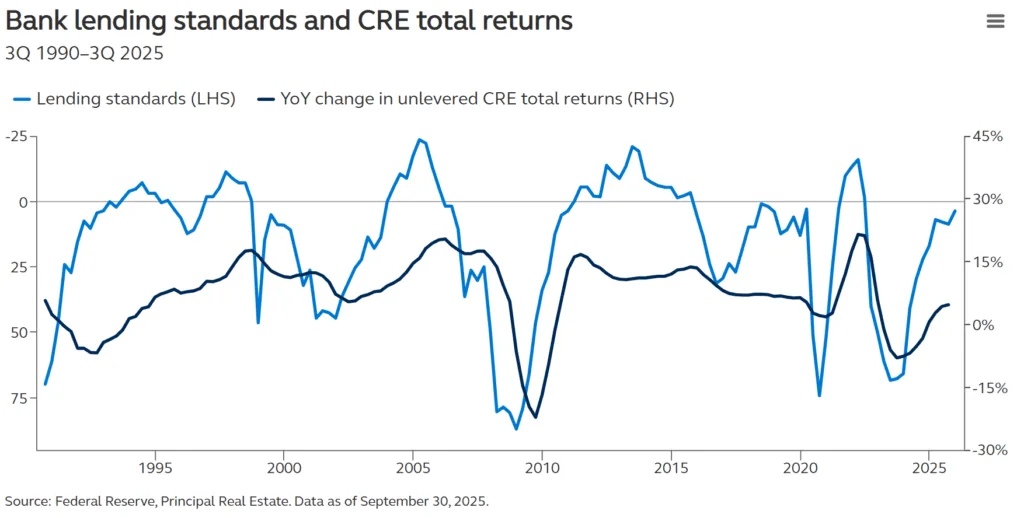

- The Federal Reserve’s 3Q25 Senior Loan Officer Survey reported the first increase in CRE loan demand since 1Q22, indicating a potential market inflection point.

- Lending standards across all property sectors remained mostly stable, with fewer banks tightening compared to prior quarters.

- Core commercial properties saw the strongest rebound in loan demand, rising to +10%, up from -11.5% last quarter.

- This shift aligns with a 17% year-over-year increase in transaction volumes and growing investor sentiment, pointing to a potential CRE recovery into 2026.

A Sign of Thawing Credit Conditions

Principal Asset Management reports that for the first time since early 2022, CRE lending demand has turned positive, according to the Federal Reserve’s 3Q25 Senior Loan Officer Opinion Survey. The shift marks a possible turning point in the lending environment, which has been marked by tighter standards and declining activity since the Fed began aggressively hiking rates in 2022.

Lending Standards Hold Steady

Banks reported relatively stable lending standards across the board, with a net 3.8% of lenders tightening standards—down significantly from nearly 10% in the prior quarter. Multifamily and core commercial sectors saw some of the most notable easing, suggesting banks are more comfortable with underwriting new deals.

- Core Commercial: 3.3% net tightened, down from 11.5%.

- Multifamily: 1.6% net tightened, down from 4.8%.

- Construction & Land Development: 6.6%, improving from 9.7%.

Rebounding Loan Demand

The most significant development is the shift in loan demand, with the net share of banks reporting stronger demand rising to +1.7%, up from -8.7% in 2Q25. Core commercial properties led the way, with a +10% net demand increase, indicating renewed borrower appetite.

- Core Commercial: +10%, a 21.5-point swing from last quarter.

- Multifamily: Flat at 0%, but up from -3.2%.

- Construction & Land Development: -4.9%, a modest improvement from -11.3%.

Why It Matters

The recovery in loan demand is coinciding with improved market activity. Transaction volumes climbed 17% year-over-year in 3Q25, and investor sentiment—measured by the CRE Finance Council Index—has approached pre-downturn levels, reaching nearly 123. Historically, shifts in loan demand and standards have preceded changes in CRE valuations, suggesting a possible acceleration in pricing ahead.

What’s Next

The current CRE lending backdrop is drawing comparisons to the post-GFC recovery in 2010–2011, when improving credit availability spurred a rebound in real estate pricing. If current trends hold, 2026 may mark the start of a more durable recovery in commercial real estate, especially in core sectors.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes