- Bank lending capacity for commercial real estate (CRE) is set to increase under proposed capital rule changes.

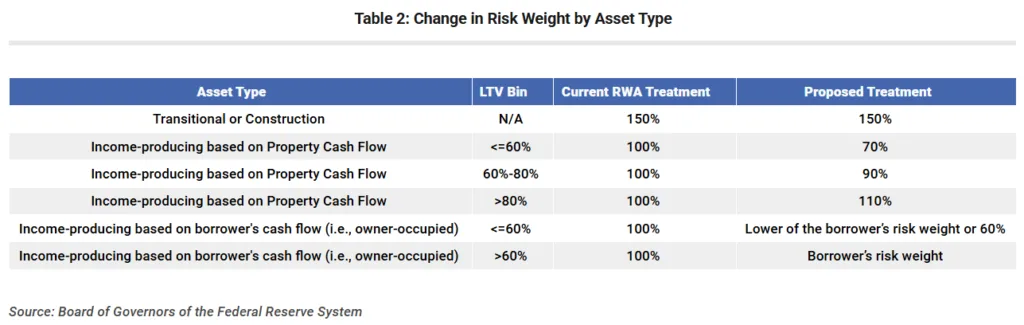

- Risk weights for CRE loans will be tied to loan-to-value (LTV), changing the capital cost of different loan types.

- Lower-leverage stabilized CRE assets could see reduced capital charges, improving bank competitiveness with non-bank lenders.

- Higher-leverage or transitional loans may not benefit, keeping non-bank lenders advantaged in riskier segments.

Expanded Bank Lending Capacity

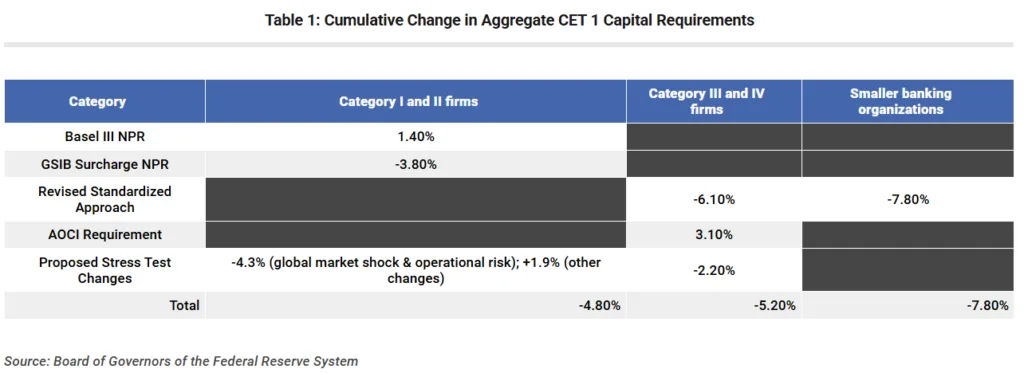

Banks play a pivotal role in the $4.9T US income-producing debt market and half the broader $6.1T commercial mortgage market. Recent proposals from the Fed, FDIC, and OCC would ease bank capital requirements, releasing regulatory buffers to support new CRE lending, reports Trepp. If passed, major banks could redeploy a portion of $175B in excess capital, providing a potential supply boost for CRE borrowers.

Risk-Weighting Changes Favor Lower Leverage

Under the proposed rules, risk weights for CRE loans will now scale with LTV rather than applying a flat treatment. Well-underwritten, stabilized properties with lower leverage will attract lower risk charges, encouraging conservative lending. Higher-leverage deals, however, face 10% larger capital charges, potentially limiting their benefits from the new framework, a shift that comes as banks are already positioning for a potential rebound in CRE lending activity as financing conditions evolve.

Competitive Dynamics with Non-Bank Lenders

The risk-weight shift could allow banks to offer more competitive pricing on loans for lower-leverage, stabilized CRE assets, closing the gap with non-bank lenders. However, higher-leverage and transitional deals, often outside the scope of the most favorable treatment, will likely remain the domain of non-banks that specialize in higher risk and speedier execution.

What’s Next

The proposals are subject to a 90-day comment period and review, with key dates approaching in June. While the rules are not final, market observers are watching closely for early moves in CRE loan pricing and underwriting as banks anticipate finalization. If lower risk weights take hold, expect to see greater bank activity and possibly tighter loan spreads for qualifying assets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes