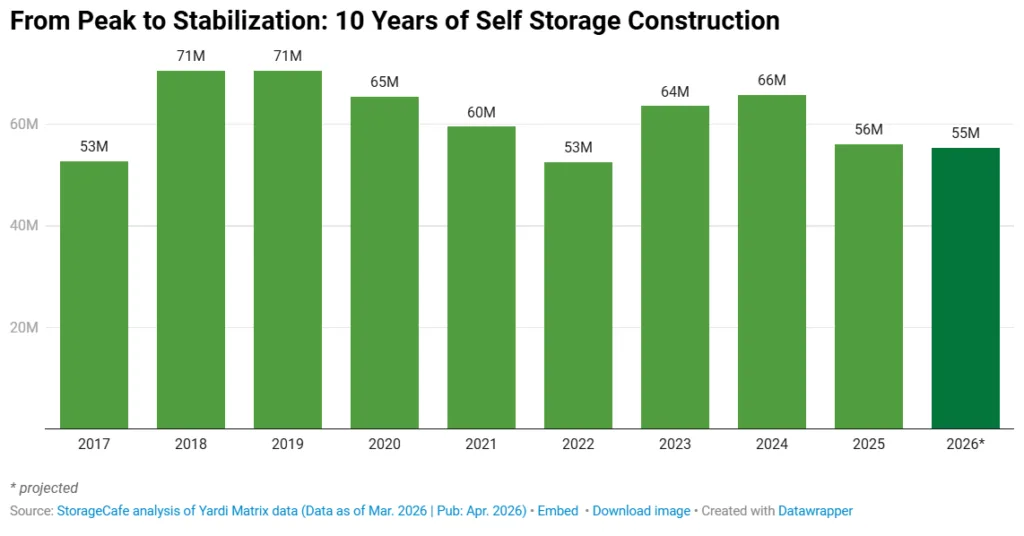

- Self storage supply in 2026 will reach 55.4M SF, a 2.6% increase nationally.

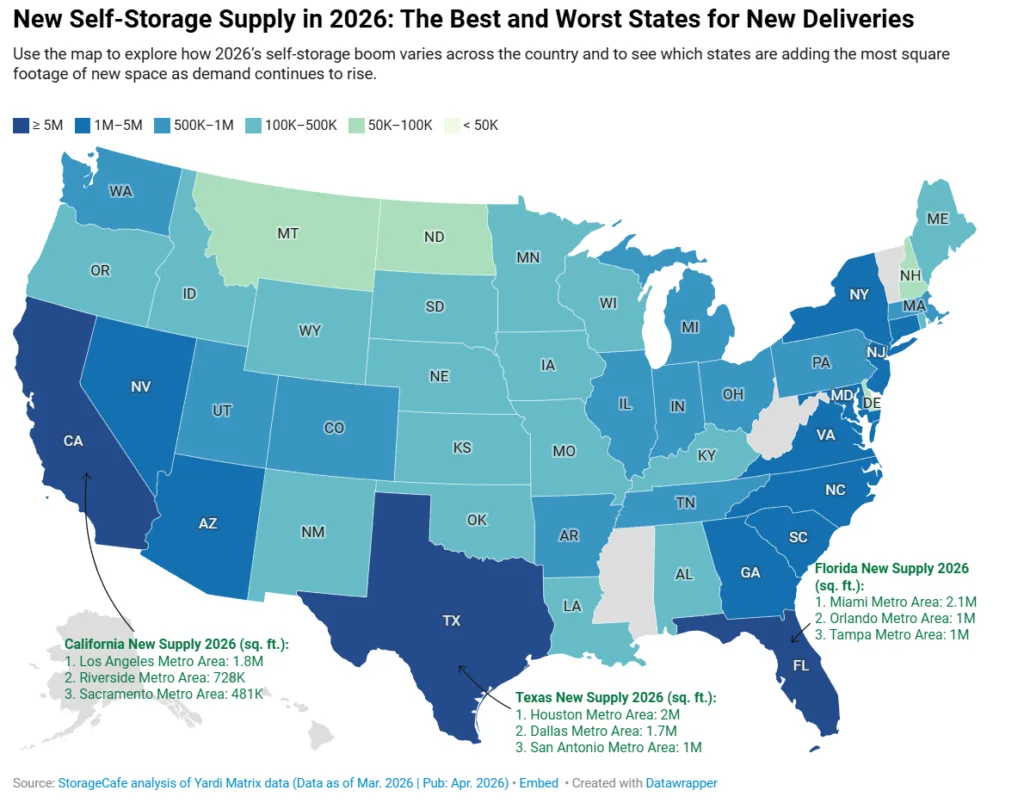

- Florida is set to deliver 10.3M SF, leading all states in self storage expansion.

- Southern and Western metros dominate new deliveries, with 14 of the top 20 metros in the South.

- Large metros grow inventory without oversupply, keeping market fundamentals stable.

Supply Push Led by Sun Belt States

Self storage growth is on track for another strong year in 2026, with 55.4M SF expected to come online across the US, representing 2.6% of total inventory, according to StorageCafe. Florida, Texas, and California lead the expansion, reinforcing the Sun Belt’s dominance in new self storage supply. Florida stands out with 10.3M SF—nearly twice as much as Texas—and claims seven of the top 20 delivery metros.

Southern metros account for more than half of all 2026 deliveries. In contrast, coastal states like California and New York are also growing supply, but the pace remains tied to higher entry barriers and entitlements. New York and New Jersey join the top 10 for inventory expansion, each planning roughly 4% annual growth.

Market Fundamentals Hold Steady

Despite robust deliveries, most large metros see new supply equal only to 2–5% of inventory. This measured growth mitigates oversupply risks and keeps fundamentals balanced. Major metros like New York and Phoenix are each adding close to 3M SF, but street rents remain stable or are easing only modestly.

Florida’s statewide average rent stands at $137/month—slightly above the $133 national average—but prices declined 2.8% last year as supply increased, mirroring broader signs of cooling momentum as new inventory continues to weigh on pricing across several markets. Texas, with 6.9M SF in deliveries and a 3% inventory boost, saw rents drop just 1.7% year over year to about $115/month, thanks to larger, more diversified metro markets.

Emerging Developments in Undersupplied Markets

Previously undersupplied metros, especially in the Northeast, are now drawing significant supply. New York maintains sub-4 SF/capita—yet rents are rising 0.6%, reflecting continued pent-up demand. Similarly, New Jersey’s limited per capita availability supports stable rents despite rising construction.

California’s 2026 pipeline reflects a geographically diverse build-out, with 5.1M SF scheduled—a 2% increase. California’s average street rate remains high at $178/month, and annual rent declines are under 1%.

Secondary Markets Capture Attention

Smaller markets show outsized inventory growth. Lumberton, NC leads with a 58% increase, fueled by local economic investments. Savannah, GA is another hotspot, with a 17.5% expansion and strong investor interest tied to port and industrial activity. This trend signals operators are targeting growth corridors beyond major urban centers where household formation outpaces previous supply.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

What’s Next

The 2026 self storage supply pipeline reflects an industry moving past its boom era, settling into a sustainable rhythm. New deliveries remain strong in markets with resilient drivers—migration, retiree demand, and logistics—but growth is generally calibrated to local absorption. As a result, pricing pressures are limited mostly to well-supplied Sun Belt metros, while undersupplied coastal and Northeastern markets absorb new inventory with minimal rent impact.