- $290B in office loans—representing 33% of all office debt—will mature by the end of 2027, with Manhattan, Los Angeles, and Boston leading in dollar volume.

- The sector is grappling with 19.4% national vacancy rates, weak job growth in office-using industries, and stubbornly high interest rates.

- Amid rising delinquencies, the likelihood of refinancing diminishes, making asset sales, loan workouts, or conversions increasingly attractive.

Loans Come Due

More than 14K office properties across the US are backed by loans that have recently matured or will do so by the end of 2027, reports yardi matrix. These loans total roughly $290B—one-third of the entire office loan market. Metro areas with the highest maturity share include Atlanta (50.5%), Denver (49.0%), and Chicago (46.0%), with Manhattan topping the chart in absolute dollar volume at $59.9B.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Interest Rate Blues

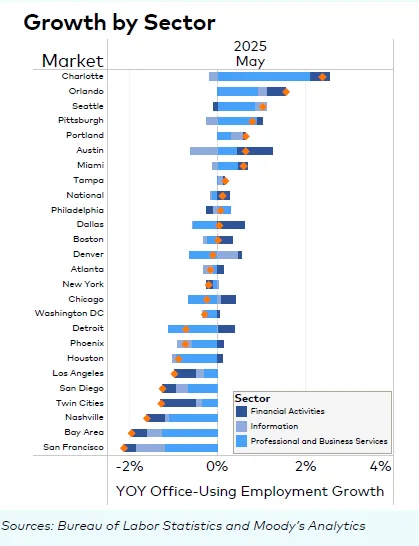

Hopes that rate cuts would ease refinancing pressure faded in June, when the Fed held steady on interest rates following a strong jobs report. Compounding the issue, office-using employment shrank by 1K jobs last month, driven largely by a 7K-job loss in professional and business services.

Delinquency Spike

Office CMBS delinquencies rose to 11.08% in June—up 3.5% year-over-year, per Trepp. With more than 60% of maturing loans originated pre-2020 (before the pandemic-induced collapse in office demand), refinancing has become increasingly difficult. Many assets are now worth less than their loan balances, making loan extensions harder to justify.

Bright Spot In Manhattan

Despite national headwinds, Manhattan showed resilience with a falling vacancy rate of 15.2%, down 130 bps year-over-year. Amazon and law firm Goodwin Procter have inked major leases totaling over half a million SF this year, helping to buoy demand in a market where remote work is less practical.

Pipeline and Supply Slowdown

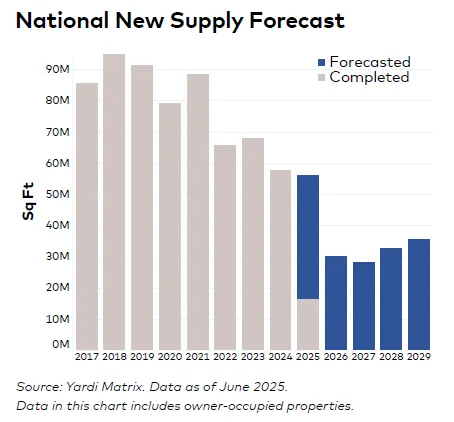

Only 6.5M SF of new office construction started in the first half of 2025, mirroring last year’s historic low. Just 0.6% of US office stock is under construction, signaling that developers are pumping the brakes amid demand uncertainty.

Sales Activity

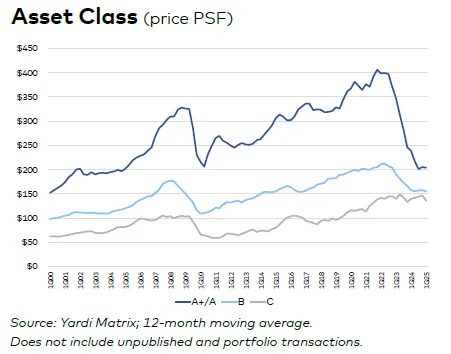

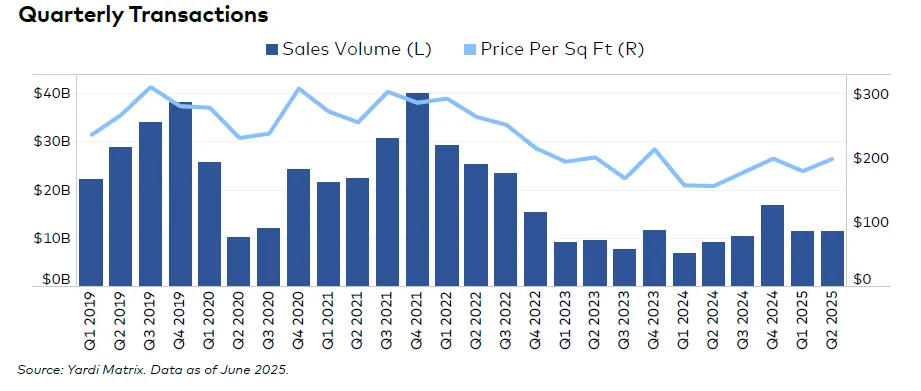

YTD office sales volume reached $23B, with average pricing at $189 PSF. Notably, Atlanta remains relatively stable, with recent sales—like Spear Street Capital’s $133.8M purchase of 1100 Peachtree—demonstrating moderate discounts but resilient pricing compared to 2019.

Why It Matters

The long-anticipated office loan maturity wall has arrived. With refinancing options shrinking, borrowers are facing tough decisions. Conversions, workouts, and defaults are all on the table, and the sector’s ability to adapt will determine how deep the shakeout goes.

What’s Next

As delinquencies rise and financing gaps widen, expect a wave of distressed sales and conversion initiatives. Meanwhile, cities like Manhattan may see renewed interest as functional necessity and tenant diversity offer some insulation from broader market woes.