- The national average rent rose to $1,631/month in December 2025, up just 0.6% year-over-year.

- Vacancy rates reached a record high of 8.5% as new construction outpaced demand.

- Luxury properties ended 2025 with an 11.1% vacancy rate, while low- and mid-tier vacancy rates also crept up.

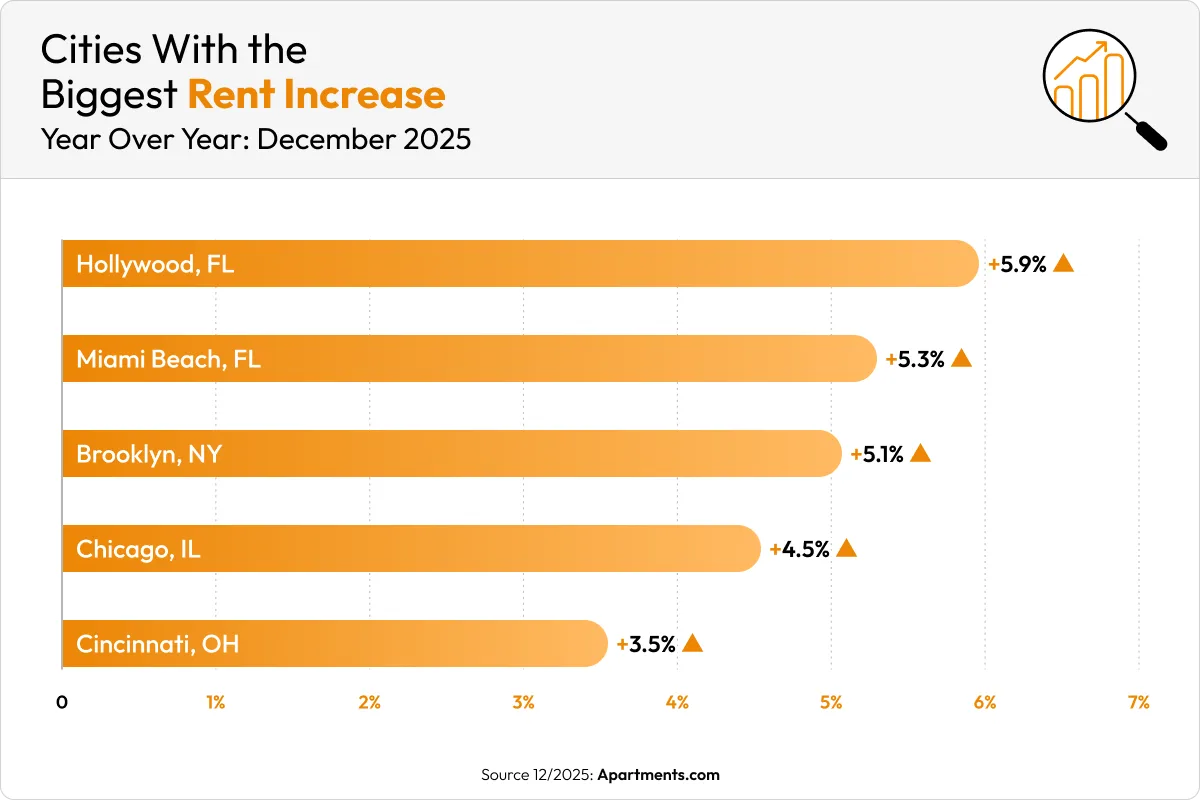

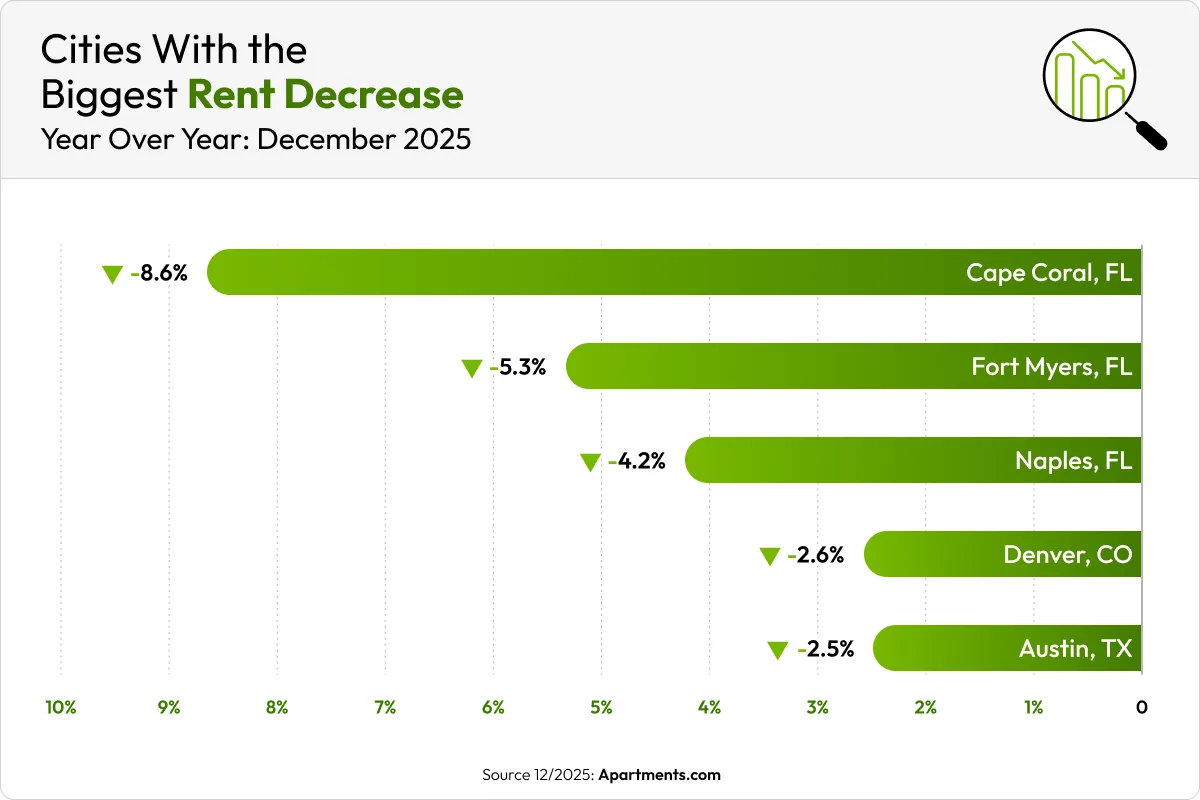

- Rent increases were most pronounced in cities like Miami Beach and Cincinnati, while Cape Coral and Fort Myers saw sharp declines.

Rent Trends Stay Flat

Apartments.com’s December 2025 rent report shows the US rental market ended the year with historically high vacancies and sluggish rent growth. The national average rent reached $1,631 per month, a 0.6% increase over December 2024. Rent growth cooled significantly compared to the post-pandemic surge, with year-end numbers reflecting a more balanced, tenant-friendly environment.

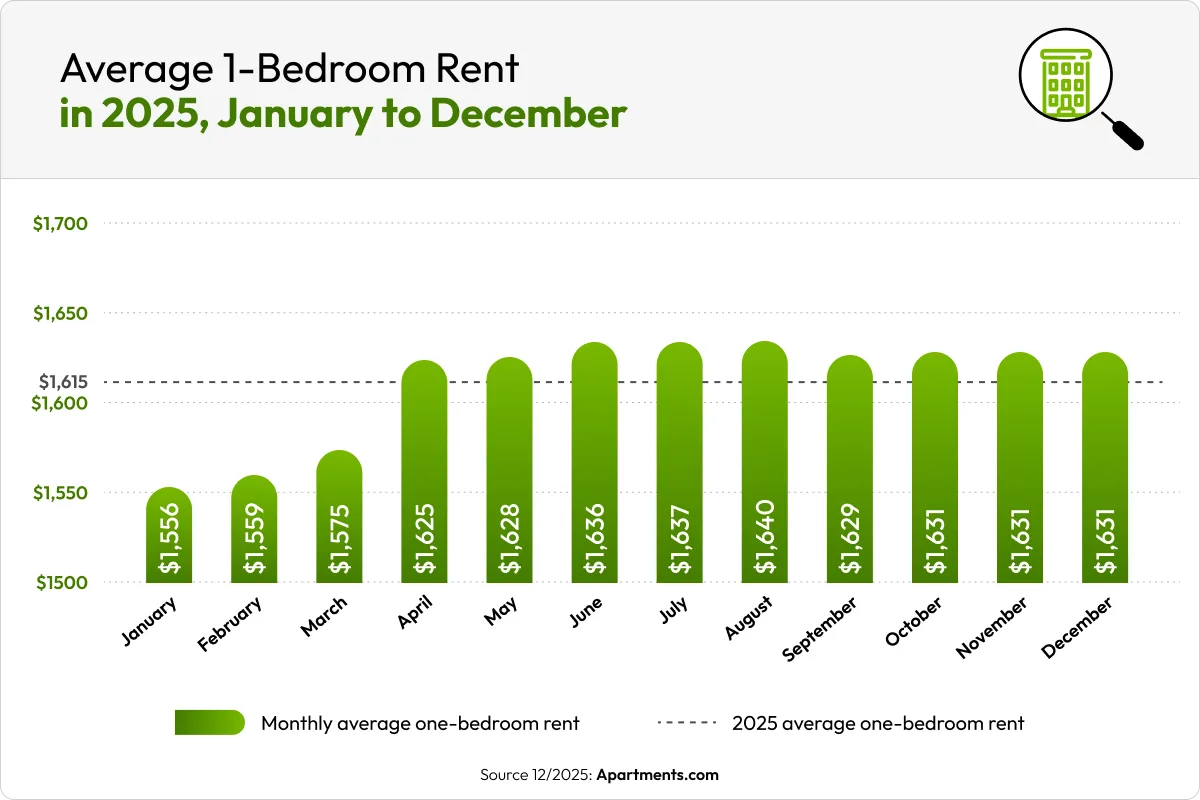

Throughout 2025, average one-bedroom rents began at $1,556/month and peaked at $1,640/month in August before settling around $1,631/month in December. The annual average for one-bedroom units landed at $1,615/month.

High Vacancy Levels Persist

Market dynamics shifted as vacancy rates reached an all-time high of 8.5% by the end of 2025. Fewer new apartment deliveries compared to past years were not enough to absorb slower leasing activity, particularly in luxury buildings. These premium properties posted an 11.1% vacancy rate, down modestly from 11.7% at the start of the year, as concessions became commonplace to attract tenants.

Low- and mid-tier property vacancies edged up while lease-ups lagged, as renters sought better amenities and value. Managers in these asset classes responded to weak demand by reducing rents — a trend likely to persist into 2026 if the supply-demand mismatch continues. This widening supply-demand gap, paired with persistently elevated vacancies, reflects broader national patterns that have been building through the latter half of the year.

Regional Rents: Leaders and Laggards

Several US housing markets diverged sharply in December. Hollywood, FL (+5.9%), Miami Beach, FL (+5.3%), Brooklyn, NY (+5.1%), Chicago, IL (+4.5%), and Cincinnati, OH (+3.5%) saw the biggest rent increases. Miami Beach and Cincinnati experienced a surge due to a larger share of new high-end product. This new supply pushed up average asking rents, even as vacancies continued to rise.

Markets with the steepest declines were Cape Coral, FL (-8.6%), Fort Myers, FL (-5.3%), Naples, FL (-4.2%), Denver, CO (-2.6%), and Austin, TX (-2.5%). These decreases signal localized oversupply and softer leasing, especially in Sunbelt markets previously marked by aggressive growth.

What’s Ahead for Apartments.com Metrics

Looking into early 2026, Apartments.com projects persistent high vacancies and a continued softening of rent growth, especially for luxury apartments. With 85% of new construction classified as luxury, property owners are expected to offer more concessions to fill empty units. As vacancy rates converge between luxury and standard properties, a wider price spread could emerge across asset classes.

Renters can expect increased flexibility and more favorable deals in upper-tier properties. Seasonal spikes are likely in spring and early summer, but analysts expect more moderate rent increases than in recent years. These Apartments.com rent trends paint a picture of a national market still adjusting to post-pandemic supply pressures and shifting renter preferences.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes