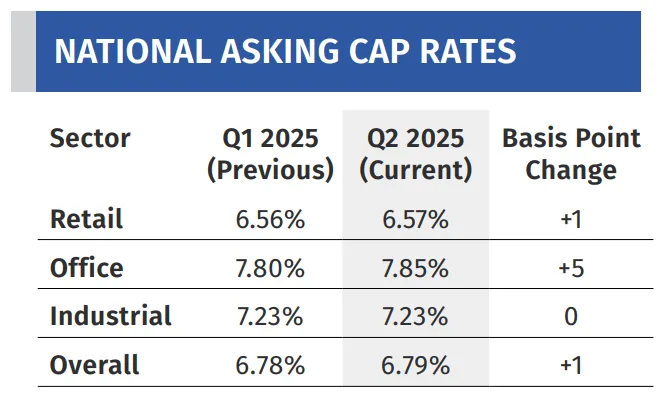

- Cap rates stabilize after years of increases, with Q2 2025 seeing just a one basis point rise to 6.79%, signaling a shift toward market normalization.

- High-credit tenants like 7-Eleven and Chase Bank continue to draw sub-6% cap rates, while brands facing challenges—like Walgreens—are trading above 7%.

- QSR and industrial sectors remain active, with Chick-fil-A and McDonald’s ground leases fetching the lowest cap rates, and industrial listings rising 10.8% in Q2.

- Lease duration remains critical, with longer leases consistently attracting lower cap rates and shorter terms seeing premiums above 7%.

A Market at a Turning Point

Per GlobeSt, after a turbulent stretch driven by interest rate hikes and macroeconomic uncertainty, the single-tenant net lease (STNL) market is showing signs of equilibrium. According to The Boulder Group’s Q2 2025 report, cap rates across the sector rose marginally—by just one basis point to 6.79%—marking a potential new phase of stability for investors and developers alike.

Sector Breakdown

Retail cap rates inched up to 6.57%, while the office segment saw a larger increase to 7.85%, continuing to reflect investor caution. Industrial rates held steady at 7.23%, buoyed by steady demand and a surge in listed properties. The report cites the Federal Reserve’s pause on rate hikes and improved investor adaptation to current financial conditions as key reasons behind the cap rate stabilization.

Quality Tenants Command Premiums

Cap rate compression is evident among high-credit tenants. A 7-Eleven in Summerville, SC, traded at a 5.27% cap rate with 15 years remaining, while a Chase Bank in Virginia sold at 4.75% with 14 years left. By contrast, a Walgreens in Florida sold at a 7.13% cap rate, underscoring investor caution toward tenants under corporate pressure.

QSRs Lead Investor Appetite

The quick service restaurant (QSR) sector continues to attract premium pricing. McDonald’s and Chick-fil-A ground leases are trading at some of the lowest cap rates in the market—4.38% and 4.45%, respectively. Meanwhile, Starbucks and Panera Bread saw modest increases in rates to 6.40% and 5.75%.

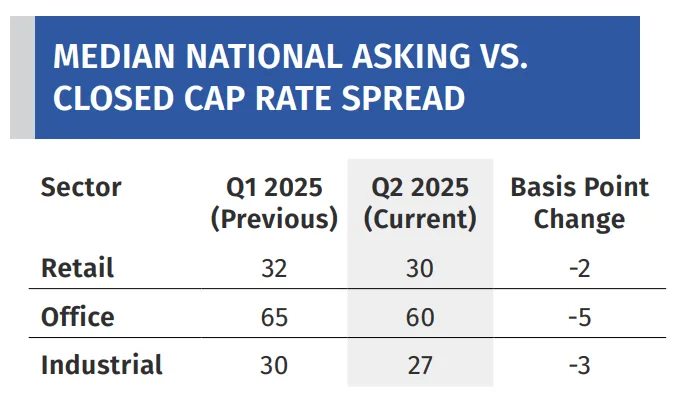

Bid-Ask Spreads Narrow, Transactions Rise

Although transaction volumes remain below past peaks, a narrowing gap between asking and closing cap rates—just 30 basis points for retail and 27 for industrial—suggests that buyer and seller expectations are aligning, a positive sign for liquidity.

Industrial Activity Ramps Up

Industrial properties saw the largest uptick in market listings, rising 10.8% in Q2. Recent deals illustrate the wide cap rate range based on asset quality: a Frito-Lay facility in Washington sold for $25.4M at a 5.99% cap rate, while an Ascend site in Tennessee traded at a much higher 9.65%.

Lease Length Drives Pricing

Across all asset types, longer lease terms are translating to lower cap rates. Auto parts stores with leases of 16–20 years are selling near 5.60%, whereas those with under five years are exceeding 7.90%. Similarly, Dollar General locations with less than three years left on their lease are reaching 9% rates.

What’s Next

While the STNL sector isn’t expected to return to previous transaction highs, current trends point to a more stable and resilient market. Experts forecast increased momentum through the remainder of 2025, with investors continuing to prioritize tenant credit quality, lease terms, and macroeconomic signals—particularly from the Fed.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes