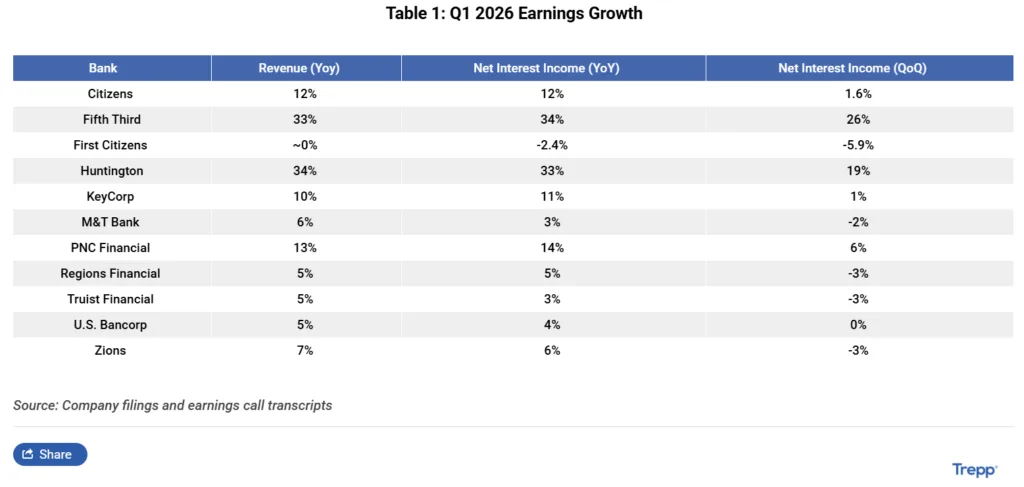

- Super regional bank earnings were stable in Q1 2026, with solid year-over-year growth.

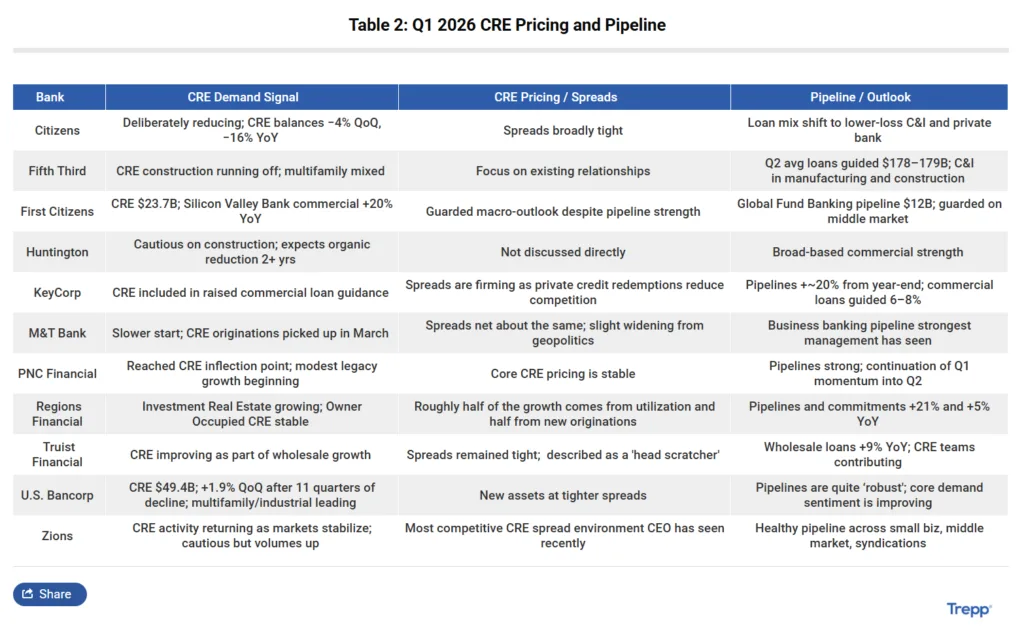

- CRE pricing remained tight despite global geopolitical and energy market uncertainty.

- Office exposure is declining, while multifamily and industrial drive new CRE demand.

- Risk provisions for CRE are stable to improving, but spread compression persists.

Positive Earnings Amid Uncertainty

Super regional banks reported steady earnings for the first quarter of 2026, reports Trepp. Most banks posted year-over-year revenue growth in the mid-to-high single digits, and earnings per share growth in double digits. However, quarter-over-quarter results varied, with some institutions noting lower net interest income due to tight CRE pricing and competitive deposit markets.

Commercial and industrial loan growth provided a boost for several banks, who also raised their forecasts for full-year loan and interest income growth. Despite external risks like the Iran conflict and energy market volatility, CRE asset quality remained healthy.

CRE Pricing Holds Firm

CRE pricing at super regional banks stayed highly competitive, with credit spreads among the tightest in years. Bank executives acknowledged significant pricing pressure, describing market spreads as unusually compressed given the broader geopolitical environment.

Some banks attributed this trend to investors rotating out of private credit and into CRE loans. Although banks continue to address troubled legacy assets, especially in office portfolios, they reported stabilization in overall CRE loan balances and expect modest growth through the rest of the year.

Sector Health: Office Weakness, Multifamily Strength

Office loan exposure continues to wind down, with banks working through existing credits and reducing reserve allocations as loans are resolved. No new office loan growth is anticipated by these institutions in 2026.

In contrast, multifamily and industrial property types are attracting the most new CRE lending. Multifamily deals are rebounding from earlier rate-driven stress, while industrial assets benefit from strong e-commerce and logistics demand, with tenant leverage in industrial markets strengthening as demand continues to outpace new supply in key logistics corridors. Stable leverage and moderate pricing declines have allowed banks to avoid forced refinancings on maturing loans.

What’s Next

CRE pricing is expected to remain tight as banks and private lenders compete for high-quality borrowers. Unless private credit activity slows sharply or bank balance sheets become constrained, spread pressure is likely to persist. Super regional banks remain cautiously optimistic about CRE credit quality and lending through 2026. They monitor sector trends closely and track evolving geopolitical risks.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes