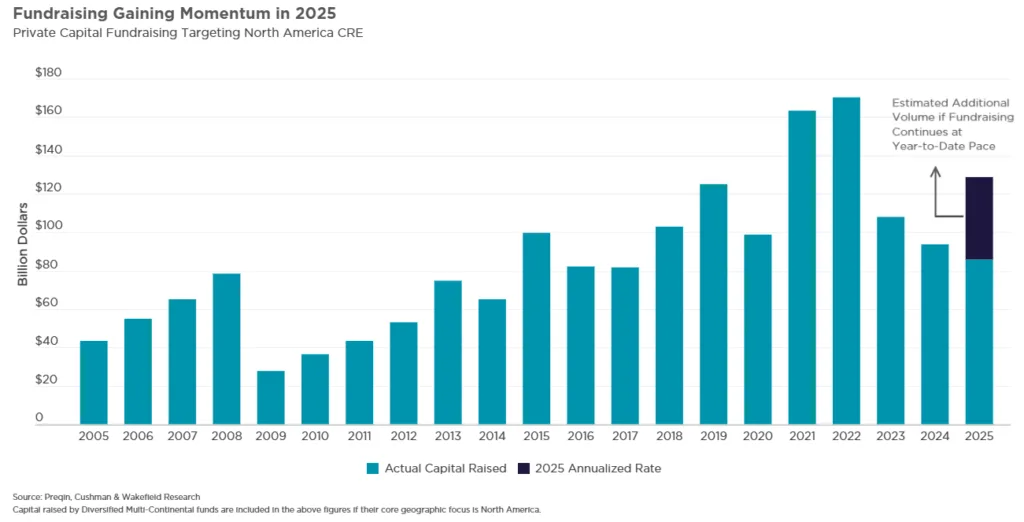

- Private CRE fundraising is on track to hit $129B in 2025, a 38% YoY increase and a strong rebound from lows in 2023–2024.

- Debt markets and property sales are showing signs of stabilization, with loan originations up 30% YoY in H1 2025 and pricing declines easing.

- Multifamily, industrial, and data centers dominate fund targets, while office and retail remain largely out of favor.

Recovery Signals Multiply Across CRE

After enduring one of the most aggressive interest rate hiking cycles in modern history, the US commercial real estate (CRE) sector is beginning to find its footing, per Cushman & Wakefield.

Vacancy rates are stabilizing or declining across key asset classes, speculative development has cooled, and debt markets are coming back to life. New loan origination volumes rose more than 30% year-over-year in the first half of 2025, contributing to a rise in transaction activity and helping property values find a floor.

But the clearest sign that confidence is returning? Capital is flowing again—and at scale.

Private Equity Capital Regains Strength

private real estate fundraising is surging in 2025. As of August, $86B has been raised by private CRE investment vehicles, putting the sector on pace to reach $129B by year-end. That would mark a 38% increase from 2024, and a definitive turnaround from the pullback seen in the previous two years.

The biggest fund closings of the year so far—Brookfield Strategic Real Estate Partners V ($16B) and Carlyle Realty Partners X ($9B)—also represent the largest ever raised by each respective firm, underscoring renewed institutional conviction in the sector’s long-term fundamentals.

According to Blackstone President Jonathan Gray, investor sentiment has shifted:

“The tone now is much more open… the lack of new supply and the falling cost of capital are laying the foundation for recovery in real estate.”

Multifamily and Industrial Are Still the Favorites

A clear trend is emerging among the largest 2025 fund closings: nearly all are prioritizing multifamily and industrial assets. Of the 20 largest equity funds closed this year, 13 explicitly target these property types, while others focus exclusively on data centers, reflecting continued belief in both demographic and digital tailwinds.

Notably, Carlyle’s CRP X fund is steering clear of office, hotel, and retail altogether, signaling that many institutional investors remain cautious toward sectors with structural headwinds.

Debt and Digital Infrastructure Draw Big Bets

It’s not just equity that’s attracting attention—private debt funds are booming too. CRE debt vehicles have raised more than $20B so far in 2025, putting this year on track to be the second-best ever for debt fundraising, trailing only 2021.

Among the biggest:

- Blackstone Real Estate Debt Strategies V ($8B), matching its 2021 predecessor as the largest debt fund globally

- Blue Owl Capital’s Digital Infrastructure Fund ($7B) and Principal’s Data Center Growth & Income Fund ($3.6B), reflecting strong investor demand for scalable digital assets

These debt and digital strategies are positioning funds to capitalize on maturing loans and technology-driven asset demand in a market still starved for liquidity.

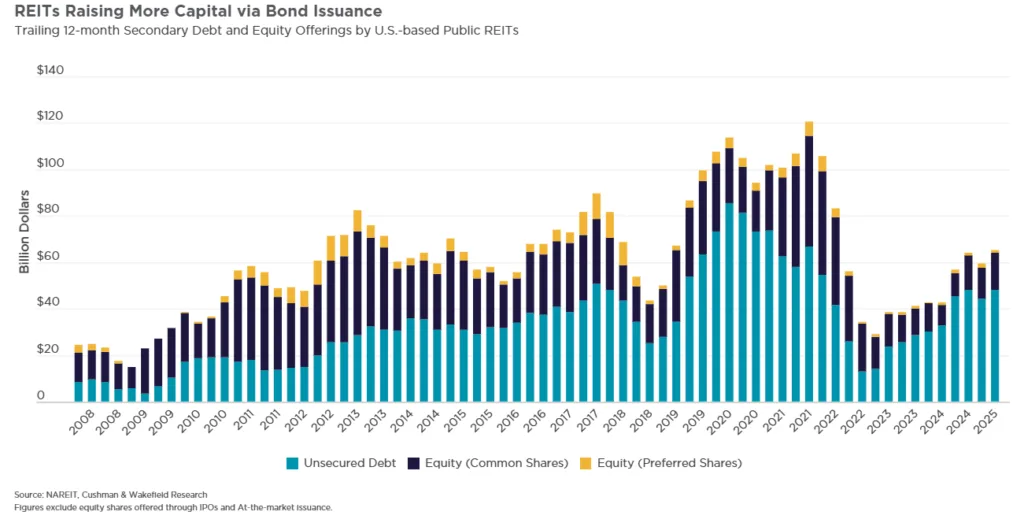

REITs Tiptoe Back into Fundraising

After keeping a low profile during the rate-hike cycle, publicly traded REITs are reengaging capital markets, particularly through debt issuance. In the 12 months ending Q2 2025, unsecured bond offerings hit $48B—up nearly 4x from late 2022 and slightly ahead of pre-pandemic averages.

Equity issuance remains subdued, with most REITs trading below NAV. Still, momentum is building. The recent uptick in secondary equity offerings marks the highest level in nearly three years, hinting at growing confidence among public market investors.

Looking Ahead

This resurgence in fundraising—particularly in multifamily, industrial, and digital infrastructure—suggests the CRE cycle may be entering a new phase. While macro uncertainty remains, the willingness of both private and public investors to commit fresh capital is a leading indicator of future deal flow and asset appreciation.

With pricing resets largely behind us and capital availability on the rise, 2025 may be remembered not just as a year of stabilization, but as the beginning of the next CRE investment cycle.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes