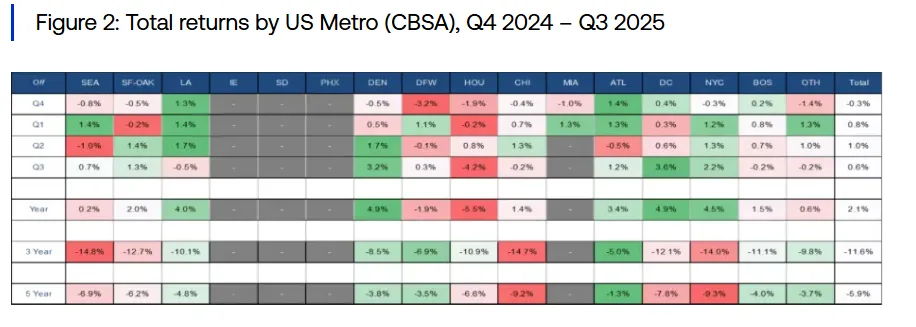

- Office recovery is uneven across regions, with Class A assets in top markets driving most of the valuation gains.

- Investor confidence is returning, supported by improving liquidity and rising leasing activity in prime locations.

- Cash flow trends are turning positive, especially in Europe and the US, signaling early signs of sector stabilization.

- Lower-tier assets continue to struggle, highlighting a K-shaped recovery and the growing divide between top-tier and commodity office stock.

A Sector In Transition

The global office sector is slowly climbing out of a historic downturn, reports AltusGroup, but the path forward remains uneven. Across the US, Europe, and Canada, investors are cautiously re-engaging, targeting best-in-class buildings in top-tier markets. Valuations remain below pre-pandemic highs, but improving cash flows suggest the steepest declines in office values may be over.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

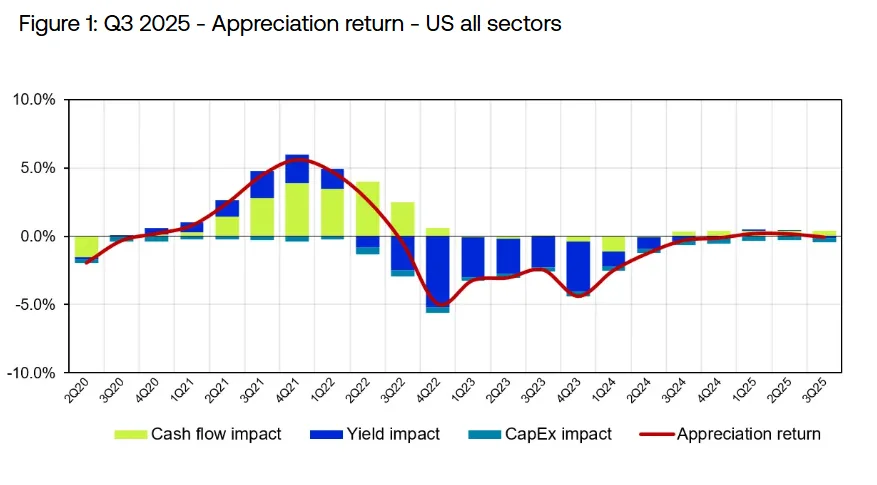

US – Office Values Show Early Signs Of Stabilization

The US office market has taken the biggest valuation hit globally, with average values down 44.8% since before the pandemic. Q3 saw a further 0.9% dip, but positive cash flow growth for the past four quarters (+0.9% YoY) suggests some stabilization is underway.

Key trends:

- High vacancies and loan defaults triggered widespread markdowns, dampening liquidity and investor sentiment.

- Leasing is gaining traction in gateway cities like NYC and San Francisco. Deloitte’s move to 70 Hudson Yards is one example of demand for high-end space.

- Financing spreads have narrowed, with debt for well-leased buildings now pricing around SOFR + 200–300 bps, a major improvement from 600–700 bps two years ago.

- Liquidity is returning, with major deals like the $1B sale of 590 Madison Avenue signaling renewed investor interest.

Outlook: The US office market is moving toward recovery, but performance is diverging sharply by asset class and location. Class A properties in major metros are leading the way, while commodity offices face ongoing headwinds from capex needs, soft tenant demand, and labor market uncertainty.

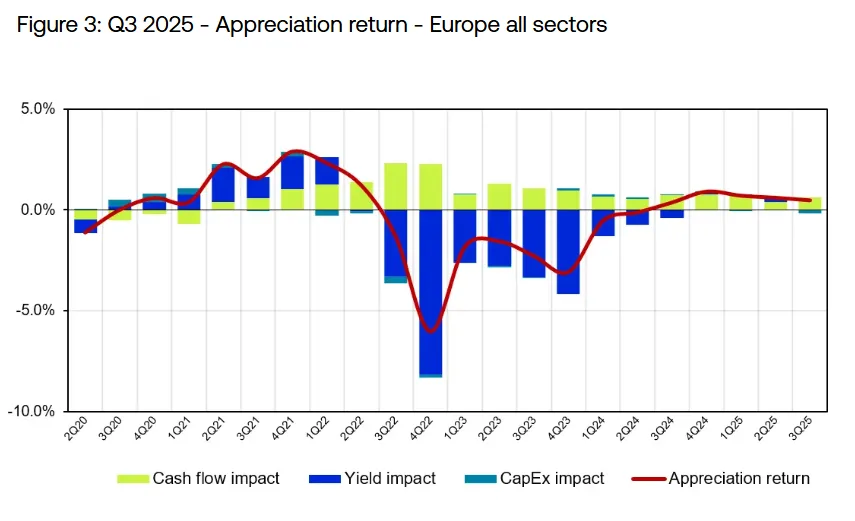

Europe – Resilience And Normalization In Prime Markets

European office values are down 15.4% from pre-COVID but show steady signs of normalization, outperforming North American markets. Q3 values rose 0.5%, with a 2.3% gain year-over-year.

Key trends:

- Cash flow gains of 0.9% in Q3 and a 2.6% increase over the past year support the upward trend.

- Flight-to-quality is strong, with core markets like Paris, London, and Amsterdam seeing tightening yields and active deal flow.

- France outperformed, with office values rising 6.3% over the past year, aided by rent growth and yield compression.

Outlook: Europe’s office market is on firmer footing, with normalization likely to continue. Demand is concentrated in prime assets, particularly in central business districts. Investors are still cautious on secondary assets.

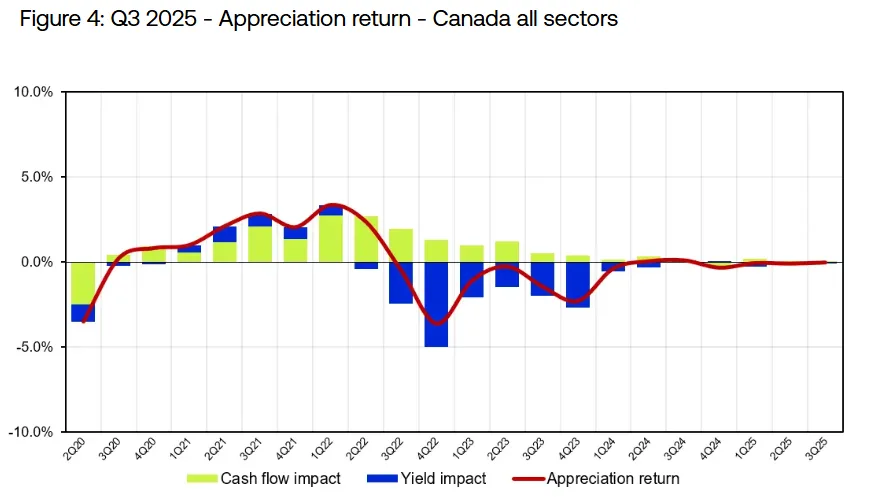

Canada – Activity Picks Up, Especially For Top-Tier Assets

Canadian office values have declined 30% since the pandemic but posted their best quarter in years with a minimal -0.26% dip in Q3. Leasing activity has rebounded sharply and now exceeds 2023 totals.

Key trends:

- Leasing surge driven by financial services, tech, and public-sector return-to-office mandates.

- AAA vacancies below 2% in cities like Toronto are pushing demand into Class A space.

- Investor appetite is returning, with trades of A+ buildings occurring at competitive yields.

Outlook: Canada’s office sector is poised for gradual recovery, led by premium buildings. Weaker labor markets and elevated youth unemployment may moderate growth, while B and C class assets remain under pressure.

A Selective Office Rebound Is Underway

The global office market is stabilizing, but recovery is selective and highly localized. Investors are targeting new, well-located buildings with strong tenant demand, while older assets face structural challenges.

For real estate professionals, the takeaway is clear: focus on asset-level underwriting and market-by-market fundamentals. Broad sector assumptions will miss the mark in a bifurcated recovery driven by quality, location, and adaptability to new workplace demands.

As office usage patterns evolve and capital markets recalibrate, successful strategies will be those that differentiate between core opportunities and structurally impaired stock.