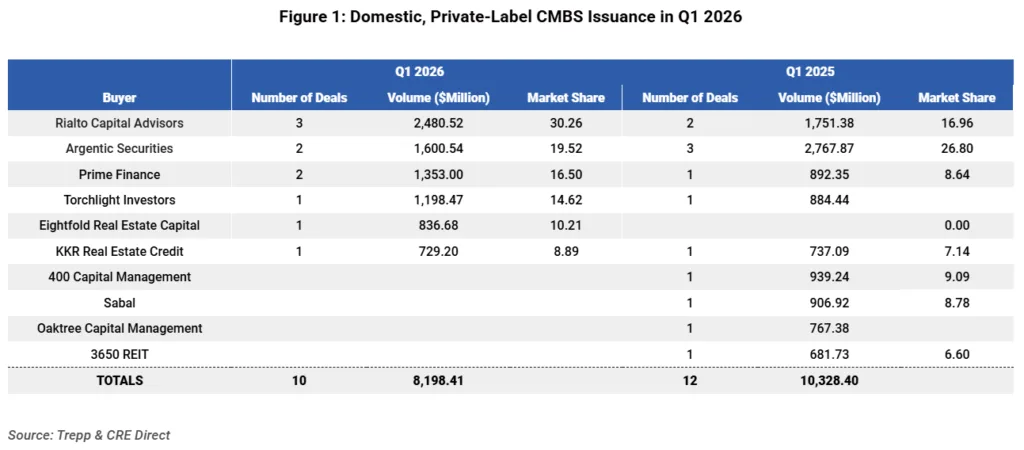

- Rialto Capital took a 30.26% share of CMBS conduit B-piece buys in Q1 2026.

- Blue Owl led overall risk-retention, particularly in SASB deals, acquiring $322.41M in risk strips.

- Conduit CMBS issuance dropped over 20% year-over-year to $8.2B amid market volatility.

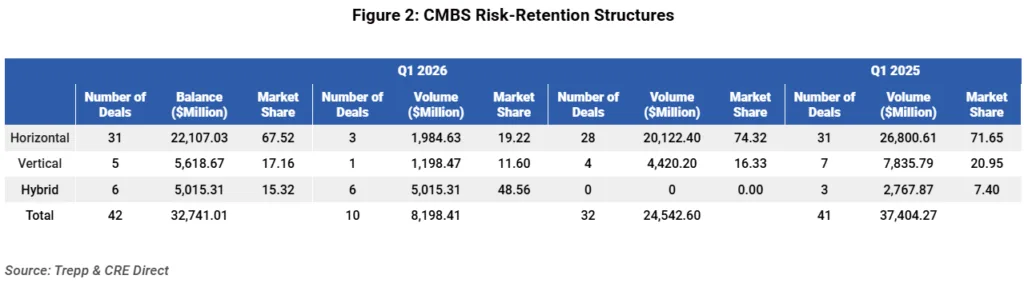

- Hybrid risk-retention structures dominated, accounting for six of ten conduit transactions.

Conduit B-Piece Activity Slows

Rialto Capital Advisors led CMBS conduit B-piece acquisitions in the first quarter. The firm bought the most subordinated tranches in three of ten deals this year. According to Trepp, Rialto secured a 30.26% market share. This performance placed it ahead of Argentic Securities and Prime Finance, which each completed two purchases. Meanwhile, issuance slowed. Total volume reached $8.2B, down more than 20% from Q1 2025. Global uncertainty and wider bond spreads continued to pressure deal activity.

Risk Retention Preferences Emerge

Regulatory rules require CMBS issuers to retain a 5% stake in each deal. In Q1, most conduit transactions favored hybrid risk retention: six deals totaling $5.02B used this approach, blending horizontal and vertical slices. Horizontal-only risk strips, often absorbing first losses, yielded between 16.63% and 21.25% based on position in the capital stack. Single-asset, single-borrower (SASB) deals mainly employed horizontal retention.

Blue Owl Rises in SASB Sector

Blue Owl Capital became the most active risk-retention buyer overall, securing horizontal strips in eight SASB deals worth $322.41M—over 17% of all new-issue CMBS risk sold in Q1. This comes as parts of its broader portfolio face pressure from rising vacancies and tenant instability, highlighting diverging performance across its holdings. Its major investments included risk pieces in the $1.87B Extended Stay America Trust and the $1.5B SLG Office Trust, which made up more than half its activity.

Industry Outlook

With market volatility, CMBS conduit issuance has lagged, but leading players like Rialto and Blue Owl are solidifying their roles in B-piece and risk-retention markets. Hybrid deal structures appear increasingly popular as issuers navigate uncertainty and adapt to evolving investor demand.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes