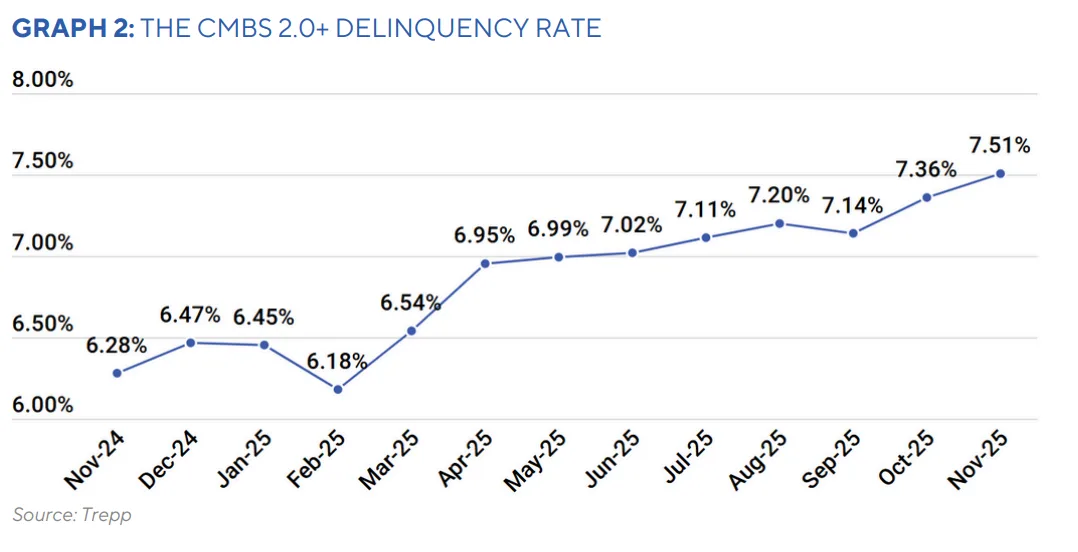

CMBS 2.0+ Update

Delinquencies in CMBS 2.0+ (issued post-2008 with tighter underwriting standards) mirrored broader market trends. The delinquency rate declined to 7.17%, with:

- Lodging up 9 bps to 6.09%

- Industrial up 3 bps to 0.67%

- Multifamily down 14 bps to 6.98%

- Office down 10 bps to 11.56%

- Retail down 15 bps to 6.45%

The share of seriously delinquent 2.0+ loans increased slightly to 6.91%.

Why It Matters

November’s report signals some stabilization in CMBS performance, but challenges remain. Rising delinquencies in lodging and industrial, alongside persistent weakness in office, point to sector-specific pressures despite broader improvements. Developers, investors, and lenders will continue watching for signals of distress, especially as debt maturities and refinancing hurdles loom in 2026.

What’s Next

While the CMBS market saw a breather in November, Trepp data suggests the recovery is uneven. With the delinquency rate still nearly 90 bps higher year-over-year, and serious delinquencies making up 7% of the market, ongoing monitoring is crucial. Expect further volatility in 2026 as economic conditions evolve and large volumes of CMBS debt approach maturity.