- Private-credit firms including Apollo, Blackstone, and Blue Owl reported weaker quarterly returns as Fed rate cuts reduced loan yields and defaults increased.

- Several lenders marked down loan valuations, trimmed dividends, or faced redemption pressure from wealthy investors worried about liquidity and transparency.

- Despite the slowdown, major firms continue attracting institutional capital, signaling that long-term confidence in the direct lending market remains intact.

The WSJ reports that private-credit firms spent the last several years delivering some of the strongest returns in alternative assets. That run is now losing momentum. First-quarter earnings from major lenders show private credit returns cooling across the industry as lower rates, rising defaults, and investor scrutiny reshape the market.

Apollo Global Management, Blackstone, Blue Owl, Ares Capital Corp., and other lenders all reported weaker performance metrics compared with a year ago. Some firms reduced dividends or marked down the value of loans tied to software and middle-market companies, while others faced rising redemption requests from individual investors.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

From Boom Years to Normalization

Private credit emerged as one of the biggest winners of the post-pandemic financing environment. As traditional banks pulled back during the pandemic and again after the 2023 regional banking crisis, direct lenders stepped in aggressively, often earning premium yields in exchange for taking on higher-risk borrowers.

The asset class also benefited from a surge in M&A and leveraged buyout activity between 2021 and 2023, which fueled demand for private financing. According to company filings and earnings reports, some private-credit funds generated mid- to high-double-digit annual gross returns during that stretch.

Now, executives say the market is entering a more normalized phase.

Blackstone President Jonathan Gray said in a recent interview with The Wall Street Journal that the decline in returns largely reflects the Federal Reserve’s rate-cut cycle, which lowers income generated from floating-rate loans. He also pointed to a “normalization” in defaults after unusually low levels over the last two years.

The Details Behind Weaker Private Credit Returns

Apollo said gross returns in its direct origination funds fell to 0.5% in the latest quarter, down from 2.6% a year ago. Blackstone and Blue Owl also reported year-over-year declines in credit fund performance.

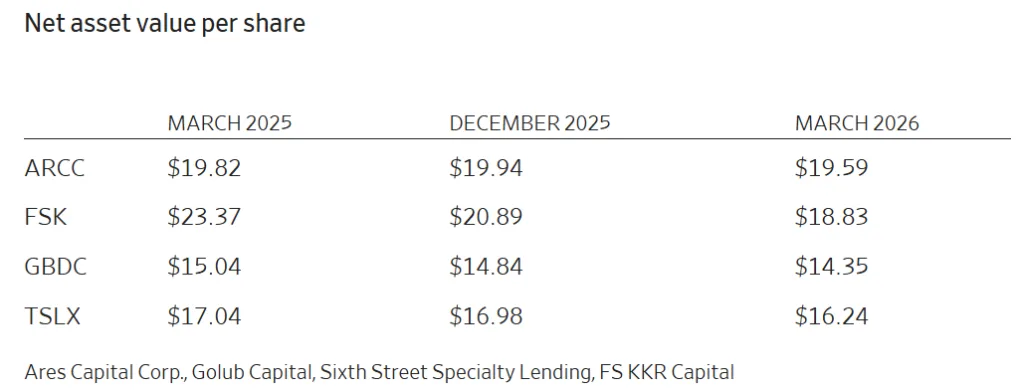

Publicly traded business development companies (BDCs) showed similar pressure. Ares Capital Corp., Golub Capital BDC, FS KKR Capital, and Sixth Street Specialty Lending all reported declines in net asset value per share after marking down portions of their loan books.

Several lenders cited stress among software borrowers, a segment private-credit firms heavily financed over the last decade because of its recurring-revenue profile. But the rise of generative AI is now creating uncertainty around the long-term viability of some software business models, increasing concerns about repayment risk.

KKR’s largest private-credit fund geared toward individual investors also reduced its dividend, adding to broader anxiety among retail allocators.

At the same time, redemption pressure is rising. Many private-credit funds cap quarterly withdrawals to prevent liquidity runs, but those limits have become a flashpoint for wealthy investors seeking faster access to cash amid market volatility.

A Transparency Push Gains Momentum

The recent volatility is also accelerating calls for greater transparency across private markets.

Apollo CEO Marc Rowan called for more consistent pricing disclosures across private credit. He said stronger transparency would help firms maintain investor trust.

Apollo plans to launch daily pricing across its private-credit funds by September. That move marks a major shift for an asset class with infrequent valuations.

Pressure remains highest in the private-wealth channel. Alternative asset managers now target individual investors for future growth. As a result, firms expanded aggressively into retail distribution and retirement accounts. Apollo also continues broadening its credit platform beyond corporate lending. The firm recently backed its first major digital infrastructure investment tied to growing data-center demand and AI capacity.

Blue Owl said fundraising declined in its private-wealth business during the quarter. However, institutional inflows still lifted total assets under management.

That divergence shows a growing split among investors. Pensions and endowments continue backing private credit. Meanwhile, retail investors remain cautious about defaults, markdowns, and liquidity limits.

Why It Matters

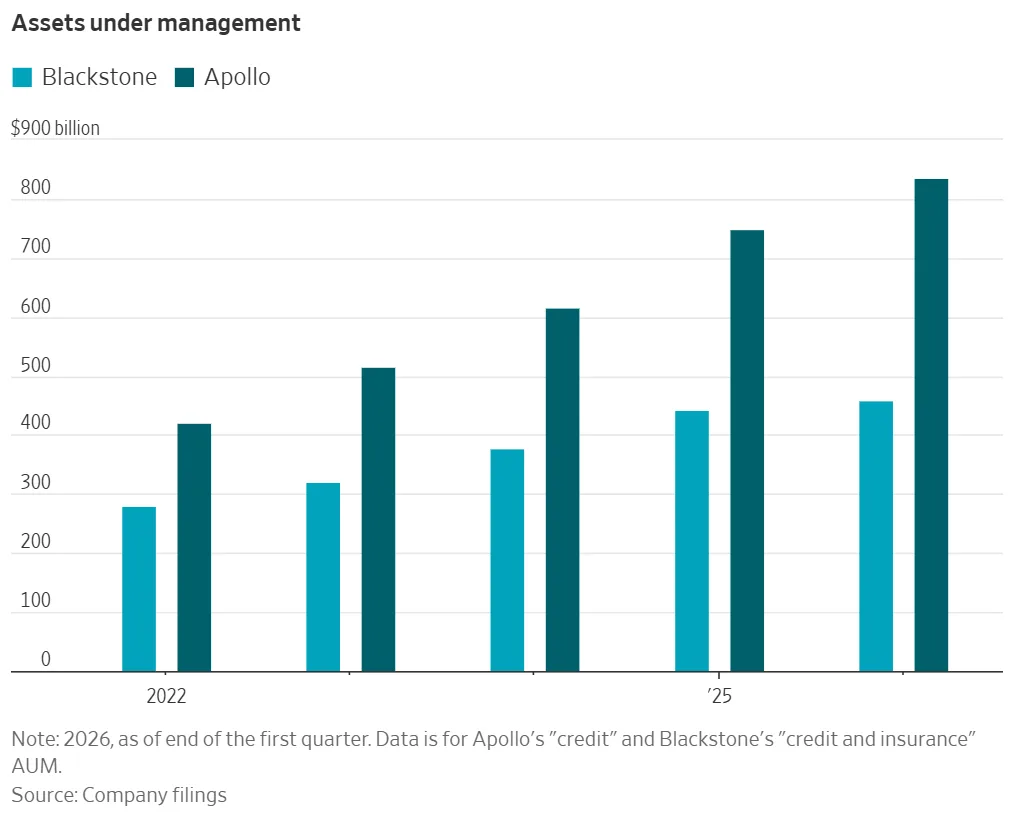

The slowdown marks a critical test for the direct lending market after years of rapid expansion. According to company disclosures, Apollo and Blackstone’s credit divisions still posted year-over-year asset growth of 30% and 18%, respectively, showing institutional demand remains strong despite weaker returns.

The industry also continues to outperform some public debt markets. A public leveraged-loan index declined 0.6% in the first quarter, while private-credit benchmarks remained positive. According to a 2026 Goldman Sachs report, the Cliffwater Direct Lending Index outperformed public loan markets in 15 of the last 21 years.

Still, the sector’s next phase may look materially different from the easy-growth environment that fueled its rise. Investors are paying closer attention to underwriting standards, borrower quality, and liquidity structures as defaults climb and yields compress.

What’s Next

Private-credit managers are likely to focus more heavily on transparency, portfolio quality, and institutional fundraising over the next several quarters. Firms with stronger underwriting track records and diversified borrower exposure could gain market share as investors become more selective.

The key question for the market is no longer whether private credit can grow—it already has. The question now is whether private credit returns can continue outperforming public markets in a lower-rate, higher-default environment.

That answer could determine how much capital continues flowing into one of commercial real estate and corporate finance’s fastest-growing asset classes.