- Build-to-Rent (BTR) sector faced a supply shock in 2025 but is stabilizing into 2026.

- Demand remains robust, driven by affordability issues for homeownership and ongoing demographic shifts.

- New development has slowed, easing pressure on rents and vacancies.

- Investment and capital market activity is cautious but showing signs of renewed momentum.

Sector Overview: Reset Sets Stage for Recovery

The Build-to-Rent (BTR) market is emerging from a volatile 2025 marked by a supply glut, reports Northmarq. Aggressive development between 2021 and 2023 led to higher vacancies and modest rent declines as new inventory outpaced immediate demand. Now, a deceleration in supply is setting the foundation for sector recovery in 2026, with demand fundamentals remaining intact.

Why Demand Remains Strong

Core drivers continue to underpin Build-to-Rent demand. Homeownership remains out of reach for many, with average mortgage payments roughly $1,000 higher per month than BTR rents. Demographic shifts—older, higher-income renters and declining first-time homebuyer rates—are keeping people in rental homes longer. Household formation has added over 1.2M renter households since 2023, supporting stable occupancy even amid slower job growth.

Supply Relief Eases Market Pressure

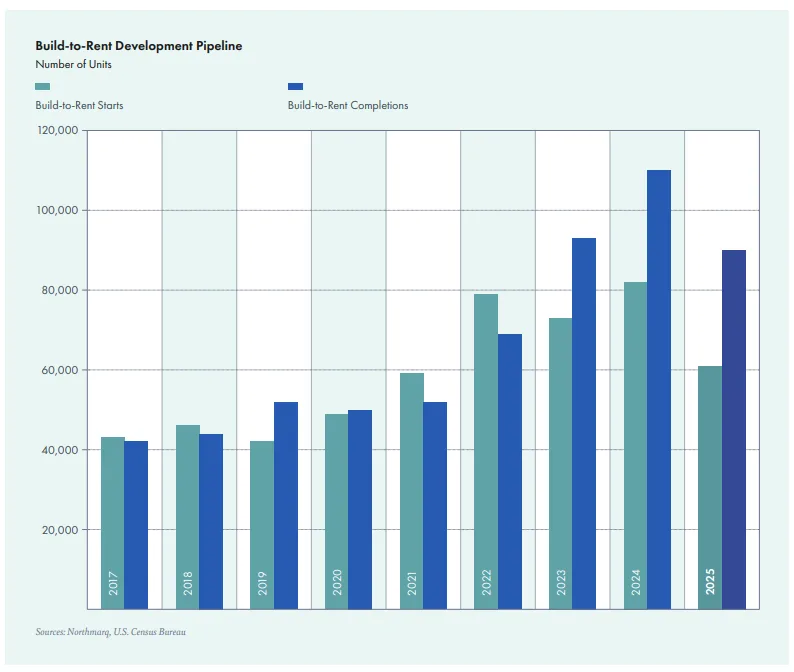

The Build-to-Rent sector delivered about 90,000 units in 2025, down from 110,000 the previous year. Developers sharply reduced new starts by 23% year-over-year, leading to a quick slowdown in pipeline activity. While Sunbelt markets like Texas and Florida have begun to saturate, capital is shifting to the Midwest and select secondary markets where fundamentals remain stronger and growth potential persists.

Stabilizing Operations and Rent Trends

Vacancies peaked nationally at around 8.8% in 2025 but have since stabilized, with key markets like Dallas showing improvement and the Midwest posting sub-4% vacancy rates. Although national BTR rents experienced a minor decline of 1.8%, there was no dramatic drop, indicating supply-driven—not demand-driven—softening. Fundamentals are expected to firm as the supply wave abates into 2026.

Get Smarter About What Matters in Texas

Subscribe to our free newsletter covering the biggest commercial real estate stories across Texas — delivered in just 5 minutes.

Investor Sentiment and Capital Flows

Capital markets remain cautious amid uncertainty, particularly regarding potential regulatory changes affecting institutional ownership. That caution is partly tied to growing political scrutiny around large-scale investor ownership of rental housing, which has introduced a layer of policy risk into underwriting assumptions. Debt financing is still available, though construction loans are tighter. Most equity is targeting joint ventures and structured deals, with pricing per unit recovering slightly but still below 2022 peaks. Cap rates have normalized around 5.5%.

Notable Markets and Emerging Trends

Southeast and Dallas-Fort Worth remain leaders in Build-to-Rent activity, with strong absorption and job growth underpinning robust fundamentals. Secondary markets like Kansas City have emerged as attractive alternatives, showing above-average rent growth and constrained supply pipelines. As primary markets mature, investor focus is expanding to locations with higher growth potential.

Outlook: Transition Year for Build-to-Rent

Looking ahead to 2026, the Build-to-Rent sector is poised for stabilization as supply pressures recede and fundamentals improve. Vacancy rates are expected to decline and rents to resume modest growth. Interest rate trends may influence both rental and homeownership demand, while policy risks around institutional rental ownership could impact future investment strategies. The sector’s evolution will be defined by operational efficiency and strategic market selection rather than aggressive expansion.