- Rental housing markets are stabilizing as supply pressures ease and fundamentals normalize.

- Almost 30% of US markets report occupancy above 95%, highlighting sustained demand.

- Multifamily loan originations rose 36% year-over-year in 2025 amid improving capital availability.

- Refinancing and disciplined capital strategies are driving new opportunities for investors.

Stabilization Sets the Stage

The US rental housing sector is entering a new phase of balance following rapid post-pandemic shifts. In 2026, moderating supply growth and stabilizing asset values have helped normalize rent growth and support resilient occupancy. According to recent data from Arbor, nearly 30% of US multifamily markets are operating above the 95% occupancy mark, underscoring steady housing demand.

Economic Trends and Market Fundamentals

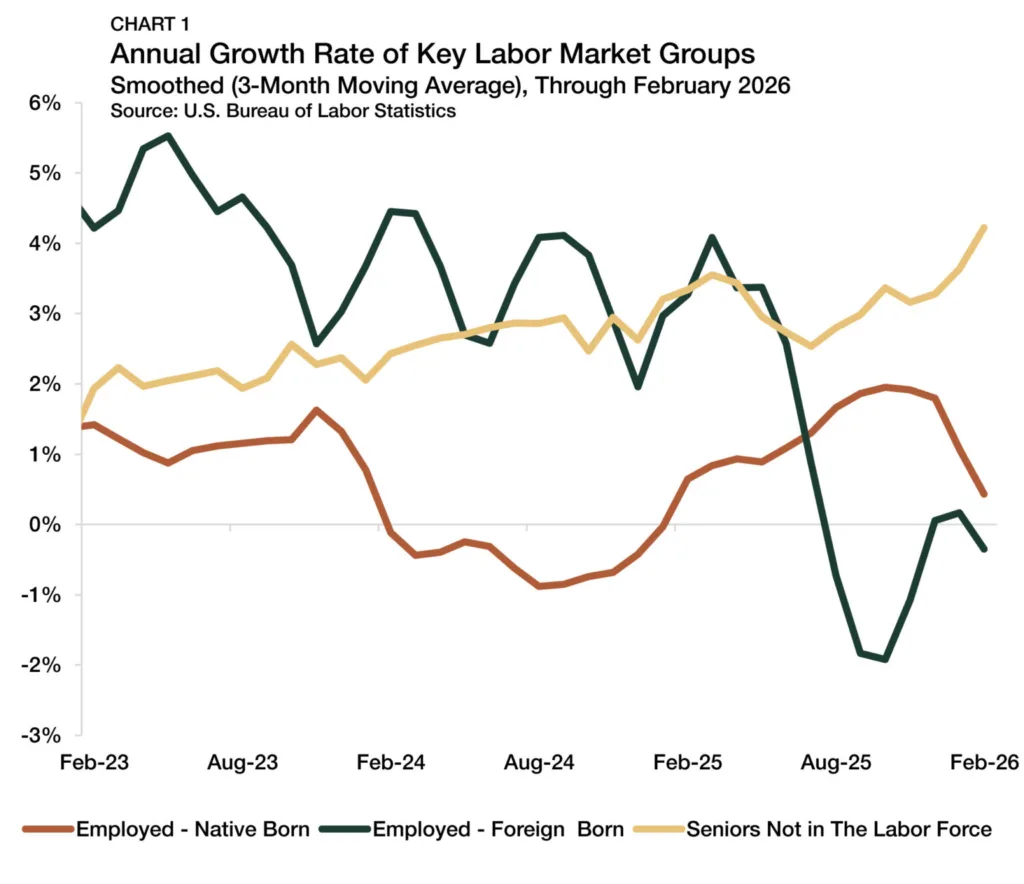

Broader economic uncertainty persists, but the risk of a major contraction has receded. The labor market is cooling, with job gains at historic lows, while real wage growth remains positive. This income resilience has contributed to stronger consumer demand and helped sustain rental housing performance. Meanwhile, tariffs impacting construction costs have eased, lowering project expenses and supporting development feasibility in the rental housing sector.

Capital Markets and Refinancing Surge

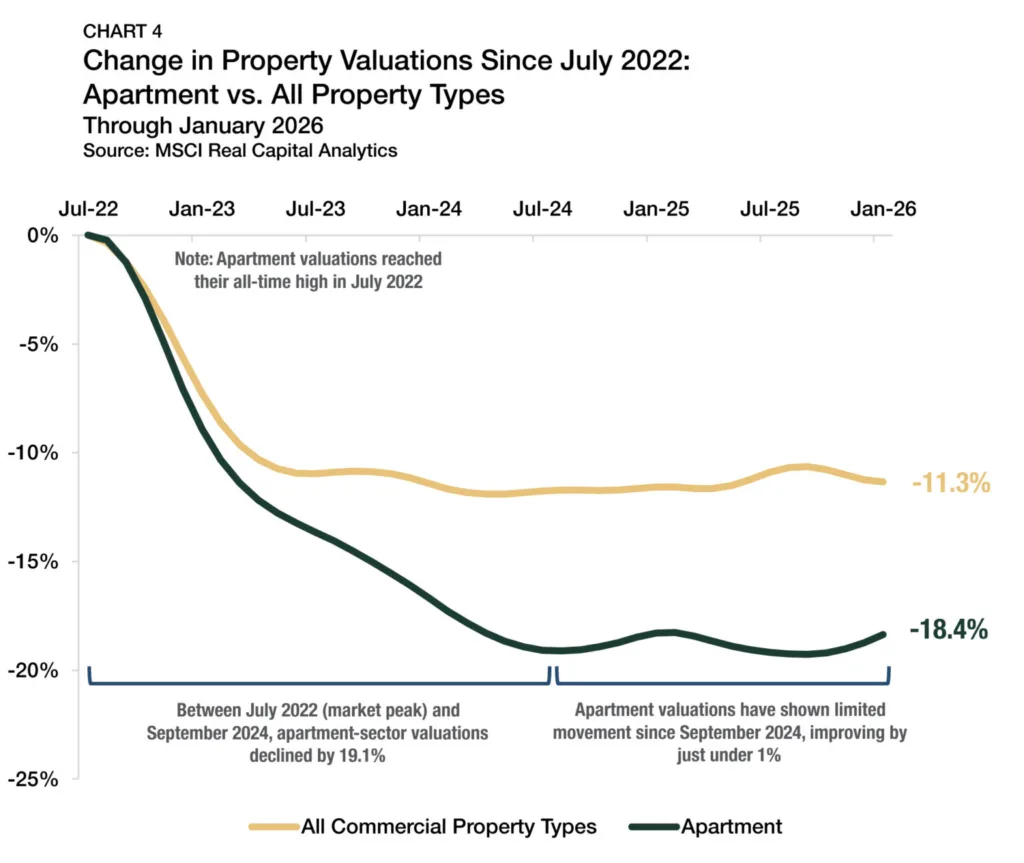

The multifamily capital landscape is shifting as loan originations and refinancing activity accelerate. Multifamily mortgage originations rebounded sharply, up 36% in 2025, signaling renewed investor confidence. National rents remain positive, and valuations, while still below 2022 peaks, are showing signs of recovery. At the same time, bidding activity across asset classes has become more selective, with investors prioritizing deals backed by durable income and clearer downside protection. A significant wave of refinancing is shaping market dynamics, particularly for assets with solid cash flow and manageable leverage.

Policy, Credit, and the Road Ahead

Legislative reforms, such as the proposed 21st Century ROAD to Housing Act, could provide incremental support for supply and affordability initiatives. Lender sentiment is beginning to improve, with a net share of institutions easing multifamily underwriting standards for the first time since 2022. As liquidity returns and refinancing opportunities grow, the rental housing sector appears poised for incremental improvement and selective investment in 2026, with long-term stability within reach.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes