- Big box industrial demand rebounded in 2025, with net absorption nearly doubling from the first half to 85.6M SF.

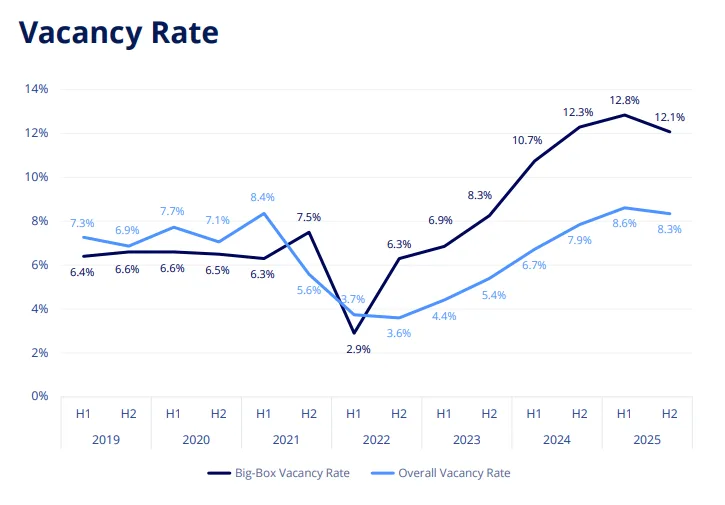

- Construction activity declined by 70% since the 2022 peak, helping vacancy rates fall to around 10%.

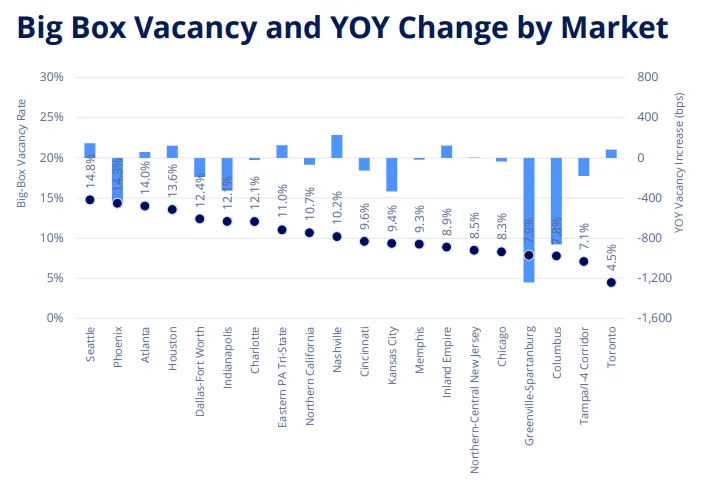

- Inland markets like Dallas-Fort Worth, Columbus, and Greenville-Spartanburg are outperforming coastal regions.

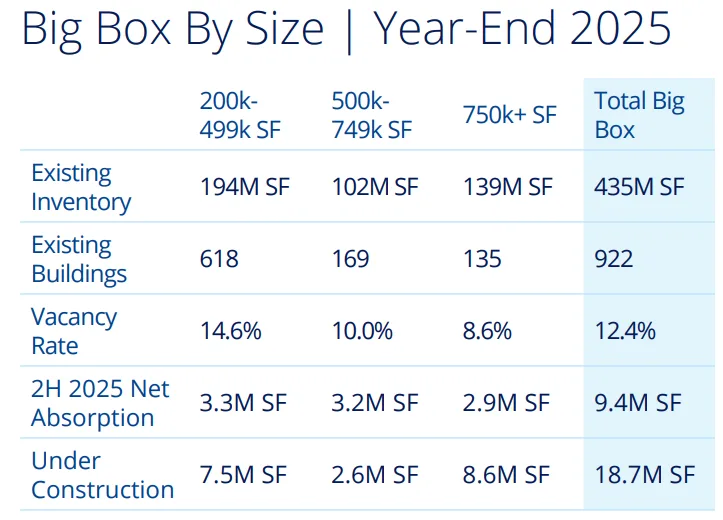

- Large-scale facilities over 750 KSF remain in highest demand, while smaller big box assets face higher vacancy.

Sector Moves Toward Balance

The big box industrial market, made up of warehouses and distribution buildings over 200 KSF, is stabilizing after years of pandemic-driven volatility. Colliers reports that a period of oversupply in 2023 and 2024 has given way to strengthening fundamentals as of late 2025. Demand has rebounded, supply additions have slowed, and vacancy rates are moving downward—signaling a more balanced market environment.

Leasing Activity Surges

Leasing momentum accelerated in the second half of 2025, with new deals totaling roughly 145.6M SF. The demand recovery is diversified, led by third-party logistics providers, retailers adjusting for omnichannel sales, e-commerce, and reshoring manufacturers. This broad tenant base makes big box industrial less vulnerable to cyclical disruptions.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Development Pullback Eases Pressure

Construction starts dropped sharply, with only 113M SF underway at year-end 2025—a 70% reduction from the sector’s 2022 peak. Most current projects are build-to-suit, with less speculative supply coming online. Fewer completions have allowed demand to catch up, bringing market vacancy down across many regions.

Vacancy and Rent Trends

The overall big box vacancy rate fell to around 10% by the end of 2025. Larger facilities (over 750 KSF) show the lowest vacancy, while mid-size and smaller big box buildings see more slack. Average asking rent is holding at $8.69 PSF, with increases moderating as the market finds its footing and tenants regain leverage in negotiations.

Regional Variations Emerge

High-growth inland markets such as Dallas-Fort Worth, Phoenix, Columbus, and Indianapolis lead in absorption and declining vacancy, helped by strong population growth and logistics infrastructure. Core traditional hubs like Chicago, Atlanta, and Houston also post healthy fundamentals. This divergence comes as some previously overheated logistics corridors continue working through excess supply, even as top inland leasing markets maintain strong momentum. Coastal regions—particularly the Inland Empire and Northern California—face more supply overhang and slower improvement.

City Highlights

- Atlanta: Net absorption turned positive in late 2025 as vacancy dropped to 14%

- Charlotte: Vacancy fell to 12.1%, fueled by major tenants including Walmart and Amazon

- Chicago: Vacancy dropped to 8.3%, with surging leasing momentum

- Cincinnati & Columbus: Columbus vacancy dipped from 16% to 7.8%, Cincinnati to 9.6%

Long-Term Demand Drivers

Big box industrial demand is sustained by evolving e-commerce, supply chain optimization, onshoring, and infrastructure investment. Larger, more efficient facilities are increasingly favored for meeting modern distribution requirements. Markets with robust transport access and growing populations remain best positioned for future growth.

Outlook for 2026

The outlook for big box industrial is positive heading into 2026, with continued but gradual vacancy declines, steady absorption, and restrained construction. While macroeconomic risks remain, the sector’s disciplined approach and diverse tenant base suggest ongoing stability and long-term resilience.