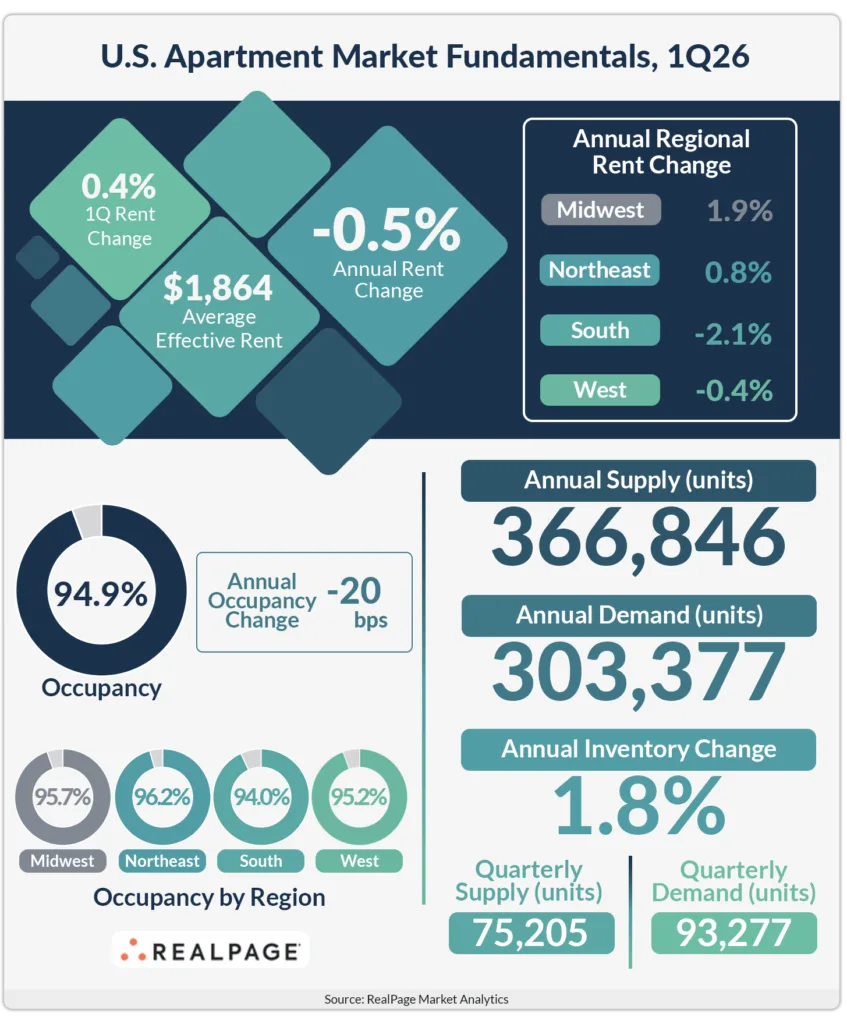

- Apartment demand reached 93,300 units in Q1 2026, reversing late 2025 move-outs.

- New supply slowed to 367,000 units annually, matching the decade norm.

- US apartment occupancy rose slightly to 94.9% but trails last year’s rate.

- Rent growth remains weak as concessions persist, especially in supply-heavy regions.

Demand and Supply Reset

RealPage reports that the US apartment market saw a strong demand recovery in the first quarter of 2026, absorbing nearly 93,300 units. This spike follows a period of net move-outs at the end of 2025. Still, annual absorption of 303,000 units remains below the decade average of 340,000.

New supply volumes continue to decelerate. Roughly 367,000 units delivered over the past year align with the 10-year average. Q1 completions totaled about 75,200 units, extending a five-quarter trend of lower deliveries following a 2024 peak.

Occupancy and Rent Trends

Overall apartment occupancy improved by 10 basis points quarter-over-quarter to 94.9% as of Q1 2026. However, occupancy remains 20 basis points below levels from a year prior. This reflects still-soft demand relative to recent years’ supply additions.

Rents reversed two consecutive quarterly declines, rising 0.4% for the quarter. Despite the uptick, effective asking rents are 0.5% below last year’s rates. Rent concessions are widespread, present in roughly 25.5% of listings, averaging 7.2% off. In some markets, incentives are becoming more targeted but richer in value, signaling that operators are shifting from broad discounting to deeper, deal-specific concessions as competition intensifies. Operators are likely to maintain incentives heading into the busy leasing season, which could further delay meaningful rent growth until concessions taper off.

Regional Differences Persist

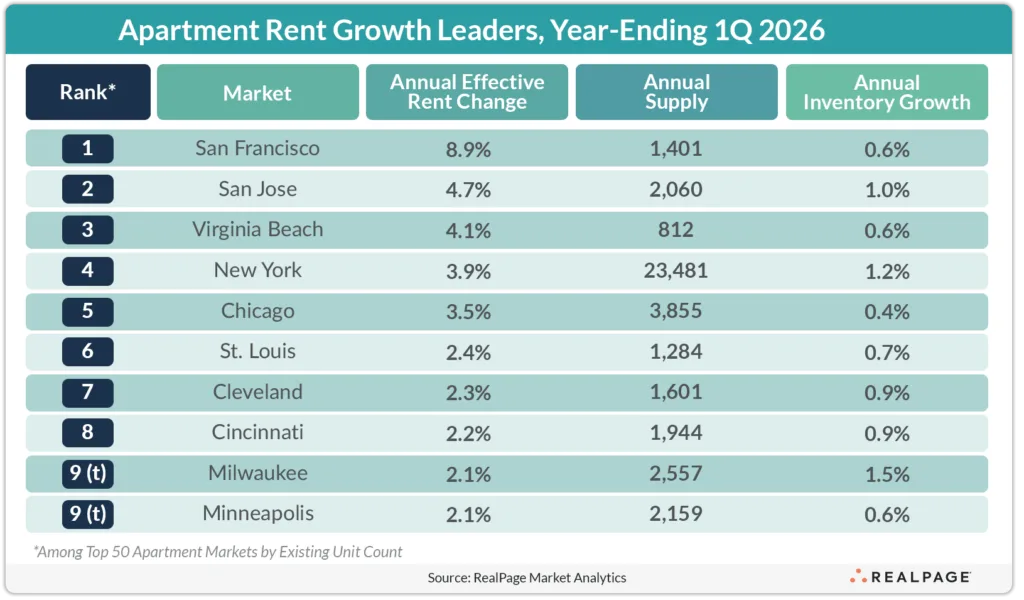

Rent cuts linger where new supply is heaviest. Markets like Austin, Denver, and Phoenix reported annual rent declines of 7%, 6%, and 5%, respectively. Tourism-driven metros including San Antonio, Tampa, Nashville, and Las Vegas also experienced ongoing softness, often an early sign of broader economic pressure as discretionary spending slows.

Meanwhile, coastal tech hubs such as San Francisco, San Jose, and New York posted positive rent growth, bolstered by return-to-office efforts and AI sector optimism. Virginia Beach led growth with over 4% year-over-year. Midwest markets with limited new builds—Chicago, St. Louis, Cleveland, Cincinnati, Minneapolis, and Milwaukee—posted steady rent gains of 2% to 4%.

What’s Next

Apartment demand has rebounded, but supply levels and widespread concessions are tempering rent growth. With regional disparities evident, operators are likely to focus on occupancy and incentives through peak leasing season, watching closely for shifts in consumer and economic sentiment that could reshape apartment fundamentals in coming quarters.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes