- National advertised multifamily rents increased 0.2% month over month in April, but remained down 0.2% year over year, according to Yardi Matrix.

- Gateway and Midwest metros including New York, San Francisco, and Chicago continued outperforming, while Austin, Denver, Tampa, and Phoenix posted steep annual declines.

- Developers and operators face mounting pressure from elevated supply, softening demand, and weaker consumer confidence, though distress opportunities are beginning to emerge.

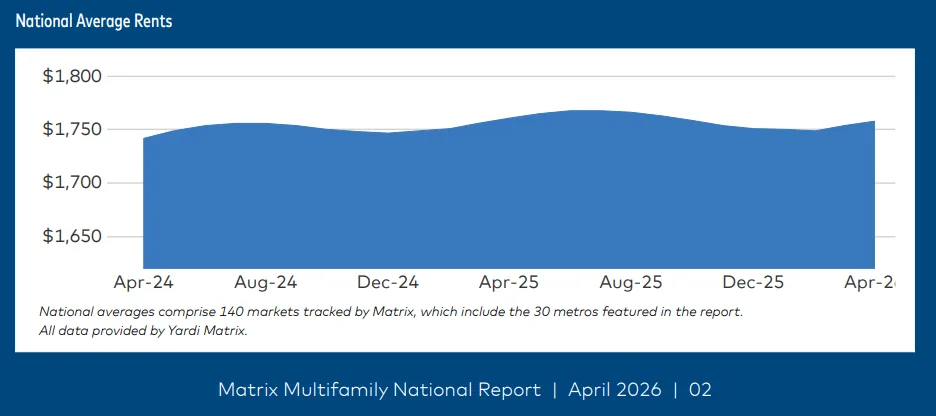

US multifamily rents posted another modest increase in April, but the broader market remains stuck in low-growth mode as supply pressures continue to outpace demand. National advertised rents rose $4 month over month to $1,758 in April, according to Yardi Matrix’s April 2026 Multifamily National Report, though rents were still down 0.2% compared to a year earlier.

The latest data reinforces a trend that has defined the multifamily market for much of the past two years: strong performance in gateway cities and Midwest metros offset by continued weakness across oversupplied Sun Belt markets. While some high-construction metros showed early signs of stabilization in April, rent growth remains far below historical norms.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Gateway Markets Pull Ahead

New York led the nation in annual rent growth at 4.8%, followed by San Francisco at 4.1% and Chicago at 3.3%, per Yardi Matrix. Midwest metros including the Twin Cities, Kansas City, Indianapolis, and Detroit also recorded positive annual gains.

Meanwhile, many of the nation’s fastest-growing pandemic-era markets continued to struggle. Austin posted the steepest annual decline at -4.3%, followed by Denver (-3.6%), Tampa (-3.4%), and Phoenix (-2.7%). Yardi noted that advertised rents are now negative year over year in 19 of the top 30 metros it tracks.

The divide largely reflects the uneven impact of new deliveries. Markets that absorbed aggressive multifamily construction pipelines over the past three years continue working through lease-up activity, limiting landlords’ pricing power.

The Details Behind Sluggish Rent Growth

National rent growth remains well below historical averages despite the start of the spring leasing season. Advertised rents are up just 0.4% year to date through April, roughly one-third of the average growth pace recorded between 2012 and 2019, according to Yardi Matrix.

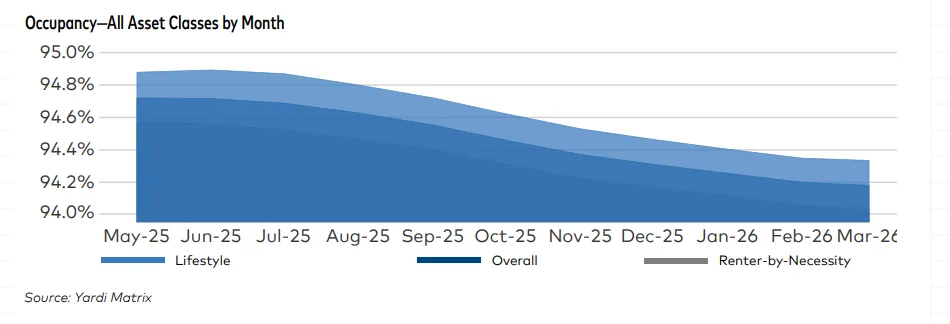

Occupancy also softened. National occupancy held at 94.2% in March but fell 50 basis points year over year. Texas metros remain among the weakest-performing markets, with Houston, Austin, and Dallas all posting occupancy below 92.5%.

At the same time, demand drivers are weakening. Yardi cited slowing population growth, softer migration trends, declining consumer confidence, and a sluggish labor market as factors constraining leasing activity. The University of Michigan’s consumer confidence survey hit a record low in April, while elevated energy costs tied to geopolitical instability have further pressured household budgets.

The supply picture also remains significant. Yardi Matrix forecasts nearly 480,000 rental units will deliver nationally in 2026, followed by roughly 450,000 annually in subsequent years. That pipeline includes market-rate multifamily, affordable housing, student housing, senior housing, and build-to-rent inventory.

Sun Belt Oversupply Still Weighs on Apartments

Despite the weak annual comparisons, several Sun Belt markets did show incremental improvement in April. Miami, Phoenix, Raleigh, Denver, Nashville, and Dallas all posted positive month-over-month rent growth, suggesting some stabilization may be forming beneath the surface.

Still, Yardi cautioned that the recovery remains fragile and uneven. Charlotte and San Diego recorded the steepest monthly declines in April at -0.4%, while Houston, Las Vegas, and Austin each fell 0.2% month over month.

The report also highlighted a growing divide between luxury “Lifestyle” properties and workforce-oriented “Renter-by-Necessity” apartments. Lifestyle rents rose 0.3% nationally in April, outperforming the 0.1% increase for renter-by-necessity units.

That gap was especially noticeable in Sun Belt metros. In Atlanta, for example, Lifestyle rents increased 0.1% while renter-by-necessity rents fell 0.4%. Nashville showed a similar pattern, with Lifestyle rents up 0.4% but renter-by-necessity rents declining 0.3%.

Build-to-Rent Faces New Policy Pressure

The report also pointed to emerging challenges in the single-family build-to-rent sector. National advertised rents for build-to-rent properties increased $7 in April to $2,211, though they remained down 0.5% year over year.

More notably, Yardi said proposed federal legislation targeting institutional ownership of single-family rentals is beginning to slow development activity. The proposed 21st Century ROAD to Housing Act would require institutional owners to dispose of properties within seven years, creating uncertainty for developers and investors.

Houston, one of the nation’s largest build-to-rent markets, has already seen some projects pause amid concerns over the bill, according to the Houston Chronicle. Analysts cited by Yardi estimate the legislation could reduce build-to-rent development activity by as much as 60%.

Why It Matters

The multifamily market is entering a prolonged normalization phase rather than a rapid rebound. While gateway markets are benefiting from constrained supply and stronger demand fundamentals, much of the Sun Belt remains oversupplied after years of aggressive development.

For investors, that creates both risks and opportunities. Distressed assets tied to floating-rate debt and refinancing pressure are becoming more common as lenders work through underwater loans originated before interest rates surged in 2022. Yardi noted that operators may increasingly look to recapitalizations, restructurings, and expense reductions to protect net operating income.

Occupancy trends have also remained relatively stable nationally despite slowing rent growth, underscoring how operators are leaning on concessions and pricing adjustments to maintain leasing velocity in high-supply markets. At the same time, expense growth continues squeezing property performance. Operating costs have risen roughly 30% over the past five years, according to Matrix Expert data cited in the report.

What’s Next

Most signs point to a gradual recovery rather than a sharp rebound in apartment fundamentals. Rent growth likely will remain muted through 2026 as elevated supply deliveries continue entering the market and demand growth slows.

Still, several oversupplied metros appear to be nearing an inflection point as construction starts moderate and lease-up pipelines slowly clear. Investors will be watching whether Sun Belt markets like Austin, Denver, Phoenix, and Nashville can stabilize later this year without a meaningful deterioration in occupancy.

The pace of economic growth, labor market conditions, and interest rate policy will also play a major role in determining whether multifamily fundamentals improve meaningfully heading into 2027.