- US megacaps rebounded strongly in 2025, powered by AI, after a turbulent start that temporarily disrupted American market leadership.

- AI investment has expanded into power and infrastructure sectors, strengthening the US’s lead in R&D, productivity, and reinvestment capacity.

- Private credit is playing a growing role in funding the AI build-out, but structural risks in semi-liquid fund vehicles could challenge market stability.

Historic Shifts, Uncertain Paths

Ashley Lester, MSCI’s Chief Research & Development Officer, frames 2025 as a year marked by both political uncertainty and technological acceleration. Early in the year, the US administration shocked markets with new tariffs, triggering a rare “Triple-Red” moment—a simultaneous decline in US equities, Treasuries, and the dollar. Despite the volatility, AI’s momentum helped markets recover, especially in the US.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

AI-Led Recovery Reinforces US Leadership

Although emerging markets and Europe outpaced US equities through April, US megacaps rallied in the second half of 2025. Between May and November, they delivered over 32% in returns, significantly outperforming broader US stocks and international peers.

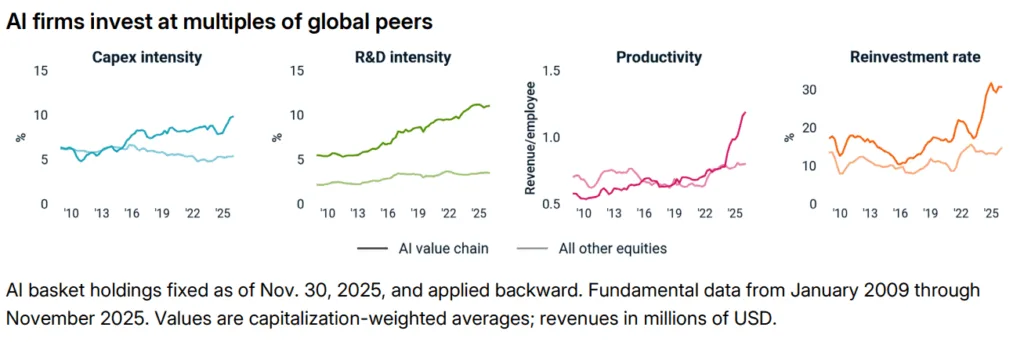

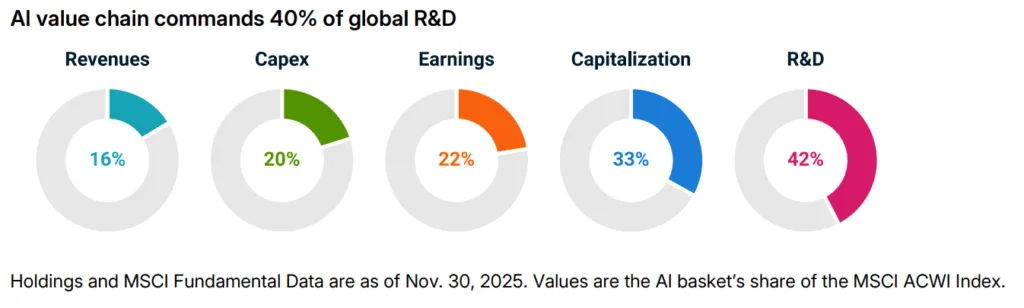

Several factors fueled this comeback. For example, American firms continue to dominate the AI value chain, which now spans nine layers—from chips to energy providers. Roughly 80% of the market capitalization in this sector remains US-based. These companies now account for:

- 40% of global R&D spending (about $600B)

- 20% of global capex (approximately $700B)

In fact, AI firms invest at far higher rates than global peers, with R&D intensity nearly four times greater. They also reinvest more of their earnings and exhibit higher labor productivity.

As a result, the US continues to lead in long-term innovation capacity. American megacaps now spend almost 10% of sales on R&D—double the rate of both smaller US companies and international competitors.

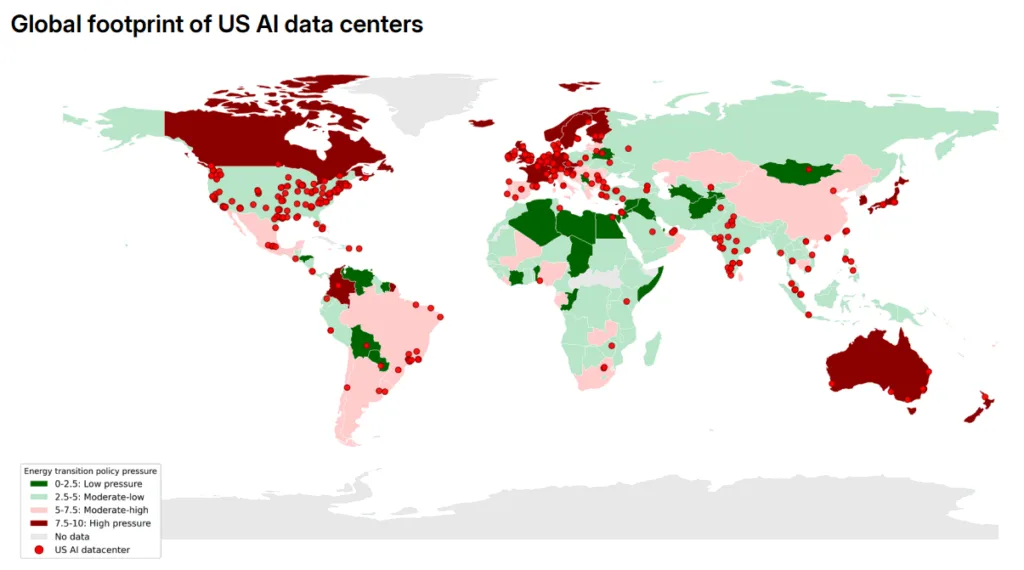

AI Infrastructure Boosts Utilities and Clean Energy

While semiconductors and data centers led earlier AI gains, 2025 saw a surge in energy and utility stocks as investors recognized the critical role of power-optimized real estate in supporting AI infrastructure at scale. According to the IEA, electricity demand from data centers is growing at 15% annually—significantly faster than overall energy use. In the US, AI-driven data centers will account for nearly half of electricity demand growth through 2030.

This energy surge reshaped market performance:

- Clean Energy Infrastructure Index: +34% YTD

- World Utilities Index: +29%

- Oil & Gas Index: Lagged at +12%

Clearly, the demand for electricity—not oil—has emerged as the key resource in the AI era.

However, China’s lead in clean tech and grid infrastructure poses a long-term strategic challenge. While the US restricts access to Chinese renewable technologies, it may be locking itself out of lower-cost solutions necessary to scale AI efficiently. This dilemma raises concerns about whether America’s energy ecosystem can support its AI ambitions sustainably.

Private Credit: A Vital but Vulnerable Capital Source

AI’s rapid expansion has required more flexible financing, and many firms have turned to private credit to meet those needs. Since 2020, annual fundraising for semi-liquid private credit funds has soared from $10B to an estimated $74B in 2025.

These funds attract investors with promises of periodic redemptions and simplified access. However, the structure still relies on fundamentally illiquid assets—multi-year loans—which introduces growing risk.

Managers have used cash buffers and credit lines to meet redemption demands. Yet these tools may falter under stress. Already, credit concerns are rising:

- 20% write-downs on senior loans have more than tripled since 2022

- 50% write-downs have impacted 13% of mezzanine loans

So far, income from performing loans has offset these losses. But if defaults increase or secondary markets freeze, the sector could face a reckoning. In essence, the industry is repeating a familiar pattern: lending long while promising liquidity short.

Outlook: Evolution, Not Revolution

Looking ahead, MSCI believes 2026 won’t bring entirely new themes—but will instead test the resilience of those already in motion. Investors must assess:

- Whether US political and institutional strength can continue to support capital markets

- If AI-related reinvestment can maintain its pace amid growing energy demands

- Whether energy infrastructure will scale fast enough to meet data center growth

- And how well private-credit vehicles can weather mounting financial stress

Although markets remain remarkably adaptive, 2025 demonstrated how quickly geopolitical or technological shifts can reshape relative performance. In 2026, the interplay among innovation, energy, and financial structures will likely determine outcomes more than any single trend alone.