- The One Big Beautiful Bill Act (OBBBA) revives key tax incentives for domestic manufacturing but cuts EV and green energy credits, prompting a strategic reset.

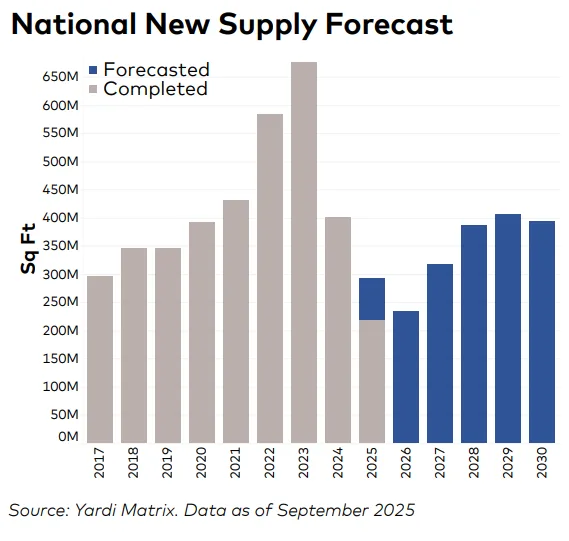

- Rent growth has slowed nationally, while vacancy rates continue to rise amid a wave of new industrial supply.

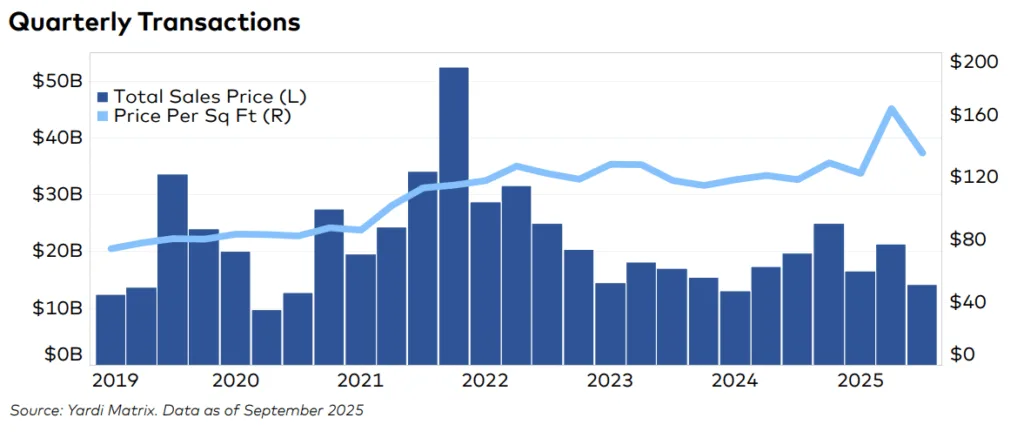

- Industrial sales hit $52.5B through Q3, with logistics hubs like Atlanta seeing strong price gains despite softer volume.

- Construction remains elevated, but owner-occupied projects and delayed deliveries are easing pressure in some markets.

Tax Reform Reshapes Manufacturing Priorities

Yardi Matrix reports that the OBBBA, passed in mid-2025, is set to impact US manufacturing for years. The law restores 100% bonus depreciation for equipment and facilities placed in service after January 19. It also reintroduces the expensing of domestic R&D costs, freeing capital for innovation and expansion.

The bill includes incentives for reshoring and enhanced interest deductibility, aimed at boosting domestic production. However, it also ends EV and green energy tax credits earlier than expected. That has led to a strategic rethink, especially for automakers and battery manufacturers. Solar panel producers also face an uncertain path.

Rent Growth Slows, Vacancies Rise

National industrial rents averaged $8.72 PSF in September, up 6.1% year-over-year. However, rent growth has cooled compared to recent years. Philadelphia, Atlanta, and Miami led rent gains, each posting over 8.5% growth.

Vacancy climbed to 9.5%, up 250 basis points from a year earlier. Over 2.7B SF of space has delivered since 2020, softening landlord leverage. The gap between new lease rates and in-place rents also narrowed, with new leases averaging $10.00 PSF, down from a $2.20 premium a year ago to just $1.28.

Construction High, But Impact Varies by Market

Developers had 340.5M SF of industrial space under construction as of September, equal to 1.7% of total inventory. In Denver, vacancy is up, but much of its pipeline is tied to large owner-occupied projects, like PepsiCo’s new 1.2M SF plant.

Amazon’s long-delayed 3.5M SF Loveland facility also inflates Denver’s numbers but hasn’t added leasing pressure. Other markets with elevated pipelines—such as Phoenix and Memphis—may also avoid oversupply due to similar build-to-suit activity.

Sales Volume Rebounds, Led by Logistics Markets

Industrial investment is recovering after 2024’s interest rate cuts. Year-to-date sales totaled $52.5B, with the average price at $142 PSF. This puts 2025 on pace to surpass last year’s volume and marks the strongest year since 2022.

Atlanta, a key logistics hub, saw prices rise 31.3% to $140 PSF despite a modest dip in overall volume. The market’s strong infrastructure and location near the Port of Savannah continue to attract third-party logistics firms. Sales were also strong in high-cost markets like Orange County, Los Angeles, and New Jersey.

Outlook

Manufacturers and developers face a complex mix of tax incentives, policy shifts, and changing tenant demands. Localized supply chains and reshoring efforts are likely to drive growth. But as vacancies rise and rent growth slows, the market may favor more strategic development in the year ahead.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes