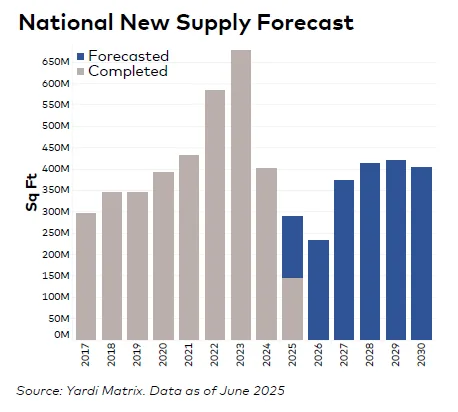

- The US industrial market hit a 9.0% vacancy rate in June 2025 as more than 2B SF of space delivered between 2020–2024 finally caught up with cooling demand.

- Rent growth remains solid, particularly in Sun Belt logistics hubs like Atlanta and coastal markets such as Miami, despite a tightening lease spread.

- Uncertainty around tariffs and a recent tax law targeting green energy have cast a shadow over future developments, particularly in the so-called Battery Belt.

A Decade-High Vacancy Rate

Following an unprecedented supply boom, the national industrial vacancy rate rose to 9.0% in June—marking a high-water mark for the decade, reports Yardi Matrix. Over 2B SF of industrial space were delivered between 2020 and 2024, spurred by pandemic-era supply chain disruptions and e-commerce growth. But 2025 is seeing the hangover: normalized demand and geopolitical headwinds are now slowing lease absorption.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

What’s Still Driving Growth?

Despite headwinds, long-term demand fundamentals remain intact. These include reshoring and nearshoring trends, data center expansion, and the continued shift toward omnichannel retail. Yet each faces friction. Tariffs have cooled leasing activity. Green manufacturing projects are threatened by eliminated tax credits. Data centers face mounting legal and infrastructure hurdles—even as the federal government pushes for global AI leadership.

Rent Trends Show Resilience

National in-place rents averaged $8.60 PSF in June—up 6.2% year-over-year. New leases are still signing above market averages, with a national spread of $1.57 PSF. That said, this gap has narrowed in recent quarters, as tenants gain leverage in lease negotiations. Miami ($12.86/SF) and Atlanta ($6.35/SF) led rent growth, up 9.4% and 8.5% respectively, thanks to strong port activity and booming logistics sectors.

Supply Pipeline Cooling

As of June, 341.8M SF of industrial space were under construction, representing 1.7% of national stock. Phoenix, Dallas, and Memphis led the pipeline by market share. Notably, development momentum in the Battery Belt—stretching from Georgia to Michigan—is at risk. The newly signed One Big Beautiful Bill Act eliminated tax credits for EVs and tightened rules for battery makers, potentially making some projects unviable.

Southern California Cools

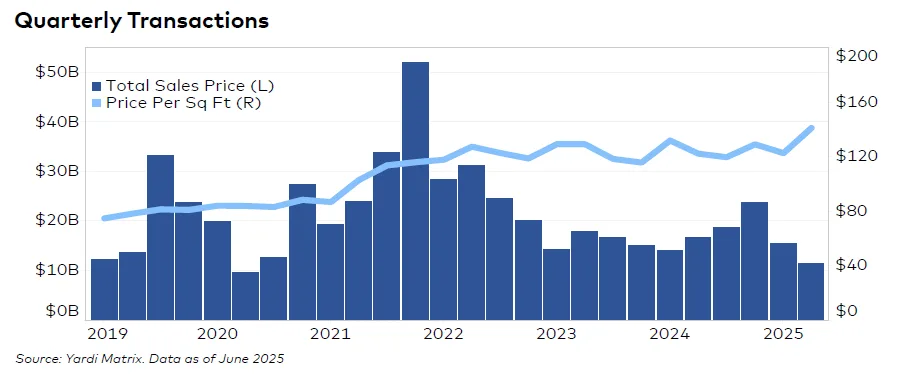

Industrial sales totaled $27.6B in the first half of 2025, with an average sale price of $130 PSF. But former hot spots like Southern California are cooling off. Los Angeles prices slipped to $279/SF (from a 2023 peak of $316), while Orange County fell to $301/SF from $343 in 2022. The Inland Empire dipped to $247/SF from its $287 peak. Regulatory challenges and land scarcity are expected to constrain future supply in the region.

What To Watch

- Leasing decisions: Many tenants are delaying commitments amid trade policy uncertainty.

- Battery Belt fallout: The impact of federal policy changes on EV-related manufacturing could reshape regional development plans.

- Sun Belt strength: Markets like Atlanta and Phoenix continue to see high activity due to demographics and infrastructure advantages.